Click Here for Printable Version

Markets continued to recover in July despite the pandemic now looking as if it will be a marathon and not the sprint the markets had priced in. At first glance this performance may seem odd as infection rates have picked up in various countries. However, the markets see that the government responses are limited in their economic scope and thus damage.

Also, being mercenary markets see that the longer the pandemic lasts then the longer Quantitative Easing will be there to support bond prices and thus drag equities up as well.

Markets are driven by a combination of the rate of change in interest rates, inflation and corporate earnings growth.

QE means that interest rates have and continue to fall around the world, there is no inflation (as yet) and even a minor uptick in economic activity means that the rate of corporate profit growth is accelerating.

So as investors we have the three key drivers for markets all positive and improving, hence markets go up.

We have nearly completed the US second quarter results season and there is clear demarcation between those that are doing very nicely from the pandemic, and those that are not.

The very high percentage of tech and healthcare in the US indices means that the negative pandemic news does not now necessarily translate into negative market news. Elsewhere, China despite Trump’s bashing and Japan’s move of production facilities from China to Indonesia, Vietnam and Laos continues to recovery quickly. Europe has also taken a potentially transformative step forward.

Europe

The European Union and the Eurozone (those countries that use the euro as a their currency) have long had a structural problem.

They have the trappings of a Federal State, a Central Bank, common currency etc. but funding comes from the individual states not from debt (bonds) issued directly, nor from direct taxation (though Brussels does receive excise duties from imports and a cut of each state’s VAT).

To move forward the EU needs to have the ability to raise its own funds. Without the UK and its opposition to “ever closer union” France and Germany have taken the opportunity presented by the economic impact of the pandemic to take a major step forward for the EU.

The proposed new EU recovery fund is large. Combined with measures such as the Guarantee Fund for EU businesses and the European Stability Mechanism (ESM), the e750 billion fund will take the total to e1.2 trillion, or a very significant 6.5% of GDP. Critically, it is predicated on closer fiscal co-ordination (taxes) and the creation of a euro zone sovereign bond.

How the fund is financed is maybe more important for Europe’s long-term future than the fund itself.

By agreeing to jointly issued bonds that will later be repaid from a central EU budget and new region-wide taxes, the bloc has taken the first steps towards integration.

There are still many political hurdles to overcome, there is opposition from some countries and the German public might worry that they could end up effectively guaranteeing all the other countries debts.

For investors, if this package proceeds, this would remove the doubts about the longevity of the euro and thus could make a stronger investment case for Europe.

With the UK having left, the EU needed to move on, the pandemic has given them the excuse to do so.

Gold and the US Treasury 20 year ETFs (TLT)

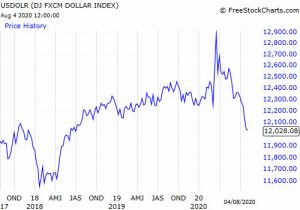

Gold has been enjoying a particularly strong run, this is a direct response to the increase in the global supply of money.

Firstly, it is important to note that gold does not qualify as an investment, as unlike a bond it pays no coupon (interest) also there is no dividend (unlike shares) and finally it is expensive to store and move.

Historically, gold was regarded as protection against inflation which is partly correct but not in the way most people think. In practice gold is primarily used to hedge complex derivative trades (known as carry trades) when the US dollar is weak.

As the second chart above shows; since QE was restarted, after the virus took hold, the dollar has been weak. One of the reasons it has been so weak is that the yield on US Treasury Bonds has fallen to 0.5% and critically this is actually below the current US inflation rate.

So US Treasury bonds are offering a negative Real Yield. Therefore they cease to be a “store of value” and effectively cost more in real terms than holding gold.

Hence, the left hand chart shows the direct correlation between the price of the US 20 year Treasury ETF and the price of Gold ETF.

This is a perfect storm for Gold, hence speculators have piled in.

UK House Prices Nationwide Index

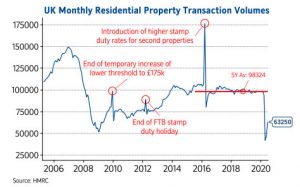

We have long argued that the biggest factor in determining the direction of the UK economy is house price growth.

Clearly, as redundancy announcements from the hospitality, retail, travel and aerospace industries hit the headlines there is genuine concern that this recession will impact house prices.

The government has so far responded with a cut in stamp duty. As the above chart shows prior stamp duty changes can cause a distortion in the number of houses bought and sold but rarely changes the trend.

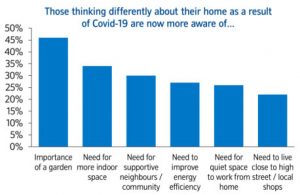

Maybe this time it will be different? The second chart from a survey done by Nationwide suggests that working from home is changing how homeowners perceive what is important in their properties.

This may yet have an impact on transactions and might help move wealth out of London? Against this positive news we have also seen banks and building societies tighten up their lending criteria and demand bigger deposits.

The Chancellor’s Autumn statement may yet bring in measures to help?

Markets

As we said last month global equity markets continue to look at the improving global economic data and are still extrapolating a quick return to something approaching pre-virus levels.

The pandemic though has not gone away as quickly as expected.

For some stocks this is bad news and as such money keeps flowing into the big tech stocks that are benefiting from remote working. Markets also are in “recession-mode”, that means they look at the future trend i.e. the next 12 months and not what is happening now.

As long as QE and fiscal stimulus packages keep being announced then they will continue to look through this crisis and wait and hope that a vaccine(s) can be approved.

We still have a US Presidential election underway and the anti-China rhetoric will only get worse. This is still a market that remains addicted to Quantitative Easing, maybe the biggest risk is that we do get a viable vaccine and the Central Banks decide to stop printing money?

The economic stats, such as the US Payrolls data, still point towards an economic recovery and markets may start to worry that the printing presses may be turned off sooner rather than later?

August 2020

Click Here for Printable Version

This information is not intended to be personal financial advice and is for general information only. Past performance is not a reliable indicator of future results.