Those that sold in May have yet to be proved right with the FTSE up by 2.4%, but the equity and bond markets are entering a critical phase. Markets are currently being driven by various global QE programmes, if there are signs that growth is beginning to return to “normal” levels the central bankers will turn off the fuel and leave the markets to their own devices.

Market interest rates will rise, bonds will fall in value and equities will rely solely on profit growth to attract buyers. The US as ever sets the tone and will be the first to turn off the tap, Europe hasn’t even started QE yet and Japan has only just embarked on its reflation journey, but for equities the USA is the benchmark and prices will be set according to the Fed’s policy only. The Fed is looking at two things, house prices and unemployment; a rise in the former will ultimately bring the latter down. House prices are now rising in the US, this may yet bring a flood of properties onto the market but it is the first hard fact that the US economic recovery is now properly under way.

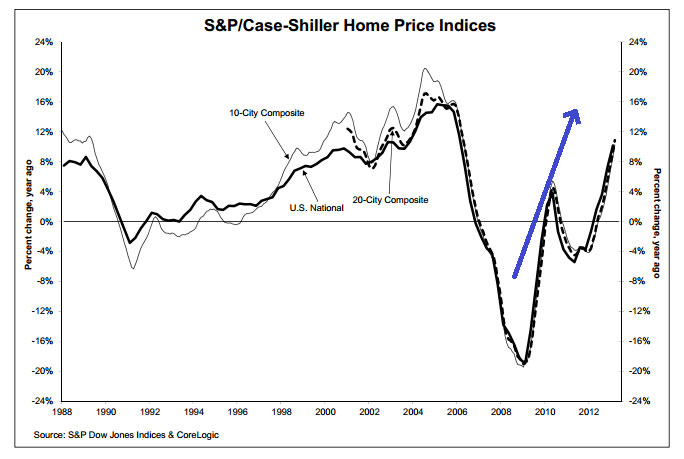

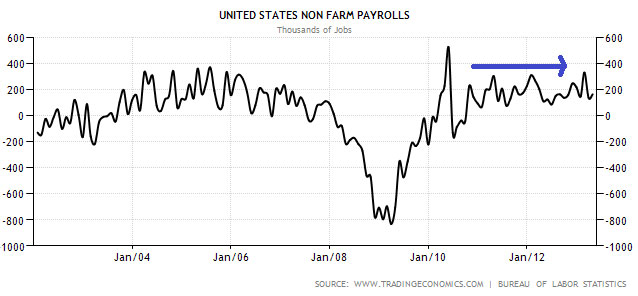

US House Prices and Unemployment

First quarter US house price data has shown an average increase during the past 12 months of over 10%. Some areas, particularly the over-developed “sunbelt” states of Florida, Arizona and Nevada, saw prices rise by over 20%. QE3, (which sees the Fed just buying mortgage bonds in the market) enables the banks to offer more mortgages safe in knowledge that they can sell them on to the Fed in the secondary market, is clearly working. The danger is now that it is working so well that it might be tapered off sooner rather than later. Talk of this happening is now impacting on the bond markets and the suggestion is that it may start as early as September.

The Fed has a rule of thumb that a growing US economy should create over 200,000 jobs per month, so far the reality is just below that target. Hurricanes and Tornados have sadly had an impact on these numbers but the trend, as can be seen above, is not quite at the halcyon days of the mid 2000s. Rising house prices should increase construction activity and will also make the consumer feel richer and thus free to spend a little more, thus creating a virtuous circle of growth. Again we are not there yet, though the equity markets are telling us it is not far away.

Corporation Tax

One of the consequences of unleashing the global free market via the World Trade Organisation is that everyone assumed that multi-national companies would be loyal national champions happy to pay tax at the prevailing rate to their home government, the fact that they simply find the cheapest place to pay tax has come as a shock to politicians, it shouldn’t.

In the EU free trade area different rates of corporation tax apply and this makes a trans-national corporate structure worthwhile. Many Unit Trusts (OEICs) are based in either Ireland or Luxembourg for just these reasons and a number of FTSE 100 companies are now technically Irish.

Nothing will change unless EU and perhaps even US corporation tax rates are harmonised, this may yet happen and there are talks to this effect. The other solution would be for the UK to undercut Ireland et al and reap the benefits, but unfortunately there is no room in the Exchequer’s piggy bank to allow that.

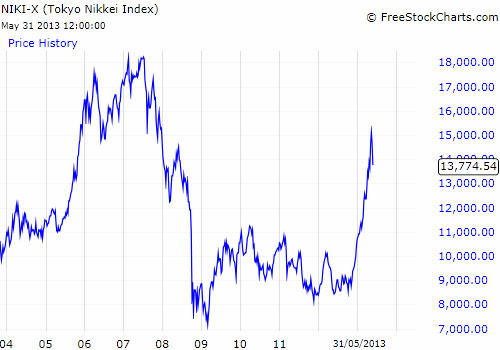

Japan

introduction of “Abenomics” or “shock and awe” QE. The policies includes targeting 2% inflation, devaluing the Yen, setting negative interest rates, quantitative easing, increase public spending and buying of construction bonds by the Bank of Japan(BoJ). In essence a lot of everything, this is an “all-in bet” on restoring Japan to growth after years of deflation. However, this will be at a huge financial cost to Japan, which is already one of the most indebted countries in the world. This is something the UK would love to do and all eyes will be on Japan to see if it works.

We are however still of the view that with a declining population Japan will always struggle to generate real growth. Recently, the Nikkei Index has fallen by over 10% as fears grew that the BoJ may be not overly committed to the plan.

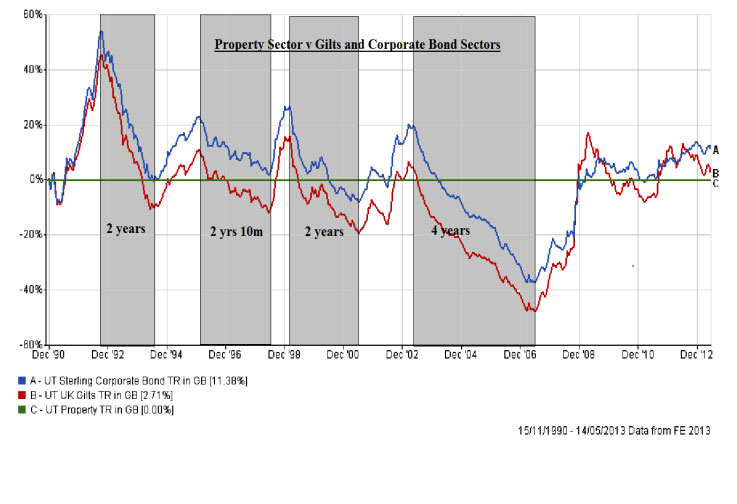

Property v Bonds

The grey shaded areas highlight the periods where it was better to be in property than in bonds. There is a natural switch between these asset classes as the big pension funds/insurance companies move money from bonds when interest rates start to rise, which means that bond prices will fall.

The BoE puts up interest rates when inflation starts to rise which is normally caused by rising property prices. Commercial property tends to go up towards the end of a cycle and as we can see the rise usually lasts two years or so. The fact that bonds are still outperforming property shows that there is still plenty of time left in the current cycle.

Bond holders do though appear to be getting an “itchy sell finger” but as this chart shows the switch is not happening yet.

Markets

To have sold in May wouldn’t have worked this year but the sharp sell-offs in Gold and Japan do remind us that no market rises indefinitely. The current worry/theme is “the taper” i.e. is US growth now so robust that the Fed can taper off QE3? Bad data perversely would see the taper delayed thus good for markets, positive data would actually worry the markets in the short term!

Much will depend on the statistics, particularly US employment. Also, eyes will be on China for any early signs that reform and reflation are bearing fruit. June can be a very quiet month for markets and thus susceptible to sharp corrections, but the background, particularly in the USA remains positive.

May 2013

Click Here for Printable Version

The interest rate on your bonds will stay solid as long as that is the type of bond you pucreashd. Some bonds have step rates or zero coupon rates. However, it sounds like you are buying a regular bond that has a fixed percent with a fixed term. Each day, the market price of the bond fluctuates based on its selling and buying values. As long as you hold it to maturity, none of this matters. The only down side for a bond these days is the solvency of the company. Like Lehman Bros. Their bond holders just received a notice that they will get $600 from a $5K investment. Bonds are a fab investment right now. Best investment is a mid term bond that would be held for five years. You can get some good ones out there with a term of five years with a 7 plus percentage return. Anything over five years, plan to hold them for a while. Eventually interest rates will go up and if you need to sell your bond, you may not get the full value.