Click Here for Printable Version

As one quarter ends and another begins the underlying patterns within markets have so far remained constant.

A bounce in the pound hurt returns during September but over the quarter UK and Global equity markets made gains of about 1%, Gilts were marginally down and the Far East/Emerging markets up around 3%.

There remains an immense cacophony of geopolitical noise, but for markets the key news came just before month end, Trump’s long awaited tax cuts were announced.

These have the potential to provide a healthy boost to US corporate profits and thus bring elevated share valuations down. Much depends on Congress; can he get them passed without being severely watered down? Only time will tell, but so far they seem to have received tacit political approval but the markets have not raced away suggesting they remain, for now, unconvinced.

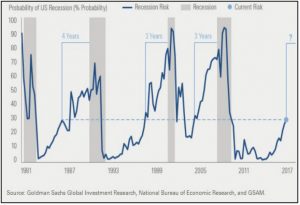

The Cycle…….Again

Source: Goldman Sachs

These charts from Goldman Sachs show that we are currently in the “healthy” part of the cycle.

As we have said before the economic ducks are all lined up. Growth remains anaemic but seems to be picking up.

The hurricanes in the US are a personal disaster but an economic benefit. If Trump can finally get his tax plans through, there is scope for economic growth to accelerate.

The table on the left shows the result of PMIs (Purchasing Manager’s survey Index) for the major economies.

A figure above 50 indicates economic expansion. All, even the UK, are in expansion mode. The second chart shows Goldman’s Probability of US recession which, based on current data, remains very low.

They even suggest that the next US recession may be up to 3 years away, which is good news.

But we must remember that ….

We have already had rumblings from the Fed that they are inclined to raise US interest rates to a level higher than the bond market is currently pricing-in.

Despite falling property price and Brexit uncertainty Bank of England Governor Mark Carney seems set on raising the Base Rate as well.

Inflation is the key; whilst it stays stubbornly low this will be just talk, if it picks up then so will rates.

Florence/May/Brexit

Theresa May made an important speech in Florence which gave the markets a rough outline of the current British

Government’s stance on the Brexit negotiations.

In a nutshell it is a classic political fence sitting exercise of trying to keep Hard, Soft Brexiteers and Remainers happy.

For the Remainers, there is a two year holding period between EU membership and non–membership.

During which time public attitudes may change or alternatively Jeremy Corbyn “rides to the rescue” (even though he is a Brexiteer, it will suit him to say he is not).

For the Softs, it is essentially status quo but with some return of political decision making to London (the half in-half out route).

For the Hards, it doesn’t really matter either way. They will vote in Parliament against whatever is agreed, assume Labour will back them, and force a no confidence vote and thus a General Election.

For the markets the pound rallied on the Florence speech so we must assume a Soft Brexit is now what the markets are pricing in.

This however gives us a problem. In markets the “herd” is rarely right, as such, we need to ask ourselves what happens if they are wrong.

Economists

There aren’t many in the investment establishment who are in favour of Brexit, but there is a group of highly experienced and interestingly historically accurate economists who do prefer a Hard Brexit on purely economic grounds.

So we have the herd on one side and small group of outliers with diametrically opposed views.

Given the high probability that Parliament might reject any laboriously negotiated Brexit deal, we do need to look at what the consequences of such a decision would be. Professor Patrick Minford is the most widely quoted of this group of economists but there are others such as Roger Bootle, Neil MacKinnon and Gerard Lyons.

None have any real political axe to grind and all have decades of experience and crucially a demonstrable track record of economic forecasting.

The crux of their argument is that the EU is a protectionist organsiation implementing trade barriers that hinder economic growth.

According to Minford eliminating EU protection, would reduce UK prices by 8%, and thus would transform the competitiveness and productivity of UK business.

Together with free trade deals, Minford’s models suggest a boost to UK GDP of 4%. Reducing regulation would add a further 2%.

None of this is rocket-science; it is basic economics. It was the basis of Adam Smith’s 1776 textbook “The Wealth of Nations” and the Free Trade League which precipitated the Industrial Revolution.

We have no idea whether they are right or not, and much will depend on politics and subsequent policy actions, but it does highlight that if the herd is wrong then the alternative is perhaps not as bad as they are suggesting, indeed it could, in the long term, prove to be very profitable for the UK.

Uber

The Fourth Industrial Revolution is only just starting to happen but the London Mayor’s decision to withdraw the operating licence for this disruptive taxi service gives us an insight as to how difficult the new revolution is likely to be.

No doubt a compromise will be made, especially given the public outcry from Uber users, who incidentally are mainly from the Labour Party’s target demographic.

However, there will be many services in the future that will be impacted by technological change.

Black cabs v Uber will be the first of many such conflicts as traditional skill based services are replaced by new technology.

What seems clear is that ultimately the consumer will be the final arbiter, just as it was in the 19th Century when technology reduced the price and increased the availability of fabric.

Germany, Europe and Catalonia

As expected Angela Merkel won the most votes in the German election but, just like Theresa May, didn’t win as many as she thought she would.

Left and Right Wing parties gained ground, which shouldn’t be surprising given the refugee/immigration issues that Germany is experiencing.

But for the markets, after the Dutch and French election results had moved European politics to the centre ground, the assumption was the Germans would also fall into line.

The fact they didn’t has ramifications.

Merkel at the time of writing has yet to form a coalition, it is expected she will do a deal with the Liberals and the Greens which may lead to a less EU friendly Germany.

At the same time this result will loom large over the forthcoming Italian General Election.

Italy is the most Eurosceptic euro group member and has the Catalan style separatist Northern League.

The potential for a euro group break up has not gone away; in fact it can be argued that following the events in Germany and Catalonia the risk level has just been raised.

Markets

Historically October is a stormy month for the weather and for stock markets.

We need to watch for inflation and thus the future direction of interest rates.

We will also get the 3rd Quarter US corporate results season.

Earnings should be good and this is before any future US tax cuts boost company profits (and thus bring valuations down).

As ever geopolitics will dominate the news headlines. North Korea, the Trump/Russia investigation, who will be the next Fed Chairman, can Trump get his tax cuts through Congress, will all create news flow.

In the UK, politics and the slowing housing market will be front and centre.

But for markets, which we must remember look 12 to 18 months ahead, it is the actions of the Central Banks that will ultimately dictate share price direction.

For them it’s all about inflation and the fact that globally it remains stubbornly low.

Furthermore, volatility remains at a historically low level, which is not normal, we shall see if October brings normality back to markets.

September 2017

Click Here for Printable Version