If the old adage of “so goes January so goes the rest of the year” is right then 2015 is going to be very confusing. The Global markets normally move in step with one another, however, this month they diverged. The US S&P 500 was down in dollar terms by 3% and Germany’s DAX in euro terms was up by 9%.

Dollar strength and euro weakness moderated these numbers for UK investors but the difference between these returns is startling. At the heart of this move was the announcement by the president of the European Central Bank “Super” Mario Draghi, that some 6 years after the UK and USA sought to save their banking systems through Quantative Easing, Europe will now do the same.

This move had the desired effect and the euro promptly weakened.

The canny Swiss, fearing that this would happen, abandoned the peg that linked the Swiss franc to the euro the week before. Why now after six years have the Europeans finally woken up the problem of a moribund European banking system and thus slowly deflating economy? Well perhaps it is a perfect deflationary storm of an oil price war, Russian sanctions and the return of the “Greek issue” that finally persuaded the Germans to allow the ECB to do its job?

European Quantative Easing

They therefore do not have enough cash to lend and remain very risk averse. Any cash they get goes on deposit with the central bank. Their focus is on preserving capital; instead of lending to other banks on the intra bank market they prefer to be charged interest rather than receive it.

QE means that the value of their government bond holdings goes up, they can book a profit and thus their capital goes up. But this on its own will not solve the problem. Debts need to written off, banks amalgamated, and new capital raised.

The ECB knows this; QE is just the first part of a wider programme, the details of which are not as yet known.

Years after the Federal Reserve began QE in the USA; Mario Draghi has overcome German opposition and unveiled a plan to buy government bonds as part of an asset-purchase program worth about e1.1 trillion.

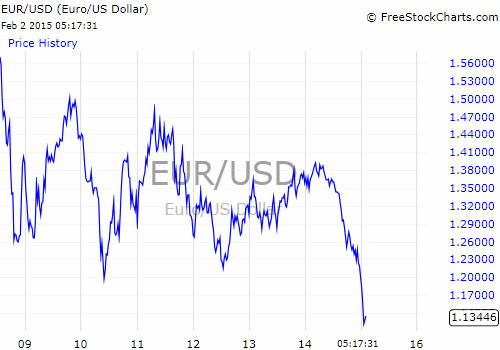

The prospect of this stimulus sent the euro tumbling earlier in the month to its lowest level against the dollar in a decade. Draghi had suggested in September that the ECB could add as much as e1 trillion to its balance sheet.

This was a major step up for ECB as the scale of previous stimulus measures had been small. In contrast, the three US QE programmes of bond purchases that ended in October quadrupled the Fed’s balance sheet to more than $4.5 trillion. Whilst this programme exceeds market expectations it is way below the size that seems to have worked in the USA and UK. Will the ECB succeed, not without an accompanying reform of the whole European Banking system?

That will probably come soon, unless of course Greece derails the process.

Greece

The Greek General Election was won by the left wing Syriza party who were elected on a mandate to get Greece’s debt burden reduced and austerity measures overturned. This has placed them on a collision course with the EU and ECB. The danger is that both sides could end up as losers.

The consequences for ordinary Greeks of a “Grexit” from the euro would be very severe.

Equally the impact of a Greek default on the already tight European credit markets could be just as bad. Syriza will be hoping to achieve some concessions, so far there have been a few conciliatory noises from Angela Merkel, but it can surely be no coincidence that ECB QE was announced just before the Greek Election and that it won’t start until March.

The Europeans do seem to have been planning for this possibility. Both sides are playing “hardball” but the Greeks have proposed an imaginative debt restructuring idea.

The normal European pattern is that this disagreement will continue on the surface for some time and then some face saving arrangement will be put in place.

The Germans don’t want to lose money, nor do they want to set a precedent for other struggling economies, but the Greeks can’t afford to repay the debt. As usual this all adds to uncertainty which is not good for markets, it is a case of déjà vu, but we should remember that the most pessimistic outcome rarely occurs.

For the markets the Greeks may bring a short term shock or two but they won’t derail the main driver of share prices and that is corporate earnings.

US Corporate Earnings

The good news is that the major support for global equity markets, US corporate profits, continues to grow.

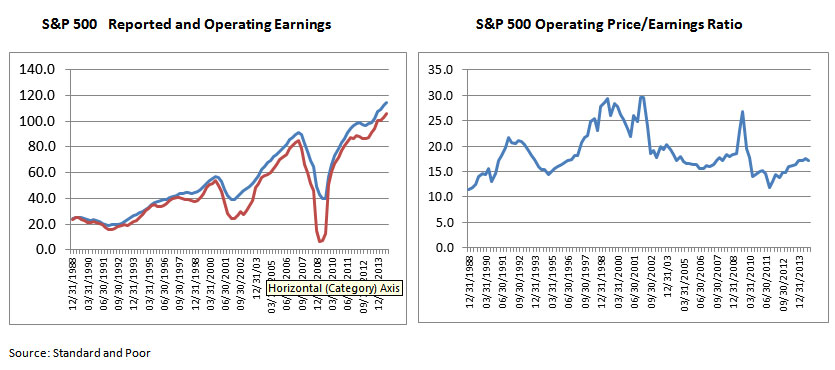

We are approaching the end of the 4th Quarter 2014 results season and the reported numbers have generally been very good.

This time last year forecasts were that US companies would generate 10% profit growth, they actually achieved 18%. For 2015 expectations are again low, oil companies will have a poor year and the strength of the dollar has led to a series of pessimistic forecasts.

However, expectations are still for a 7% increase on the 2015 numbers which is very respectable, especially when inflation is so low. The key value measure, the P/E ratio, also remains low by historic standards.

If Europe can finally begin to grow again (it represents 20% of US corporate profits) then it will provide a major boost to global earnings. Despite all of the geopolitical risks that are around the trend in multinational corporate profits remains upward, which is good news, as is the market valuation. Ultimately this means that shares remain fundamentally cheap.

Markets

We have experienced very choppy trading so far in 2015; Greece is threatening to negate the benefits from the European QE programme. We should expect some “horse trading” between the two sides for some months, Greece has already offered a form of debt to equity swap.

Oil seems to have stabilised and whilst this will act as a deflator for a few months we have to remember that the inflation calculation moves with time, any pick up in oil now, will in the months ahead, be manifested as rising inflation.

So whilst the deflationists are back out in force their justification for taking this extreme stance could disappear literally overnight. We have to

be dispassionate, until we have hard evidence to the contrary then our view has to be that the cycle remains intact. Lots of things may happen in the future but we can’t invest on this basis, we have to follow what we know, and that is markets are good value, earnings are rising and Central Banks “have our back”. There are lots of geopolitical issues around, any of which could cause a short term shock, but long term the cycle keeps running and therefore ultimately so should share prices.

December 2014

Click Here for Printable Version