October is often the most feared month by investors and traders. The crashes of 1929 and 1987 both occurred in this month, stormy weather is often matched by stormy stock markets. The US Budget impasse raised fears that this October could be similar, but the Republicans blinked first and “the can has been kicked down the road again”, at least until the New Year when we start all over again.

The shutdown of the US government during this argument has however had an impact at the Federal Reserve Bank. Unemployment data wasn’t collected and thus no decision could be made concerning when to start tapering QE3. Furthermore no-one as yet knows what impact sending so many Government employees home without pay will have on US consumer spending particularly as the key US shopping season starts shortly as Thanksgiving Day approaches.

Some recent US statistics such as Home Sales have indicated that US growth is still not as robust as it should be

Investment Scenarios

When we structure client portfolios through the use of a range of assets e.g. Gilts, Bonds, UK Equities etc., this reflects the client’s own needs but also where we are in the investment cycle. Essentially during growth phases we want to be in equities and during recessions bonds are preferable. As this cycle is progressing equities have started to overtake bonds just as they should. However, whilst this appears to be a “normal cycle”, QE and other hangovers from the Credit Crunch mean that we have to constantly reassess where we are in the cycle and ask ourselves the most dangerous words in investment i.e. “is it different this time?”

Essentially we have 3 “scenarios” that may come to pass with varying probabilities of likelihood.

The Doomster Scenario. The pessimists, who dominate the media’s attention, as bad news sells, suggest that the global economy is entering a Japan style phase of long term deflation and low growth. Current growth levels are only being generated because the Central Banks are flooding markets with cheap cash. However, governments are so indebted that this support cannot go on for ever and when it ends so will the growth, leaving economies burdened with Greek style debt, high taxes and no growth. This is certainly possible and has indeed happened in Japan. But as we have said many times before just using one economy as an example is dangerous and Japan’s problems are due primarily to a shrinking and ageing population.

The Goldilocks Scenario. This is the normal cycle, not too hot, not too cold. This is what governments and central banks aim for and in a cycle of 5-6 years. Why? Well because elections such as US Presidential and UK General are every 5 years. Politicians always like to engineer a boom just before the electorate cast their votes. Why did the Coalition introduce the Deposit Funding scheme when they did, we have known about the mortgage problem for the past 3 years? Central Banks are getting much better at managing the cycle, particularly post Alan Greenspan, so this scenario has to have the highest probability of success and is supported by history.

It doesn’t make good TV, but the logical stance has to be that this cycle will be the same as all the other ones.

The Inflation Scenario. This is too much growth and has been rarely mentioned. Economic theory says that if you print money (QE) you end up with inflation, do too much you end up with hyperinflation just as in Weimar Germany or more recently Mugabe’s Zimbabwe. This is where you literally need a wheelbarrow full of cash to buy a loaf of bread! But we could also be underestimating how robust the global economy actually is. Stimulating growth is like manoeuvring a super tanker, turn the wheel and nothing happens for a long time, but eventually the ship does turn and pretty quickly. US growth may be about to accelerate just as China is getting going again and Europe and Japan emerge from recession. If this happens Central Banks will be chasing their tails ending QE and raising interest rates.

Our view is that QE will not initially lead to inflation as it is keeping banks alive who are still not lending properly, so the printed money is merely substituting that which has been withdrawn by the banks. However, if QE goes on too long, then we will get inflation, but it is impossible to say when.

For example the inflation of 1970s was partly blamed on the post WW2 Marshall Aid programme. In the global economy nothing happens immediately.

We do have to monitor which of these is likely to pass as each scenario dictates a different mix of investment assets in client portfolios. The Doomster means more bonds and less in equities whereas the Goldilocks and Inflation theories will impact bond capital values. Our approach is to assume that the strategy that has worked consistently over the past 100 years will continue to do so, but be very wary of what may be happening in the global economy. All current evidence supports the Goldilocks theory and thus to take an alternate stance is not investment but speculation.

3D Printing

The development of 3D printing has gone through the classic development cycle i.e. nice idea but what can you do with it? A very expensive “toy” that was useful for prototyping or making one off components for Formula 1 teams is on the verge of entering mainstream manufacturing and becoming a transformational technology. 3D printers work by spraying very thin layers of metal, plastic or even food on top of each other to make highly complex shapes that are currently impossible to cast or machine.

As new materials that can be sprayed are developed and the price of the printers comes down then the potential gets bigger and bigger. The market is dominated by a few specialist US companies, but General Electric and Hewlett Packard are intimating they want to get involved as well. The speed of the printing process seems to be the major handicap at the moment but as new machines and materials are developed this will change.

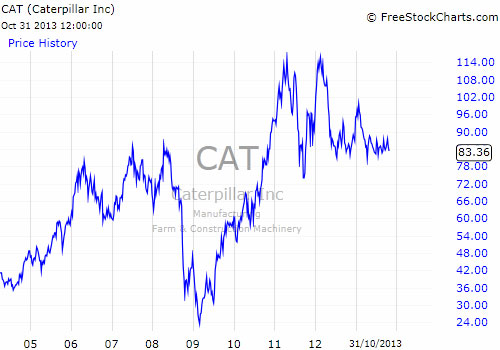

Caterpillar

Whilst it appears that tonnage mined is increasing Caterpillar is not seeing any increase in demand. This may be simply that the mining companies re-equipped during the boom and will not need new trucks/diggers for several years yet? Nor are they developing new mines yet. There was however good news that US construction related sales is increasing; this is a positive sign

for the health of the US recovery.

Begbies Traynor

This company is a well-known firm of insolvency specialists. Such firms traditionally do well in recessions and can offer a valuable insight into the health of the UK economy, remembering that the first year out of recession is normally when most insolvency occurs. They reported that “across all sectors, UK businesses experiencing critical financial problems reduced…supported by significant improvements in the UK’s consumer-facing industries including Bars & Restaurants, Hotels, Food Retailing and General Retail.” This was some extent offset by deterioration in the Services sector, but the overall impression is that in the “real world” things are improving. This is particularly important for the banks, which may yet feel confident enough to start lending again.

Markets

We now enter what is normally a good period for stock markets, as the US consumer spending season starts with Thanksgiving and runs through to the January sales. Expectations somewhat surprisingly appear to be low. Our view is that with house prices rising and unemployment falling consumer confidence may surprise the economists who tend to look backwards with their forecasts. The big unknown in the US is what impact the government shutdown had and whether this will scare the US consumer into keeping their Dollars in the bank rather than spending them. November will also see the Chinese Party Congress where reforms are expected to be announced.

The Chinese markets have been recovering as manufacturing picks up. We will also get the most hotly anticipated flotation for many years, Twitter. Only a small number of shares will be listed in the US but with Facebook and LinkedIn being so successful Twitter is thought to be certain to do the same. Markets though remain well supported by reasonable valuations at a time when earnings growth remains pedestrian. Growth should though begin accelerating particularly if the consumer starts spending again.

31st October 2013

Click Here for Printable Version