Click Here for Printable Version

November saw the difficult market conditions continue. The markets are worrying that the US Federal Reserve Bank has moved too fast too soon, monetary conditions have been tightened as interest rates rise and US Quantitative Easing is reversed.

The Federal Reserve Bank is shrinking its balance sheet which reduces the Money Supply and magnifies the impact of what appears to be quite modest increases in interest rates.

If we then add in the impact of Trump’s America First trade policies then there is a risk that company profit expectations for 2019 might be squeezed, hence markets have to fall. But what if the Fed slows down and Trump does a trade deal with Xi of China?

Late November Fed Chair Powell moderated his language which lead the markets to consider that they might indeed be slowing their stated strategy. December will see some significant geopolitical events, there is the Brexit vote in Parliament, the Italians trying to agree a budget with the EU, the Fed meets to set interest rates. Focus will also be on the oil price, are the Saudis doing Trump a favour?

But it will be the Fed and US/China trade talks that will be critical to the market’s direction. Unfortunately though, the headlines will be dominated by the Brexit soap opera.

The Latest (but possibly not the last) Brexit Deal

As expected the Prime Minister has negotiated a withdrawal agreement, which is the second stage of the Brexit process.

This is the legal divorce settlement that paves the way for the ultimate trade deal (which is all the markets are concerned about).

This agreement points towards the trade deal being the softest of soft Brexits. It has come in for a lot of criticism, but to be fair to Theresa May, she seems to have achieved what was once considered impossible, i.e. to have a very close relationship with the EU without having to sign up to free movement of labour.

This was the one thing that David Cameron wanted, it was Juncker’s refusal to accept this that triggered the whole soap opera.

However, it could be all academic as she does not appear to have enough support for it to pass through Parliament. We have always said that the risk of Brexit is not economic but political. Sadly, it would appear that this theoretical risk is about to become a real one.

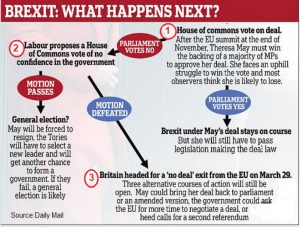

What happens next? This flow chart gives us a simplified road map.

In investment everything is possible but we have to ask what is the most probable outcome?

At the moment it is probable that Theresa May will lose the first stage of this roadmap. However, there is time yet for her to win support.

In order to get over the line she needs to get the Tory remainers onside, the DUP and for some Labour MPs to either vote for the deal or abstain. It is possible that the remainers will begrudgingly fall into line.

The current legal view is that if there is no Parliamentary approval before 29th March 2019 then the UK will leave the EU regardless, hence for them this “very soft” deal should be better than No Deal.

But they might just hang on for a possible second referendum?

The DUP say they would need a change to the deal in order to support it.

For Labour rebels meanwhile they would have to make a judgment of whether it is better to support the present government or vote it down and thus trigger Number 2 on the flow chart, a No Confidence vote and thus a possible General Election. Logically therefore, this deal seems doomed, but in UK politics you never know!

The REAL QUESTION Is Not Whether The Deal Can Pass Parliament, But Can The Conservatives Win The Ensuing No Confidence Vote?

If they can, then we are back to square one and a Conservative/DUP government goes to Brussels to see if this deal can be improved on.

In hindsight, if the EU had agreed that stages 2 and 3 (the actual trade deal) would take place concurrently then there wouldn’t be this problem; it may well be that something along those lines might ultimately be a solution?

If the Conservatives can’t win a No Confidence vote then we are in for another General Election and the risk of a Labour or Labour/SNP government increases significantly.

Hence the DUP might ultimately fall into line? So as we write and without much confidence, the most probable outcome is: Theresa May loses the Brexit deal vote on December 11th; this then triggers a No Confidence vote, which the Conservatives with the support of the DUP might just win?

The Brexit deal would then go back to Brussels to see if it can be improved on. For the markets, they still expect some sort of deal to be done.

The risk is not ultimately of a Hard Brexit, as virtually all independent economic forecasts suggest that the short term impact would be negative but manageable and depending on the policy response, might be positive in the long term, but of a chaotic No Deal where the UK and EU have an acrimonious divorce with no agreement of any sort.

The probability of that seems small with options to extend the Transition Period or temporary EEA membership examples of possible short term measures currently being suggested to avoid a chaotic exit.

The headline grabbing Bank of England forecasts show the cumulative impact over 10 years versus “where you could have been”.

On an annualised basis they match the 1.0% to 1.5% immediate hit to UK GDP from the independent economists. But that doesn’t make such dramatic headlines!

The US Economy

The Brexit soap opera is interesting but what really matters for client portfolios is whether the US economy, which represents nearly 70% of global consumer expenditure, is about to enter recession. We continue to plan for a difficult market in 2019, particularly in the second half.

US recessions typically occur in the first year of a new Presidency, which will begin in February 2021. Stock markets are predictive some 12 to 18 months in advance of the recession actually happening.

That brings us to a “danger zone” in late 2019.

Client cash reserves should reflect this possibility.

There are many supposedly reliable indicators threatening to give sell signals. The danger is that the markets are regularly subjected to these often false signals, if all were accurate then computers could be safely left to manage money, they can’t, which tells us just how unreliable these indicators are.

The other very reliable long term indicator is the US Conference Board Leading Indicator.

As this chart shows the Leading Indicator turns down before a recession arrives, there is no sign as yet of this happening. Ultimately, this all depends on the US Federal Reserve Bank, there are fears they have gone “too hard, too fast”.

Also Trump has been positive for markets but he is at risk of becoming a liability. His “America First” policy is designed to win political support in America’s mid-west rust belt, but the General Motors announcement of mass plant closures and redundancies is highlighting the economic reality of his policies.

Steel tariffs have added $100m to GM’s cost base when the nextindustrial revolution will hit future demand for traditional vehicles.

Markets

Much as ever will depend on Trump, will the penny drop that trade tariffs will kill American jobs rather than save them?

Or will he “double down” and start penalising the likes of GM for making practical business decisions?

GM is just the first of many that will be impacted by the arrival of the next industrial revolution.

Businesses don’t want to be left making steam traction engines as the diesel tractor arrives. If Trump can do a deal with China then the headwinds from his trade war may well be reversed.

The G20 meeting with Xi in Buenos Aries did bring some progress, the US has delayed introducing another series of tariffs for 90 days, which is all the markets could reasonably have hoped for at this stage.

December is likely to be an even more complex than normal trading month.

Santa traditionally arrives after Futures and Options Expiration. This year it is later on the 19th December, the Fed meets to set interest rates on the 18th and announces its decision irritatingly on the 19th.

This will create volatility, especially when there will be so few trading days until Year End.

The Brexit Parliamentary Vote on the 11th will add to the mix, especially if there is to be a No Confidence Vote before Parliament closes on the 20th December.

This is the sort of environment where real investors tend to sit on their hands and let the computerised trading robots swing prices around until the murky picture becomes a little bit clearer.

The traditional Santa Claus market rally normally brings a nice boost to indices before year end, hopefully Trump doesn’t cancel it this year!

December 2018

Click Here for Printable Version