Click Here for Printable Version

April 2nd was given the name of “Liberation Day” by US President Donald Trump, perhaps a deliberately confusing title for what, for the majority of US consumers, manufacturers, and farmers, is likely to be a financially painful experience. Indeed, even before the formal tariff announcements, US Consumer Confidence has dived and manufacturing costs have risen. Classical economic theory suggests that tariffs hurt growth and are inflationary. The Republican Party manifesto argued that increased costs would be more than outweighed by greater economic growth as manufacturing moved back to the US and by tax cuts. There was always a debate as to whether such costs would be transitory and just how practical it is for companies to move back to the US with a now restricted supply of cheap labor. For markets, the announcement marked the end of the negative uncertainty. What they want is for this announcement to be the end of it, so they can move on and focus on the size and benefit of the forthcoming tax cuts. Markets will not like any sign that this is just the start of a process whereby each month new tariffs are introduced on top of the last. As ever with the Trump administration, not all is necessarily what it seems. Tariffs themselves make little economic sense, so why has Trump made them such a key part of his strategy, especially when he is generally so pro-business and pro-stock market?

Stephen Miran of Hudson Bay Capital

Dr Miran of this Hedge Fund is the Chair of the US Council of Economic Advisers and is the main architect of the whole tariff economic strategy. He has made clear that the imposition of tariffs is a tool to achieve a broader restructuring of the global system of international trade. As he has stated in a post-election essay:-

“The root of the economic imbalances lies in persistent dollar overvaluation that prevents the balancing of international trade, and this overvaluation is driven by inelastic demand for reserve assets (US Treasury Bonds). As global GDP grows, it becomes increasingly burdensome for the United States to finance the provision of reserve assets and the defense umbrella, as the manufacturing and tradeable sectors bear the brunt of the costs.”

More simplistically, the dollar is too strong for US manufacturing and a strong dollar leads to excessive overseas buying and selling of US Treasury Bonds which leads to US interest rates being too high. So the ultimate objective is to weaken the dollar.

“Liberation Day” Tariffs

Expectations were for the best case of a flat 10% and the worst case of a flat 20%. We got the flat 10% for countries Trump likes but also 20% plus for those with large trade imbalances with the US. 20% for the EU, another 34% on top of 20% for China, etc. Vietnam and Cambodia were both hit hard, but nothing further on Mexico and Canada. The kicker is that the above 10% tariffs are delayed by a week, presumably for some “horse trading”. But if there is retaliation, they could get worse. Tariffs at these levels would turn America into its own economic island, trading only with itself. Horizontal links with the rest of the world are out, thus ending America’s participation in globalisation. Clarity is still lacking, even excluding the possibility that some of these rates are never levied after a few days or even weeks of negotiation, but the sheer scale is concerning. Fitch Ratings estimate that the new effective tariff rate might settle at 22% (up from 2.5% last year), much higher than the markets expected.

The US Consumer

These tariffs are also a revenue-raising measure. If all trade continues as before, then it should raise $600 billion or 2.2% of US GDP, twice the size of the largest tax increase in modern US history. If exporters don’t discount their prices and just add the tariffs on, then this is effectively a VAT that the US consumer will have to pay. Theoretically, Trump plans to hand this cash back to consumers via tax cuts, possibly along with the $1 trillion government savings Elon Musk claims to have found. But timing is everything; any delay could tip the US into a recession. If the dollar is weak, then this adds a further cost onto imported goods. Whilst this is the ultimate objective, perhaps Trump should have built the factories first before imposing the tariff? Some manufacturing will undoubtedly switch to the USA from abroad, but that will take time.

Double-Dip Recession?

As the US transitions away from globalisation to a closed economy, the risk of it tipping into a short recession rises significantly. It is estimated that inflation will jump to around 5% and economic growth will slow markedly as a result. The role of the US Federal Reserve Bank will come into focus. Trump wants interest rates down, as US mortgage rates are still around 6.6%. Helpfully, with the US Budget Deficit seemingly under control, US Treasuries should remain strong. Nevertheless, current recession odds have risen to around a 40% chance of a US recession in the next 12 months. The US consumer doesn’t like tariffs, so the offsetting tax and mortgage cuts will be needed very quickly.

German Rearmament

It pays to be prudent and not to borrow as much as “the bank” will allow, just in case of a rainy day. With the US starting to treat Russia as no longer a threat, that rainy day has arrived for Germany. A newly empowered Russia at the other end of the Fulda Gap has scared Germany into action. The scale of this borrowing is immense. As this chart shows, it is potentially double the post World War 2 Marshall Plan and possibly up to four times the cost of reunification. The beauty for the German economy is that it still has the manufacturing base to build the equipment it needs. It also crucially has the technical capability to develop the unmanned fighting technology that will dominate military warfare in the future. The money will not go to US arms manufacturers. Trump has got his way, but perversely this will economically harm America and should provide the true economic stimulus that Europe has been waiting for.

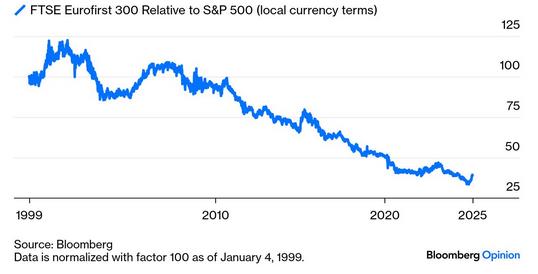

Europe

Europe as an investment market has been poor since the 2008/09 Financial crisis. Greece, Brexit, Ukraine and the lack of competitors to the dominant US Technology companies have meant that, Europe has been left behind. For US investors and their “wall of money” faced with the uncertainty of an unpredictable President and dominant technology companies that are expensive depending on whether A.I. is a game changer or just a better search engine, Europe represents an undervalued opportunity. Perhaps the biggest risk is the ability of the European Union to prevaricate; in the past, many large headline grabbing stimulus schemes end up not being spent. The ability of the EU to choke off investment through red tape is legendary. But this time it is mainly German money, so hopefully, it will actually have an impact.

Markets

This is a pivotal moment for markets, as the USA is attempting to withdraw from the global trade system. As the world’s largest consumer market, this will have long-term consequences. However, it is hard to see cheap consumer goods manufacturing moving back to the USA; consumers will be the big losers. For the key market factors, US inflation is likely to go up, which is bad, US growth will slow, which is bad, though US interest rates will have to come down, which is good. Much depends on the tax cuts. Markets will have to reprice the unexpectedly severe tariffs but will then move on to interest rates and tax cuts as the key market drivers. With a newly weak dollar, investors and traders have already moved on to China, where technology developments are now outpacing those of the USA and also to Europe, where inflation is under control, interest rates are falling, and growth should accelerate. The stimulus in Germany is actually a bigger deal than Trump’s tariffs. In markets, the old adage of “sell the rumor, buy the event” should come into play once the tariff repricing has taken place. The Mag 7 are already down 15% on the year. How quickly things change in markets. The beauty of markets is that it is not just US equities available to us. The tariffs have not gone away yet, but the end is closer. Markets want “one and done” for the tariffs and tax cuts soon.