Click Here for Printable Version

October is usually the most volatile month of the year, this time though the US equity markets experienced their quietest month in history.

As the 30th anniversary of the Black Monday stock market crash passes, amid the rising uncertainty of US tax reform, Catalonia declaring independence, revelations that some Middle Eastern countries had funded terrorism, North Korea and the clear desire of global Central Banks to end QE and/or raise interest rates, US markets again hit new all-time highs.

These gains have though not fully benefitted UK investors, as the pound continued to recover and the FTSE delivered only modest gains.

This all may seem to be totally illogical but markets are rational.

We are in the midst of the US corporate results season and it has been a good one. Whilst the geopolitical world seems to be heading to “hell in a handcart” the economic one continues to do just fine, and its companies we buy, not governments.

Exchange Traded Funds

In the old days when grumpy old stockbrokers were asked why the stock market was going up the irritated answer was always

“there are more buyers than sellers…”

They were right then and they are right now. The only difference is the way the buyers buy.

Investment managers rarely pick stocks, instead they allocate assets. They move the percentage of money allocated between cash, bonds, equities and hedge funds not only on a broad basis but between individual countries as well.

The huge sums of money involved mean that this could be a complex process. As ever the industry has come up with methods to assist the flow of money around the world.

The development of Index Exchange Traded Funds (ETF) means that asset allocators can quickly sell one market and buy another in just two deals.

So as money flows into an index then the majority of money goes into the biggest shares, which thus perform the best and attract even more money.

This phenomenon always happens during strong bull markets when there is heavy buying taking place.

We also need to bear in mind when markets reverse then these big companies are also the easiest to sell.

It also isn’t efficient; it takes no account of underlying corporate quality or value.

This chart shows the relative performance of the weighted S&P 500 index and the unweighted one.

This shows that the current buying is being driven by the asset allocators not the stock pickers.

Market Psychology

Recent results from the major Wall St investment banks suggested that share trading activity is at very low levels.

One quote from Credit Suisse is typical of what is currently happening …

“two rockets flew over Japan and nothing happened, there were no calls. That’s absolutely crazy.”

No doubt in the future with the benefit of hindsight it will certainly appear to be so, but today as ever, there are rational reasons for the lack of fear and thus volatility in global equity markets.

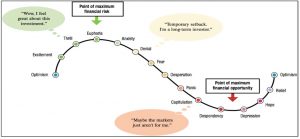

We have seen a change in market psychology from fear to FOMO (Fear of Missing Out), and importantly this is now the least predictable part of the cycle.

So what’s going on? After all, during most of the first 8½ years of the bull market, the mood was one of fear.

Although stocks were rising, the psyche of investors was dominated by their experiences of the 2008/9 Credit Crunch.

Every geopolitical event e.g. Grexit, the Scottish Referendum seemed to herald the next big meltdown (even though underlying fundamentals remained reasonably strong). Now, the psychology has changed, geopolitics doesn’t matter, just buy shares because they are going up.

We have gone from Fear to Greed or more accurately, FOMO. This famous chart shows the market psychology cycle.

There is increasing talk in the US about the potential for a stock market melt-up, Trump tax cuts, low interest rates, with economists suggesting there could be at least three years until the next US recession.

A melt-up is a last-gasp surge like the one in 1999 on the run-up to Y2K, just before markets rolled over, 9/11 occurred and Bush Jnr embarked on Gulf War2.

That would count as Euphoria on the above chart. We are not there yet, as up until now this remains a truly unloved bull market The hazards of market timing were illustrated by a Bank of America study last year, which showed that missing the very end of a bull market often means missing a quarter of its gains.

This is a complex and very difficult part of the cycle, bailing out too early can be very expensive.

But we must also remember that anyone who bought global stocks just before the worst bear market since the Great Depression would now have doubled their money, and historically this is not unusual, in fact, it is typical of how markets work.

Provided, of course, investors have the mental strength and a financial plan which enables them to remain invested in the face of a doom-laden, despondent media onslaught.

Markets

As long term investors we can ignore this change in market psychology, we must though recognise it for what it is i.e. normal noise and to be expected at this point of the cycle.

It does though remind us that that we are closer to cycle end than the beginning.

Also, we must always revert to economic fundamentals and make a judgement as to whether investments in bonds or equities represent good value or not. For bonds the picture is pretty clear and getting clearer each day.

“Cheap money” from the central banks is coming to an end.

The Fed, the ECB and now the Bank of England are increasing the cost and reducing the availability of money.

If inflation picks up, as it should (but currently isn’t) then this tightening process will accelerate.

So bonds are poor value. As the global economy returns to normal then corporate profit growth will accelerate.

We are though currently in a guessing game as to extent that this will happen.

Historically, analysts underestimate this rate of growth, and the evidence from the current results season suggests the same thing is occurring this year.

This means that whilst valuations are expensive they are crucially justifiable.

So whilst there is a whiff of “Excitement” in the investment air the fundamentals do support it.

There is always a “but” and it is from the fact that there are many variables in play at present and the supports for the markets are fragile and can be easily eroded, particularly by inflation and the actions of the Central Banks.

For now though inflation is low and so the party continues.

October 2017

Click Here for Printable Version