Click Here for Printable Version

As 2017 progresses to its conclusion we are starting to get some clarity from two of the big issues facing investors.

Trump is close to finally achieving something tangible and Brexit talks are reaching their first hurdle. However, Trump still faces a major test with the FBI investigation, we had a brief “Fake News” event that scared the market and gave us a clue of what might happen if this investigation ever gets to Court.

We are in the messy part of the cycle, growth is picking up, valuations are high and market psychology is very positive.

The danger is now that the reality has to match the expectation. It should do, there are lots to be positive about in the global markets (not necessarily the UK) but, this part of the cycle is fragile.

It relies on the Central Banks “playing ball” and not pushing up interest rates too high or too fast.

The market is fixating on the Yield Curve.

The Yield Curve

If you place cash on deposit with your bank for say 1 year with no access you naturally expect to receive a better rate of interest than you would get for instant access.

For Gilts and US Government Treasury Bonds the same principle applies.

When you buy a bond (the same as putting money on deposit with the government) the further out in time (say 10 or 25 years) you buy then you would expect a higher rate of return.

But what if over the time frame you are buying you expect interest rates to fall? Then you might accept a lower rate of interest than you would get over a shorter time as this means you have traded short term return for secure reliable long term income regardless of what happens to the economy.

If this longer term rate is lower than the short term rate then the yield curve has become “Inverted”.

This is important as it is normally a very accurate indicator that a recession is coming.

This chart from the Federal Reserve Bank of Louisiana shows the difference in Yields between the US 2 Year Bond and

the US 10 Year Bond.

Below the black line the Yield Curve is inverted and thus predicts a recession (the Grey Bars) in 12 months’ time.

Currently, the difference is narrowing, crucially, it has not yet moved below the black line but it is getting close.

What makes this difficult to use as a predictor is that during circle A it took nearly 5 years to fully invert. But at B, it only took a few months.

The current market view is that the Bull market has two to three years to run, so it is betting on scenario A.

But as ever, Bull markets don’t die of old age they are killed off by Central Banks. With a new Governor, Jerome Powell, the Fed has a new head which adds a further element of unpredictability to an already complicated picture.

Trump and the FBI

Some false reporting by a US reporter led to a brief sharp move downwards in US share prices.

The report alleged that the sacked adviser Flynn, would testify against Trump.

Whilst this proved to be false, it does give us an indication of what may happen when this investigation comes to a conclusion.

Trump remains unpopular within his own party and he may find himself friendless. Whilst undoubtedly this could cause market volatility, it should not lead to a new election.

If Trump ends up being impeached then Mike Pence would become President. He may prove to be more popular with the Republicans and thus might actually be more able to implement Trump’s agenda.

As we write Trump is close to achieving at least one of his objectives, a much watered down Tax Plan might be enacted by Christmas.

This will help corporate earnings and thus the market valuation but is not likely to be the hoped for boost to consumer spending.

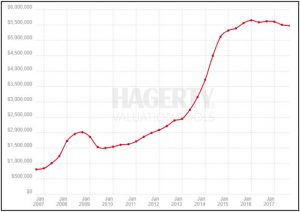

The Ferrari Index

But we know that globally Consumer Price Inflation is low and lower than where it should be at this stage of the cycle, which is odd. But, there is inflation out there, just not where it is expected to be.

This chart from US car insurer Hagerty shows the inflation of the price of classic Ferraris.

The index dropped during the Credit Crunch but as QE was introduced values have increased roughly five fold.

Interestingly, as QE in the US has ended prices have moved sideways.

The hot money has moved on to the art market, a Leonardo da Vinci has sold for a staggering $450m.

There are asset bubbles out there, just not where you would expect them to be. Inflation is coming, we just don’t know when.

Brexit

As the Brexit talks continue their convoluted path we remain of the view that whatever deal is eventually done is effectively irrelevant as it is unlikely to pass a Parliamentary vote.

The inclusion of a fixed date in the EU Withdrawal Bill is an attempt to remove the option of “kicking the can down the road” i.e. have continual talks about talks that keep us in the EU, at least until public opinion changes.

The “soft” deal seems to be the route that is currently being choreographed; however, such a deal is unlikely to be acceptable to the Conservative Party Brexiteers.

Labour is equally unlikely to miss the opportunity to force a crisis/no confidence vote.

So as we progress with the talks, we must anticipate that ultimately this will end in some sort of political crisis and possibly a new UK Prime Minister.

Who that will be is anyone’s guess.

Merkel

In 1890 the satirical magazine Punch published a cartoon of the young Kaiser watching the creator of modern Germany, Bismarck walk down the gangplank of a ship.

The caption was “dropping the pilot”, is Germany about to do the same with Angela Merkel?

After a poor showing in the election, again as we write, she is struggling to put together a governing coalition.

It may well be, just like Margaret Thatcher, her strength is becoming a hindrance?

There might be another general election which could lead to Germany becoming less pro-EU. The main implication of this would be higher interest rates.

Europe, despite being the most popular investment market amongst commentators, to us remainsrisky.

The Italian election is due soon in 2018 and the Eastern European states are increasingly challenging the status quo.

A collapse of the euro remains a significant risk to global markets.

Markets

December is normally a good month for shares. But the Santa rally often has to wait until after Options and Futures Expiration day before it gets going.

This year expiry day is a bit later than normal on the 20th, so with all that is going on the geopolitical world there is the risk that this time Santa may take a bit longer to get his reindeers flying.

Economically, nothing has changed and the background continues to improve. Inflation is a key focus now and will be watched obsessively by the Central Bankers around the world.

If Trump is implicated in the investigation into Russian involvement in the Presidential election or North Korea continues to develop its missiles, then markets might just take the opportunity to pull back. This Bull Run isn’t unusual but will also not last forever.

November 2017

Click Here for Printable Version