Click Here for Printable Version

“Perhaps for the next six months” was no doubt met with a collective groan from everyone in the UK. Hopes that this pandemic would follow the historic influenza and recent Chinese/Far East experience have, for now, been dashed.

Restrictions on personal movement have though, crucially, not been matched with restriction on the majority of business activity.

The exception, of course, remains those customer facing industries such as travel, hospitality etc. which have been brought to the edge of bankruptcy.

For many, restrictions over the critical Christmas trading period will tip them over the financial edge.

This is not just a UK problem but is mirrored across Europe, new infections are also starting to grow in the USA as well. But, from a market perspective, this was expected, a winter second wave and also a pick-up in infections as schools and universities reopened was priced in.

The problem we may have is that this is all coinciding with two other potentially market distorting events i.e. the US Presidential Election and the latest round in the fractious UK/EU trade negotiations.

During September markets did start to price in a more pessimistic outcome for each of these events.

Pandemic Progress?

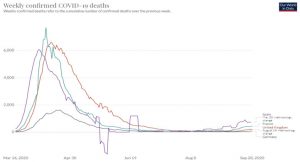

Clearly across the world new identified Covid-19 infections are accelerating.

It would be logical to assume, that as infections rose last time the stock indices went down and only started to recover when the new infection rate peaked and then rolled over. That does not appear to be happening now?

The reason can be explained by the above two charts. Firstly, mortality rates, thankfully, remain low.

The argument here is that more cases are being identified through greater testing and it seems that new infections are being concentrated amongst the younger age groups, which tend to be less medically impacted by the virus.

This means that the economically damaging total lock-downs have not been reintroduced.

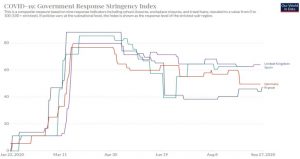

The second chart shows an index of how stringent government movement restrictions are.

What is interesting is how similar they are across Europe and also the degree of restriction at present is less than during the initial wave. What is also interesting that whilst there is increasing pessimism surrounding the pandemic there has been positive news on vaccines, treatments and testing. For the hospitality industry the, very recently introduced, automated 15 minute tests from Abbott Labs and Becton Dickson could be game changers.

On top of this positive testing development, if a successful vaccine is identified then markets will bounce strongly.

Even though it could take a while to be physically available it would crucially put an end date into the market’s price discovery equation.

US Presidential Election

The U.S. Presidential race, at present, is probably much closer than the national opinion polls suggest. A recent Reuters/Ipsos opinion polls in the battleground states shows that Democrat Joe Biden has only a slim lead over President Donald Trump in three highly competitive States and in a dead heat in three others.

These State polls, conducted earlier in September and before the recent TV debate, found Biden and Trump tied among likely voters in Florida and North Carolina.

With Biden leading marginally in Arizona, Pennsylvania, Wisconsin and Michigan. Like the UK, US elections are not won in the metropolitan areas but in the farming and old industrial areas. For the markets, whether it is Trump or Biden doesn’t really matter, what is needed is a decisive victory one way or the other.

A close result like the 2000 George W Bush/Al Gore election that led to recounts and legal challenges and took over a month to be decided, would not be well received by the markets.

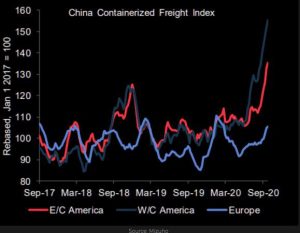

Global Economic Recovery

(sources: Mizuho and JP Morgan Chase)

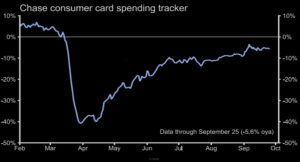

Importantly, the global economy and especially the US consumer continues to recover quickly.

The first chart shows Chinese exports to Europe and US East Coast(E/C) and West Cost(W/C) ports. Despite the continued trade war there has been a dramatic increase in exports to the US.

This is not typical of an economy dropping further into recession. Similarly, US consumer spending continues to recover strongly. Now if the virus takes further hold and if total lock-downs are reintroduced this may well reverse, but for now economies (and there are similar patterns in the UK) are outperforming all expectations.

This may yet cause the Federal Reserve Bank a problem.

They calculated that US Personal Income would fall by 10% in 2020, hence the magnitude of the monetary stimulus.

It is now looking like the impact might only be 3% to 4%. Have they printed too much money? That ultimately still depends on just how many jobs are going to be lost over the next few months.

UK Stock Indices and UK/EU Trade Deal

(source: FTSERussell)

The UK/EU trade talks have a deadline of the end of October but few believe an agreement will be reached just yet.

Indeed, there could also be no deal with a series of temporary measures whilst they keep on talking!

For the UK stock market, bad trade news could be good news, as long the pound is weak. This table shows the reason why, within the top 10 of both the main FTSE UK indices there are very few companies that would be impacted significantly by any trade disruption, but many are big gainers from a weak pound.

Markets

As long as the Fed keeps printing money markets have a back-stop. Clearly, there are fears surrounding the election and rising infections and these are outweighing the possible positives that might be out there, such as a vaccine, quick and easy Covid-19 tests, even a last minute US Fiscal Stimulus programme.

We need to be aware, as we enter the seasonally weakest period of the year, that if some of these negatives are resolved one way or the other markets will have to reprice.

Between now and Thanksgiving is often a tough period for markets and there are more than enough big issues to deal with over this quarter.

However, because of the Covid-19 news it would be easy to become too pessimistic, we need to remember negatives can very easily turn into positives.

For markets it is not about the virus but the lock-downs, anything that helps to avoid further economic restrictions would be good news.

October 2020

Click Here for Printable Version

This information is not intended to be personal financial advice and is for general information only. Past performance is not a reliable indicator of future results.