Click Here for Printable Version

As we enter the final three months of 2018 the main investment markets have so far delivered varying capital returns. Helped by the mighty dollar, the US is up by 13.4% whereas the other major markets are down, including the FTSE 100 by 2.5%, the German DAX by 4.4% and the Emerging Markets by 6.3%. Gilt prices have also fallen by 3.6%.

So the investment world remains very Trump centric, part of this is down to the currency and part to the nature of the US equity markets. The FAANGs (Facebook, Apple, Amazon, Netflix, Google) dominate the US indices and continue to grow rapidly and generate huge sums of cash.

Only China has companies remotely similar (Alibaba, Tencent etc.). The US is also the only major mature economy where interest rates are “normal” and has an economy not dependent on QE.

This will ultimately give the rest of the mature world, especially Europe and the UK, a problem as the US Investment Cycle will undoubtedly turn down before they have fully recovered.

When will this be?

That depends on inflation, as we keep saying “Bull Markets don’t die of old age they are killed off by Central Banks” in response to rising inflation. So the real question is what is the outlook for US inflation?

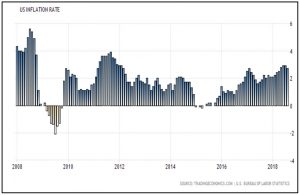

Inflation

This then precipitated a fall in house prices and thus bond defaults.

Since then inflation has been roughly 2.5%, which is fine.

However, what we haven’t had is wage inflation which is normally the precursor to a jump in retail prices. This has seemed odd as US unemployment has been falling rapidly.

But since Trump arrived, jobs growth has accelerated and there are now staff shortages in some key areas such as trucking and construction.

As such we are now seeing wage inflation pick up to 2.7% and likely to go higher still. Economic statistics tend to take time to change direction but then can accelerate quickly.

This does not bode well for price inflation in the USA.

The other big impetus to inflation will be oil, crude oil prices are rising.

Brent Crude

It is the correct trend and the current fund price equates to about $85 per barrel.

This price rise reflects Saudi Arabia controlling supply as well as Venezuela’s economic implosion.

More recently Trump’s very aggressive speech at the UN, which specifically targeted Iran, has removed the possibility of an early Iran nuclear deal and thus Iranian oil coming back onto the market.

Clearly, this helps oil company profits and the US shale producers in particular.

But it will also have an impact on US gasoline prices and is thus inflationary.

From the chart it looks as if oil prices have further to rise. It follows therefore, so must US inflation and then so must US interest rates.

This all increases the future recession risk.

Italy

We have highlighted before the risk that the new Government of Italy poses to the whole euro currency project and could possibly precipitate another credit crunch.

This will not be an overnight process, it will be a slow burn in the background of the global bond and equity markets.

However, the initial fears have come to pass. The Italian populist coalition government has defied the EU and apparently set a budget that is in excess of income by 2.4%.

This prompted a sell-off in Italian government bonds and some European shares.

What is worse is that they haven’t specified what this expenditure will actually be spent on.

Talk is of increased pensions and the worrisome Universal Income.

However, as ever, Italian politics is unpredictable, there are many stages to come before this can be considered a crisis.

The Italians have until the 15th October to send their complete proposed Budget to Brussels. It then has its first reading in the Italian Parliament around the 20th of October, at that point the bond rating agencies will decide whether or not to downgrade Italian Government Debt. The crunch with the EU won’t happen until the 30th November deadline when Brussels has to decide whether to accept or reject this proposed excess spending.

Given that this process will involve Italy and the EU this is unlikely to be smooth.

Trump and trade

Another month, another trade deal or two in the bag for President Trump.

South Korea and Canada have joined Mexico in signing new trade rules and tariffs with the USA.

What is remarkable, as we saw last month with Mexico, is how little has actually changed from the previous trade agreements.

This raises hopes that separate deals with China and also the EU could be relatively easily negotiated.

The big one is China, as it is not just about trade, but who is the biggest kid in the class.

Labour and Jeremy Corbyn

The Labour Party annual conference gave us a little more clarity on what exactly would be the policies of a future Labour Government, should it happen.

The big headline grabbing policy is renationalisation of the utility companies and the railways.

The market’s main fear is how will it be paid for.

The second major headline related to Brexit, Keir Starmer seemed to go “off script” in calling for a second referendum as it isn’t official party policy.

This seems to be that Labour would vote against whatever deal Theresa May comes back with as it prefers a General Election, preferably before the constituency boundary changes take effect.

This fact may actually help the PM as Brexit rebels of both the soft and hard persuasions may choose to back her final deal rather than risk an election loss.

What lies behind Corbyn’s “confused” Brexit strategy? There seems to be two aspects, firstly to gain an overall majority Corbyn needs to win back the Brexit-voting English working class areas, yet retain his new remain-focussed supporters in London, a very difficult balance, hence better to say nothing.

His other problem is that his flagship renationalisation policies may be technically illegal under EU Law.

For example, in France, the EU is forcing the privatisation of state owned SNCF railways under the new Market Pillar Directive. This potentially gives him a policy problem.

So Corbyn needs to decide which is more important to him, re-nationalisation or a very soft Brexit.

Given his personal historical voting pattern our guess is that he will put taking back the utilities into public ownership first.

The danger for the UK economy is that under a “No Deal” Brexit where all trade takes place under WTO tariff arrangements, Corbyn, instead of signing a series of free trade deals and thus negating the initial detrimental set-back of a very Hard Brexit, decides to keep the substantial extra tariff revenue.

A Labour government would be very hungry for cash and the billions of extra trade tariff and VAT revenue would be hard to resist.

That would be the worst of all worlds for the UK economy. A Hard Brexit under the Conservatives would be short term bad, hopefully, if the right policy decisions were taken, long term good for the economy.

Under Labour a Hard Brexit might just be bad.

Markets

October is the market’s bogey month, sitting between the end of Summer and the US Thanksgiving holiday, this period is usually one of immense volatility.

At the company level we the get the third US corporate quarterly results season which should continue the trend of this year and be spectacularly good.

At the macroeconomic level, the major areas of the world are diverging. The USA has “normalised” economically and is growing nicely, US interest rates will though have to rise much further as wages and inflation start to accelerate.

This mean that this cycle is now officially a normal one and thus will come to an end, as all ultimately must, in recession, but not just yet.

China is being impacted by trade sanctions; some of the Emerging Markets are being hit by a double whammy of a strong dollar and high oil prices; Europe will at some stage have a major problem, Germany is booming, the rest of Europe isn’t, for which area will the ECB set interest rates?

We are already seeing this divergence in market performance and this is likely to continue.

The dollar and US interest rates are always the key, but all could turn on a sixpence, that will depend on a China trade deal.

Nothing will happen ahead of the US mid-term elections next month, but as Trump says, he has now “cleared the decks” to deal with China.

The markets still believe a deal will be done and the nature of the Canadian and Mexican deals suggest they are not wrong.

October, is always a nervous month and with markets so high and bond yields rising this will be even more nervous than usual.

The short term news flow out of Italy and Trump/China will be the key to how markets will move over the month.

October 2018

Click Here for Printable Version