Click Here for Printable Version

The main focus for global stock markets remains the China US trade war. There were some signs of a truce at the G20 where Presidents Trump and Xi agreed to restart talks. As yet though nothing has actually changed nor have talks formally started, but Trump is now under time pressure and the Chinese will be fully aware of this fact.

Trump has also not given up on pursuing a trade war with Europe.

With German manufacturing data collapsing this will be the last thing the various new European Presidents will want.

The longer these trade wars go on then there is the increased risk of the recession coming early. Globally,company profit expectations keep being downgraded whilst bond yields flirt with inversion (2 year yields being higher than 10year ones)despite equity prices continuing to rise there are signs that some investors are starting to be more defensive, Gold has rallied and currency traders have moved into the safe haven of the Japanese yen.

In the UK,Brexit remains in abeyance whilst the Conservative Government appoints a new leader.

The markets don’t usually care about politics, particularly in the UK, however with an early General Election increasingly likely they will want the candidate that is most capable of beating Nigel Farage, preventing a split in the pro-Brexit vote that would let in a Labour government.

It is also very unusual for the dull world of investment management to move from the newspaper money pages to the front page, but the suspension of dealing at Woodford UK Equity Income fund did just that.

Woodford

Following a period of disappointing performance several large institutional holders placed redemption orders for their entire holding of the Woodford Equity Income unit trust.

For the overwhelming majority of UK Equity Income unit trusts this would have been painful but relatively easy to deal with, but for Woodford there isa particular structural issue that is making complying with these sell instructions a problem.

This has forced dealings to be suspended until these issues have been resolved.

The problem is that historically unit trusts have been allowed to hold up to 10% of their funds in “unquoted assets”.

This arose from the times when certain exchanges were not “Recognised” by the then authorities and it also allowed funds to retain investments in former listed companies that had gone private or had issued loan notes as part of a takeover.

Most mainstream funds don’t use this provision and those that do restrict themselves to companies that are very close to floatation.

Woodford Equity Income,however,invested in early stage companies and bought very high percentages of them.Neil Woodford to his credit was very open about all of the fund’s holdings, publishing a full list every month,whereas other funds do this every 6 months and hide the data away in Report and Account notes.

However, after a particularly bad run (and all investment managers have them) funds under management fell.

The unquoted investments then became a problem, valuations are set by accountants and not by the market.

As the quoted value fell and the unquoted value stayed the same then the 10% limit became a massive problem and was soon breached. With no obvious buyers for the unquoted investments, Woodford tried various “creative measures” to get the percentage down but eventually had to admit defeat and suspend trading.

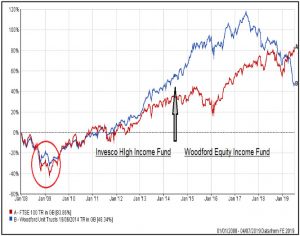

But we mustn’t forget that Neil Woodford has had a very long and up until now exceptional career in fund management.

As this chart shows (which combines one of his funds at Invesco with the Woodford Equity Income).

Unit holders were protected from the worst of the 2008/09 crash (see the Red Circle) and then benefited from significant out-performance compared to the FTSE100.

Performance started to drop off after peaking in June 2017. Concerns had been raised for some time in the specialist financial press about the high unquoted element,notably by Tom Winnifrith.

But the media falls back on personality rather than analysis. Of course,if just a few of his mainstream stocks had outperformed then this picture could have been very different, the line between success and failure is very fine in investment.

What seems to be happening now is that some investments will be written down and attempts are being made to sell others in the unquoted portfolio.

Investment Process

The issues with Woodford do highlight the importance of process when selecting unit trusts.

Pre the internet,portfolio managers had to rely on trusting the individual manager,hence the focus on personalities,but as the industry has evolved so has fund selection and the increased focus on risk. Put simply “you manage the risk and let the returns look after themselves”.

We do this by looking at a fund’s underling investment process.

There are only three ways of managing equity portfolios:-

1.The Index Tracker. Here the manager (usually a computer) buys equities in exactly the same percentage as the chosen index. This removes the risk of the manager going “off-piste”. However, it is therefore impossible for the fund to outperform and over time returns will not match the index due to the impact of charges.

2.Index Plus/Minus. Here the manager has freer reign over the investments but only within limits as set by the Trustees or Board of Directors. They exert control by giving a strict parameter as to the degree of variance a sector or stock can be away from the benchmark index. So if a stock is say 5% of the index then under a +/-3% restriction the maximum a portfolio could hold is 8% and the minimum, even if it is hated, must be 2% of the portfolio.

This means that the fund can outperform, but not by much and underperform, but again not by much. This is how the majority of institutional money is managed globally

3.Unrestricted. This is where the manager has free reign with no restrictive conditions,bar legal ones,and is the Woodford situation. This gives scope for significant out and under performance, and that is exactly what has happened. Often such funds are badged as Special Situations, Alpha, Recovery etc. Furthermore, when this strategy is run by smaller owner/manager investment houses the fundamental risk increases.

So when picking funds from Category 3 it is important to note,that however they may be marketed,such funds have a fundamentally higher degree of risk.

We are also very cautious of investing in funds managed by small boutique firms and especially ones where the owner of the firm and manager of the fund are the same person.

Oversight of a manager is crucial,especially when a fund inevitably goes through a period of underperformance.

Would Neil Woodford have had these problems if he was still at Invesco? Large investment houses often merge funds and have natural in-house buyers.

Having the support of a large organisation offers strength in depth of management, finances and investment personnel.

We use the analogy of Premiership Football teams, occasionally a team comes from nowhere to win the League,however, the bigger, well-financed clubs with large squads and youth schemes will always be there or thereabouts into the foreseeable future.

It is the financial equivalent of these clubs we need to concentrate on. We don’t want to buy the best performers over one year,but the most consistent performers over the whole investment cycle.

Facebook and Libra

Facebook announced the initial launch of Libra.

Calling it “a global currency and financial infrastructure”i.e. a Facebook version of Bitcoin.

With a quarter of the world’s population using Facebook this is big news. The name Libra comes from the Roman measurement of weight the pound, hence lb for the imperial weight and the £ symbol is derived from a copperplate L in Libra.

This has sent alarm bells ringing in Central Banks around the world and marks the first of many expected major moves by Big Tech into financial services.

So concerned is the US Congress that it has asked Facebook to “pause development on its Libra cryptocurrency until lawmakers have had more time to investigate the ramifications of the company’s actions”.

This is the beginnings of what will be a very significant development for the whole financial system

Markets

The global economy remains hostage to Trump and his trade wars,the true impact will start to be seen as US corporations report second quarter profits this month.

Expectations have been downgraded rapidly over the past month,failure to match these now modest expectations will not be well received.

The key remains the trade negotiations, even if Trump can conclude a satisfactory deal with China he will then turn to Europe and test what will soon be a new leadership.

They might well be facing an enormous double whammy of a no-deal Brexit and a US trade war. In the UK we will get a new Prime Minister in July, he may well have a very short term of office. It seems that a snap General Election may be the only solution to the Brexit impasse, barring an unlikely climb-down by the outgoing European leadership.

The global investment picture, as we are now well into the Summer doldrums,remains very messy. If US earnings can hold up then so will equity markets and if Trump signs a trade deal they will go higher, but for now this Bull is still running, but looking increasingly tired.

July 2019

Click Here for Printable Version

This information is not intended to be personal financial advice and is for general information only. Past performance is not a reliable indicator of future results.