For many months now equity markets have been going up in straight lines with minimal volatility, we have warned that this is not normal and to be aware of the “Black Swans” (unforeseen events), as June progressed a pair of such swans have crossed the market’s path and normal volatility has now resumed.

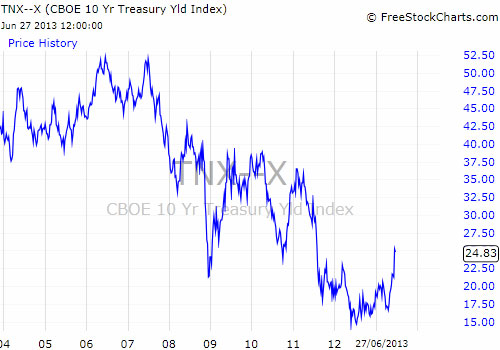

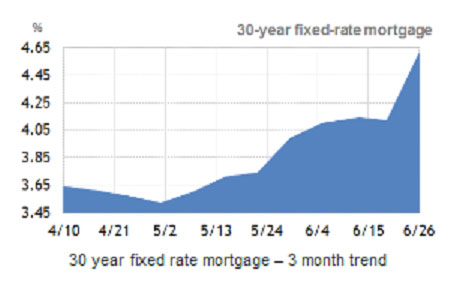

The first of these was from Ben Bernanke who formally laid out a plan for the ending of QE3, the markets took this as a certainty and have re-priced bonds and thus US mortgage rates, as though QE3 no longer exists.

The second swan was a display of bravado from the Chinese version of the Bank of England, the People’s Bank of China.

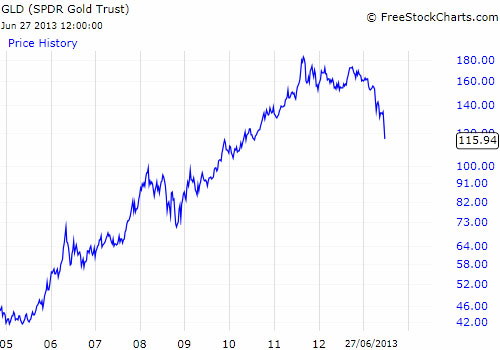

They deliberately withheld cash from the Shanghai Inter-Bank markets thus bringing a number of banks close to collapse, then having made their point, liquidity was eventually provided. At the same time Japan remains very volatile and the gold price keeps falling. The second quarter ended with global equities down 1%, the more volatile emerging markets 8% and bonds down 4%.

Ben Bernanke

In the last newsletter we highlighted that US house prices were showing decent levels of growth helped by QE3 and “the danger is now that it is working so well that it might be tapered off sooner rather than later”. So markets were expecting the programme to be reduced but they did not expect from the normally very evasive Federal Reserve Bank an unequivocal statement of intent i.e.

“And if the subsequent data remain broadly aligned with our current expectations for the economy, we would continue to reduce the pace of purchases in measured steps through the first half of next year, ending purchases around midyear. In this scenario, when asset purchases ultimately come to an end, the unemployment rate would likely be in the vicinity of 7%, with solid economic growth supporting further job gains……. If conditions improve faster than expected, the pace of asset purchases could be reduced somewhat more quickly…” Ben Bernanke, FOMC press conference.

The current US unemployment rate is 7.6%, not too far away from 7.0% and markets had been working on the basis that a 6.5% rate would be the trigger for QE3 ending. Markets were very quick to extrapolate and now assume QE3 will be tapered off starting in September. The result was the yield on US Treasury Bonds rose (prices thus fell) from a low of 1.5% to 2.5% and crucially so did mortgage rates for US home buyers.

It took 3 QE programmes to get interest rates down to the point that the US housing market started to recover, has it taken just one comment to undo 5 years of work? The rise in mortgage rates could be very significant, no-one knows what the tipping point is in terms of home affordability in the USA, especially in a still uncertain US jobs market, these rates may force up mortage defaults, bring a flood of homes onto the market and threatens to derail the recovery just as it was getting going.

All of these questions add to uncertainty, and as we know markets hate uncertainty. If it does, those who believe that the US will not recover and is stuck in a Japan-like cycle of long term deflation will start to come out of the woodwork again. Perversely they will be buying the asset classes that have fallen the most post the announcement, bonds and gold. All eyes will now be on the jobs data, and also whether earnings growth from US corporates will be finally good enough to keep the equity markets rising without its QE addiction?

Gold

QE3 might end, the Chinese are clamping down on shadow banking and Abe wants to weaken the Yen meaning that these various carry trades have to be closed down and the cash runs ”home” to the Dollar, and so gold has to be sold. Many traders are though queuing up to buy this most volatile of assets, just a question of when?

China Shadow Banks

In China short term interest rates surged from about 5% to 9.75%. Clearly the Chinese government and Peoples Bank of China (PBOC) are awash with cash so why is this happening? China likes to control its banks, in order to choke off inflation it tells them to stop lending for speculative property development and expects them to comply.

Being Chinese they of course do, but then set up wealth management subsidiaries that are technically not banks but as part of their product range offer mortgages for investment purposes (a shadow bank, just as a building society is in the UK). They fund these mortgages from the money markets, as did Northern Rock/Bradford Bingley, but as they are not banks they are outside the PBOC’s control and speculative property purchases are rising again, as China reflates.

The new leadership is not happy with this as it threatens to derail a whole package of reforms that will be announced later this year. So in order to flush these wealth management companies out, the PBOC has “gone fishing”.

They have refused to provide the market with liquidity and are sitting back and watching who gets close to going bust. Ruthless, but could be effective.

Long term if it works, then the PBOC is to be applauded as it will squeeze this dangerous property speculation out of the market. If China is emerging from this state controlled/capitalist hybrid to an open market economy then this is a very positive thing.

Markets

So we have the return of more normal volatility to markets plus a confusing economic picture. Ben Bernanke is playing with fire and risks derailing the recovery just as it is about to get going properly.

The Chinese are still on target to reflate during the final quarter and the yet to be announced reforms could be significant. But we are now having to wait for news, both of the state of the US economy and the health of corporate earnings, throw in what the Chinese may do to “clear the decks” before the Party Congress and you have many reasons for institutions to sit on their cash for now.

July is often just as quiet as June and we have the US 4th July holiday to disrupt market flows as well. Gold may be the key to this, if the new quarter sees the price fall reverse trend this could stimulate “greedy traders” to join in, but further falls could add to the uncertainty and “fear” will be the dominant emotion.

June 2013

Click Here for Printable Version