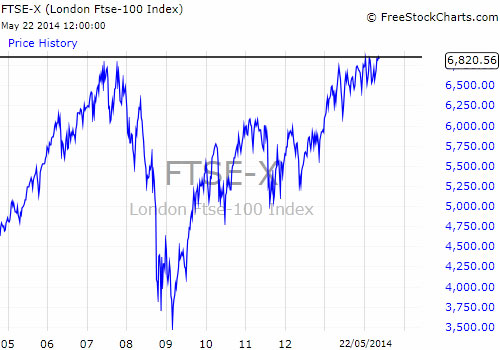

The FTSE remains stuck in neutral. The index has tried to break above 6800 to new highs but has struggled. Astra Zeneca spurning the advances of Pfizer has not helped.

But the real problem is the lack of US growth. Of the companies that make up the FTSE index, few are dependent on the UK economy; it is therefore the direction that the US gives us that is the key. Share markets are driven by corporate profitability and the value that the markets place on this growth, as ever it is the US that sets the agenda.

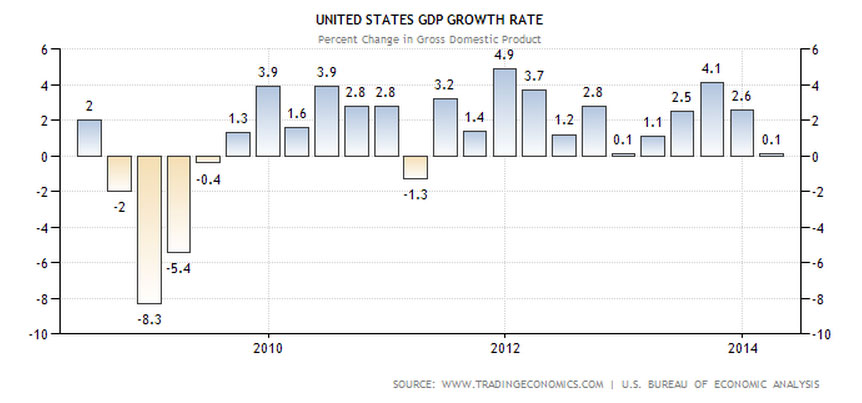

The problem is that US growth is below where it should be and worryingly is showing no sign as yet of returning to “normal” levels.

During May, as the summer doldrums started, there were signs that “hot money” investors were starting to “throw in the towel” and move their short term cash back into bonds, safe in the knowledge that with low growth and low inflation, interest rates are unlikely to rise for some time. Are they being short-sighted though?

Where is the growth?

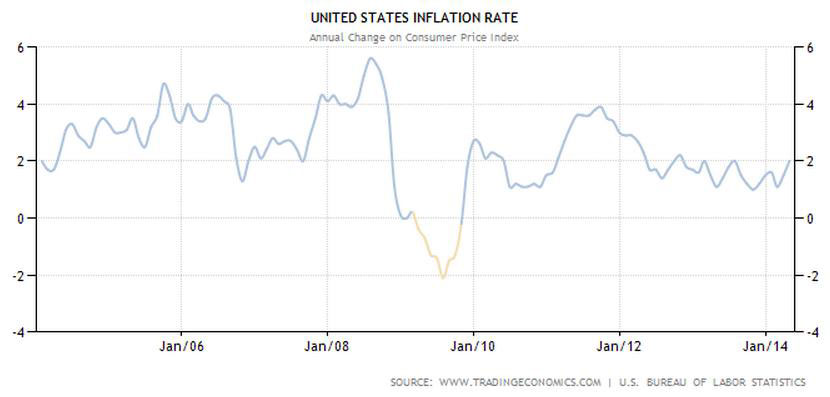

These two charts show the problem that both the markets and the US Federal Reserve Bank have. Growth since the ending of the credit crunch inspired recession has been consistent, which is ok, but normally it gets progressively greater each quarter.

With growth we get inflation, above 2.0% inflation is actually good but when it gets above 4%, which is the long term average, then central banks get twitchy and start to raise interest rates. Around 6% they panic and put up rates to the point where we get a recession, company profits then collapse and so do share prices. Below 2%, then deflation is the worry, the issue is that inflation is on the cusp of 2% yet the Fed is reducing the QE stimulus and recent GDP figures have shown no improvement over last year.

So where is the growth?

US unemployment is going down but this may be due to emigration, particularly back to Mexico where deregulation is causing a mini-boom and also many workers have decided to retire. Many older US employees continued to work so they could benefit from company provided health insurance. With the introduction of Obamacare there is no need to keep working and they are now retiring, thus reducing employment numbers.

So is the US economy creating enough jobs to get growth going?

Many will point to the severe weather of the beginning of the year and the distortion this could have caused; this will now be dropping out of the statistics so we are in for a nervy period, is there a hidden boom going on in the USA? Company profits, again backward looking, say no, but the real test will happen over the coming months. These are twitchy times for equities and the Fed, but as we know “Bull markets climb walls of fear and worry”, it’s when there is nothing to worry about that you should be worried!

Alibaba

The Chinese technology company Alibaba is due to float in the US, possibly in August. Alibaba is a mix of Amazon, EBay and PayPal.

There’s Tmall, an online shopping mall; Taobao, a marketplace where small Chinese companies can sell directly to consumers; and Alipay, a digital payments company that Chinese consumers use through their mobile phones for all sorts of transactions.

Why is this important, it is because Alibaba is an enormous business, and is probably going to be the largest flotation ever? Last year, Alibaba

sold $248bn in goods and is forecast to sell $400bn plus this year, Amazon meanwhile sold $90bn, Ebay $18bn. Alibaba is the biggest e-commerce site in the world’s fastest-growing economy with a potential 1.4bn consumers.

As it functions largely as a marketplace Alibaba’s operating costs are low, and that means it has profit margins of 45 percent, unlike Amazon that barely breaks even.

Analysts estimate that the company’s post-IPO value will range from $136 billion to $245 billion. If it’s anywhere near the top of that range, it means that it will be more valuable than Facebook. Yahoo owns 22.6% of Alibaba. One of the questions analysts are asking is will Alibaba look to expand outside China? In its prospectus the company seems to be keeping its focus at home.

Alibaba points out that China has far less retail space than both the U.S. and Europe, while at the same time online shopping still makes up only 8%

of Chinese consumer spending. Furthermore, Chinese consumer spending in 2013 made up only 36% of GDP, compared with 67% in the USA. China, it seems, has only just begun to shop!

Indian Elections

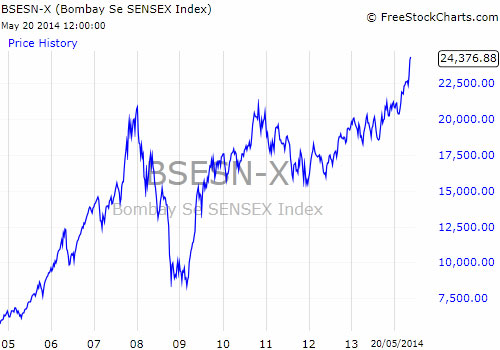

This victory gives Modi a clear mandate to push through his “Gujarat model of reform” which is named after the state that Modi has led since 2002 as Chief Minister. This model targets high economic growth through a business-friendly regulatory environment: investment in much needed infrastructure which will help business development; and a support for capital intensive agriculture, a significant move for India. The Indian stock market has responded by reaching new highs. We now have India as well as China embarking on their next stage of capitalism, the implications for long term global growth must not be underestimated.

Markets

This herd is still grazing at the moment and waiting for some good economic news to arrive. There are high expectations that the ECB will start some form of QE, as signs of deflation are starting to appear across Europe and maybe the Germans will finally allow Mario Draghi to attempt some form of stimulation, better late than never.

The Emerging Markets are seeing better news flow and Brazil and India have been leading the way. For the Brazilian stock market World Cup Fever has arrived! The valuation gap became too compelling to ignore and as the US and UK hesitated the hot money flowed into the cheapest and fastest growing markets.

May 2014

Click Here for Printable Version