Click Here for Printable Version

This is the time of year when investment managers look back on what happened in 2016 and make forecasts for the next twelve months. The odd aspect of this now traditional occurrence is that in investment terms both last year and the present year are irrelevant.

Last year is in the past and investors, as long as they have taken the correct advice and structured their wealth appropriately, needn’t worry about what 2017 may bring.

It is how these years fit into the long term trend and market pattern that is important.

We can’t get away from the fact that markets move in cycles and this present one by historic standards is long in the tooth.

We may sound like a stuck record but we are investing not in economies but 600 plus global multinational businesses and receiving our share of their profits. Cycles turn because of the possibility of an impending recession which causes these profits to collapse so share prices have to reprice to reflect this fact.

So we have to ask ourselves, what is likely to happen to these profits over the next few years, are they likely to collapse?

There is a risk that in the short term the rise in US market interest rates may create a short US recession before Trump can start his reflation strategies.

In the medium term however, the election of Donald Trump has ripped up the script the investment world has been using since 2009; it could be a very exciting Presidency for company profits.

Nevertheless, his personal reputation does create nervousness and markets don’t like any more unpredictability than is strictly necessary.

We also know that the consensus view is rarely correct, the Brexit vote and US Election were classic examples of the market pricing in what the media were reporting rather than looking at fundamental facts.

The markets are lazy, they like to join in and agree with the prevailing conversation rather than asking is it right?

By doing this it creates mispricing and thus volatility. The current opinion is that Trump might not succeed, the UK will lose out from Brexit, emerging markets will suffer from dollar strength and that Europe will somehow avoid the populist wave and will keep muddling on through.

The “talking heads” tend to lean pro-Europe and anti-Trump.

We nether agree or disagree with their stance but use it to formulate a view of which way the consensus is leaning and is thus likely to be wrong!

The Economic Background (Source Trading economics)

This table shows the current global economic position, which is pretty good. The big three populations centres the USA, China and India are growing nicely and if we annualise the most recent quarter GDP growth figures, are accelerating. Europe and Japan are still flirting with deflation; Russia and Brazil are commodity economies and have been hit by oil’s decline.

The US numbers point towards a return to normal levels of growth and inflation for the world’s biggest consumer market, and this is before Trump takes control.

But, history tells us that with growth and inflation at these levels, US interest rates should be at approximately 2.0% not 0.75%.

This is a huge variance and one of the key risks for 2017. In the UK the picture is muddied by the lack of clarity over Brexit, but again with growth at 2.2% and inflation at 1.2% Interest rates should be at least 1%.

US Interest Rates

There are always two types of interest rate, the official rate set by the Central Bank and the market rate set by the yield on a country’s national debt.

It is the latter that dictates business loan and mortgage rates. The US economy was already picking up before the Presidential Election and the yield on the 10 year US Treasury Bond had started to increase.

From a low of 1.3% it moved ahead of the election up to 1.8%, and post Trump ended the year at 2.45%.

This effectively prices in inflation of 2% and growth of 3% to 4%. But a move of this magnitude has consequences.

Borrowers looking to refinance their mortgages (a common practice in the US) could have got a fixed 30 year rate of circa 3.4% in August now they would be paying 4.1%.

This is another sign of normalisation, and would be fine, as long as wages in the US are rising to compensate consumers for the reduction in their spending power.

If not then rising rates and a fragile job market could precipitate a fall in the US housing market just at the wrong time, and thus raise the risk of a short recession.

This would not be what Trump supporters voted for, but for Trump he could always “blame it on the other guy”. It may yet suit him to “ride to the rescue”.

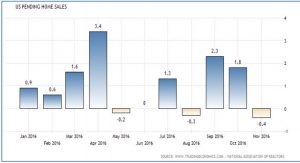

The most recent data is not good news. As the following charts show, both hourly earnings and pending home sales have dipped, just when they should be picking up.

Trump

For the multi-national companies we invest in its all about Donald Trump, will they be invited to the reflation party?

Since 2008 the dominant business strategy has been about cutting costs, hoarding cash and not investing in new factories or new technology.

Why?

Well there is no top line growth as the global consumer is not spending, which in turn was because they were paid less and scared of losing their jobs.

That is true deflation, a spiral down to be the cheapest producer. Buy your competitor and close down their factories.

Thus the net result is a “hollowing out” of industrial capacity and no growth. Trump has the potential to change the game by changing business attitudes. No one wants to be the Chief Executive that fails to catch the bounce in his or her market; Trump has brought optimism to the global business world. The political world, with hindsight, made a huge mistake after the Credit Crunch of 2008/9.

The likes of Obama, Merkel and Cameron correctly blamed capitalism for the crisis but instead of allowing it to right its wrong sought to emasculate business with greater regulation and central control.

They should have let capitalism heal itself, create growth and then regulate.

Instead all Obama and Cameron did was maintain their core populations in genteel poverty.

Voters always vote with their wallets, as the Democrats and David Cameron found to their cost.

Trump (and the Brexit vote) recognised this and tapped into a huge anger that the media had either missed or chose to ignore.

Capitalism and the US corporate world now havea champion, one whose party controls both Houses of Congress and has appointed a Cabinet full of hugely experienced and successful businessman, not career politicians.

The global economy, not just the USA, as the US consumer dominates global retail sales, now has a golden opportunity to grow again and start creating wealth for the majority for the first time in nearly 10 years.

Purely economically speaking (ignoring social and foreign policy issues) long term, assuming he is successful, this is an excellent background for stock markets.

Valuation and Profit Growth

So Trump is offering the markets the prospect of real growth for the first time in many years.

But growth on its own does not mean that share prices will go up. We have to assess whether they are cheap or expensive and if this value represents a fair price to pay for the forecast future growth.

This table from Deutsche Bank takes the current consensus valuation (Price/Earnings Ratio) and places it in a historic context.

Regular readers will be aware that valuations are high and this has been due almost entirely to the collapse of profits at the major oil companies. As oil has recovered then so should their profits.

The recent news from OPEC and Russia concerning oil production cuts is therefore very promising for valuations.

What this shows is that valuations are slightly expensive but not massively so.

If growth does start to accelerate then the forecast P/E ratios will move rapidly to the bottom end of the grey columns and thus become cheap.

Brexit and Europe

The only hard fact we know about Brexit is that Article 50 will be triggered at the end of the first quarter.

Other than that we still know nothing.

This has all the appearances of being deliberate. Brexit is now tied into the series of crucial general elections across Europe this year.

The three core euro economies France, Holland and Germany all have elections and each have a growing and vocal right wing in the political ascendency.

Just one of these countries voting an anti EU party into power will change the dynamic of the Brexit poker game and thus the markets.

There are also UK Local Elections in May, no one can rule out the possibility of a UK snap general election at that time as well.

The various UK legal challenges currently help Theresa May’s prevarication strategy but if they develop to be something more serious she might well go to the country to (possibly) reinforce her position.

The Dutch vote first in March, before Article 50 is likely to be enacted.

A big swing towards Geert Wilders’ PVV party will embolden the Brexiteers, and set the markets up for a worrying French Presidential Election in April.

Markets have not priced in a euro-threatening move to the right in the heart of Europe, but neither have they priced in a reform of the EU that moves it from a Super State back to a Free Trade Bloc.

A move that might see the UK be happy to stay? March and April will be a major risk period for markets.

Blockchain

We are always looking for the latest technological trends that could change the investment world; Bitcoin comes and goes but could be just the starting point of something interesting, just like the internet in the 1990s, who knows where the underlying technology of Bitcoin will take us?

The basis of this alternative currency is the Blockchain.

This records where a bitcoin is at any given moment, and thus who owns it.

This same software could also be used to record the ownership of any asset and then to trade this asset instantly at very low cost.

This has huge implications for the way stocks, bonds and futures, indeed all financial assets, are registered and traded.

Potentially, banking, stock markets, investment banks, money processing and even the legal system face competition from blockchain based technology.

Blockchain tokens will be as good as any deed of ownership – and will be significantly cheaper to provide.

Barclays Bank claims to have provided the first Blockchain based trade finance transaction between an Irish dairy and a Seychelles based company replacing the present document based system that is slow, complicated and thus expensive.

Complex contract conditions could be encoded within the Blockchain and all the corresponding actions automated for a fraction of the cost of drafting, disputing and executing a traditional contract.

Just imagine a Blockchain based house purchase contract? It is possible that Blockchain technology will do the work of bankers, lawyers, solicitors and registrars to a much higher standard for a fraction of the price.

Also if you are in a developing country creating a robust and low cost system of contract law could transform your economy.

The fact that the likes of Barclays are involved means that Blockchain based technology is here to stay and will develop rapidly.

Investment Strategy for 2017

So what are we looking for in 2017? Well if we didn’t have a series of elections across Europe then the outlook would be very positive.

The old world economies have been stuck in neutral with governments unwilling to stimulate and deregulate, relying instead on super low interest rates whilst they increase taxes.

The Brexit and US Presidency votes together have signalled to the politicians around the world that this strategy was simply not good enough.

The investment world has changed.

Prior to 2016 the investment mantra was low growth; low interest rates and they were going to stay “lower for longer”. The strategy therefore had to be, hold bonds and defensive equities such as pharmaceutical companies, tobacco and consumer goods companies.

But post Trump, stimulus and deregulation should create growth, but with growth comes inflation, which is fine, it’s what we need for now at least.

So bonds, which were looking expensive by historic valuations, have to reprice.

If Trump does deliver, then bonds have further to fall as interest rates must rise.

But in the very short term there is, as we have said earlier, scope for short term disappointment, so we may see bonds rally in the early part of this year.

But we cannot escape the fact that the Bond/Equity cycle has swung decisively in favour of equities.

For equities two positive factors are coming into play. Firstly, the oil price is recovering; that helps energy companies’ profits and it also helps those markets in particular that are dominated by oil, such as Brazil and Russia.

Trump, so far, likes to bash the emerging markets for taking US jobs, but if the consumer does start spending again there are many products that the US simply has no capacity to make and remember we invest in companies not economies, Chinese companies could easily move production to the US if it was profitable for them.

The biggest positive of them all is the return of Yield Curve; again this is something we have written about at length before.

Simplistically, a healthy economy needs healthy banks and banks need interest rates at “normal” levels to make money.

Banks share prices have been a major beneficiary of the Trump victory.

But this Trump reflation will be dangerous for some, as we have seen earlier the increase in interest rates is already having an adverse impact on the US economy, and it will take time for Trump to enact his policies.

So given the magnitude of the rally it is more than reasonable to expect some pullback, especially given the unpredictability of the new President.

Could we have a short recession in 2017 and thus the start of a whole new cycle? It is certainly not priced in so we must regard it as more than a possibility.

As we have said earlier it may suit Donald Trump nicely.

Traditionally cycles do turn in the first year of a US Presidency and certainly no-one is looking in that direction.

For 2017 the short term looks particularly confusing, the market’s euphoria over Trump may actually tip the US economy backwards, at the same time the risk in Europe will build in March and April with the Dutch and French elections and Article 50 all occurring in a short space of time.

The medium and long term though look better than at any time since 2008. Trump promises a new paradigm of Thatcher/Reagan style stimulus and deregulation.

Other countries will have to follow suit or get left behind.

Markets over the long term go up in a consistent uptrend, but in the short term this trend is made up of periods of

volatility The QE period has dampened this volatility, it has not been normal.

With Trump arriving normal service (i.e. volatility) must be resumed. 2017 will be dominated by European elections, but having said that, the long term background has just got a whole lot better.

December 2016

Click Here for Printable Version