The first quarter of 2015 has now passed and for UK investors it has been another good one, it also marks six years since global stock market bottomed in 2009 after the disastrous “Credit Crunch”. This remains perhaps the most mistrusted bull market in recorded history.

Why?

There is a belief that the entire rise so far has been based on financial engineering. Everyone believes that it’s a by-product of the US Federal Reserve’s extraordinary monetary policy actions rather than the by-product of fundamental economic growth and productivity, and what the Fed giveth, the Fed can (and is) taketh away.

There perhaps is some truth in this but it does ignore the real hard fact that corporate profits did rise significantly and valuations were way below average.

Having said that the quarter did show what QE can do to markets. We now have a divergence of economic policy amongst the mature western economies.

In the USA, QE has ended and interest rates will probably start rising shortly. In Europe, QE is just getting going. In local currency this meant that the US S&P index was unchanged over the quarter whereas Europe in euros was up by 18%! However, when we translate these returns back into sterling the S&P returned 5.5% and Europe 10%.

So as the cycle gets even more mature where do we go from here? As ever company profits are the key.

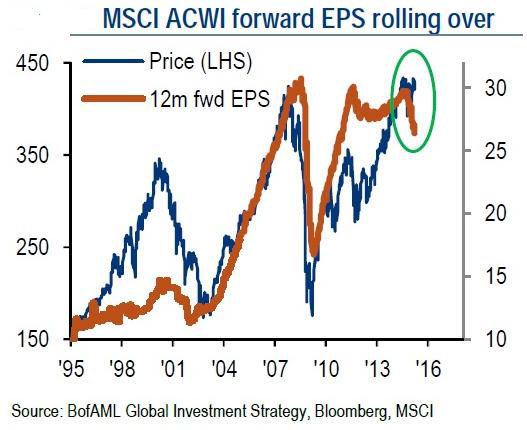

Forecast Corporate Profits

This chart from Bank of America shows the World Index and is based on forecast profits rather than historic reported figures. The pattern is very similar though as forecast profits rise so do share prices.

The oddity was the “tech bubble” period in the run up to Y2K.

The issue is that in all areas bar Europe forecast profits are falling. Oil companies are suffering the most but exporters and those companies that

report in US Dollar are being impacted.

This may yet change if the US consumer finally starts spending again. But what we can say is that after 6 years the dynamics of the bull market seem to be changing.

“The trend is your friend”

Having identified that the dynamics may be changing, markets are like super tankers, it can often be difficult for the trend to alter. The big investment institutions buy shares on a steady drip feed basis, often only reviewed quarterly.

They daren’t buy hugely expensive bonds; get no return from cash so despite the worries over earnings they could keep on buying, knowing that they get a circa 3% dividend yield, a significant return above inflation, plus the probability of long term capital growth as well.

The price for this is volatility and some elevated risk. On this basis the trend could well continue for a while yet.

Germany

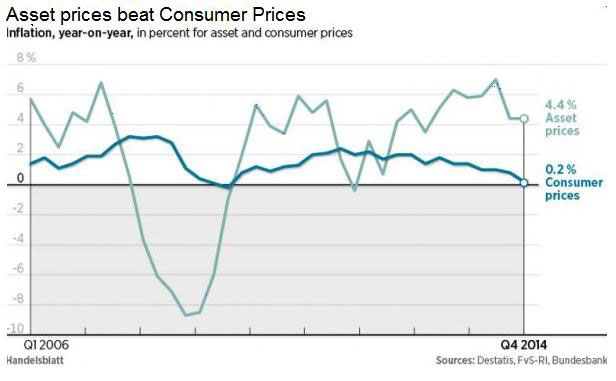

The Germans prevaricated for 6 years about QE; it was perhaps the threat of a Grexit that finally pushed them to accept what is an economically uncomfortable step for them to take.

The spectre of 1920s hyperinflation and the ensuing rise of the National Socialists still dominate the thinking in the Bundesbank, so any sign of inflation may yet see the Bundesbank exert influence on the ECB and QE in Europe could be cut short, regardless of what it may do to the peripheral economies.

whilst consumer prices are flirting with deflation, asset prices are increasing sharply.

Property in Germany is regarded very differently to the UK; houses are seen as somewhere to live rather than as a means of creating or storing wealth.

Stimulating housing is not a tool of monetary policy, whereas in the UK getting “house prices up” is now the key stimulus for the economy. If there is

any sign of a “bubble” in German house prices then the Bundesbank will quickly pull the rug from under the ECB’s QE programme.

Saudi Arabia/Yemen/Iran

A new development during the month was the Saudi Arabian led intervention into the civil war in Yemen. This caused some surprise as the Middle Eastern countries tend to avoid direct conflict whenever they can.

What makes Yemen different is that it is geographically close to the Saudi oil fields and its people are from the same Shia tribal groups that dominate the Saudi Oil regions, in marked contrast to the Sunni leadership in Riyadh.

An overthrow of the Saudi supported Sunni President in Yemen by Iran-backed Shia rebels is just too dangerous for the Saudis to ignore. In the wider context Iran seems to be resurgent, nuclear talks with the West have already made some progress; sanctions are close to being lifted. Whilst in Iraq, Shia militiamen with Iranian “advisers” are pushing ISIS back.

Iran and Saudi Arabia are old enemies, any sign that the two Middle East super-powers are going head to head will not be good news.

Especially as any move up in the oil price from here would also tick the inflation calculation upward.

Markets

We have said many times in this newsletter that the ultimate investment question to any global crisis or event is “what impact would this have on a global multinational company and its ability to generate profits and pay dividends.”

Since 2009 growing profits and rising dividends have supported this hugely mistrusted Bull market. Our concern is that the current statistics suggest that this key support is coming under pressure from the strong dollar. Now this may be transitory, the Democrats need a booming US economy as they head into the US Election, and the inexorable rise of the Dollar seems to have stopped for now.

April will see the most watched US corporate earnings season for some time. The markets need good numbers and forward guidance from company CEOs. In the UK the Budget has barely impacted on the polls and the Election has so far had a limited impact on the FTSE.

But then again most of the profits of the FTSE constituents come from abroad; the UK for many companies is a sideshow. The choice for the City is a possible EU “Britexit” from the Conservatives or a “Scotexit” from the UK from a Labour/SNP combination.

But against this we have to apply the above corporate profit/dividend test and when we do that it is the Dollar and US/Global growth we really need

to worry about rather than UK politics.

April could be a tricky month, corporate deals such as Shell/BG, Fedex/TNT and ECB QE are helping but we may get an answer to the critical question, how robust are US corporate earnings?

March 2015

Click Here for Printable Version