Click Here for Printable Version

For the majority of markets July saw a return to the low volatility drift upwards. A strong euro hurt the German Dax index, but so far the usual summer headwinds have yet to arrive.

Complacency is always dangerous in markets as it tends to deepen the extent of any shock when the inevitable happens. For now though markets are not mispriced.

They are simply reflecting good corporate earnings growth, steadily growing economies and low inflation expectations.

The Central Bankers are itching to tighten monetary policy and increase the rate of interest globally but need an excuse to do so. They haven’t got one, at least not for now.

Geopolitics remains troubling, North Korea and Trump are keeping politicians busy, but this is all (hopefully) short term noise.

Markets are so far assuming that the Korean situation remains a “war of words” as the military options, bar all-out war, are very limited.

As long term investors we need to focus on the big picture, as ever, where we are in the cycle needs to be constantly revisited. In time terms the cycle is mature; in economic terms there still remains a lot of potential for benign growth with low inflation and that means markets should have further to run.

We do need however a return to normal volatility; the current market pattern is unhealthy.

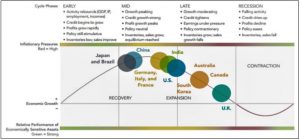

Investment Cycle

Source: Fidelity

We have written many times about the Investment Cycle, historically a recession occurs every 7 or so years.

The stock market predicts this recession about 12 to 18 months ahead of it actually happening.

A recession normally leads to a collapse of corporate profits and thus share prices have to fall in order for the rating to remain within historic ranges.

We are overdue a recession, though the post “Credit Crunch” recovery has not been a normal one. Only now are global economies starting to display reasonable levels of growth.

Crucially, inflation remains low and whilst it does, Central Bankers have no excuse to push interest rates significantly higher, and thus the probability of a recession remains low.

The above chart from Fidelity shows the current state of play between the major economies in the cycle.

All are in expansion mode, though the Brexit referendum, political crisis and deliberate bursting of the London “Buy to Let” bubble means that the UK is heading towards contraction.

Crucially though, we are not there yet and could easily reverse on a positive political policy decision. Australia and Canada are commodity economies and oil price weakness has a knock on effect on these areas.

Critically, all of the big economies are in the sweet spot. Much will depend on Trump; bookies have staggering odds of 4/6 that he will be impeached during his term of office.

Perversely, it may actually take him losing (or even walking away) from office in order to get his economic growth policies implemented!

So whilst the cycle is mature it is only the UK where we have to be on recession watch. As ever it always pays to have a balanced portfolio.

Harley Davidson

Our favorite bellwether for the US economy recently announced a decline in sales for Q2 2017.

This is slightly alarming as we have found in the past sales of these expensive but not very practical motorcycles have proved areasonably accurate predictor for US business activity.

Harley-Davidson’s sales fell 9.3% in the U.S. and 6.7% globally in Q2, remember no-one actually needs a Harley it is purely a discretionary purchase.

Harley-Davidson sold 262,221 motorcycles last year, but has now downgraded forecasts for this year to around 246,000 units.

This may support our fears that the US economy is not as strong as it appears.

Others have suggested that it is a demographic issue.

Harley’s “baby boomer” customer base is getting older and may be thinking about a different kind of scooter in the future!

This demographic fact is increasingly being used as an explanation for the sub-par level of growth and low inflation in the USA.

Demographics

One of the key tenets of economic theory is that growth is driven by an increase in the size of a country’s labour force.

For example, Japan has struggled with deflation as it has an inverse population pyramid (greater number of older people than younger ones).

Economists also point to America’s above average growth in the 1970s, 80s and 90s and explain it was driven by the post war “baby boomers” starting to work, as well as the widespread entry of women into the labour force. However, what we have seen in the USA since 2000 is a steady decline in the percentage of the US working age population that is employed, despite falling overall unemployment.

If this pattern continues, then US growth will continue to be anaemic. Male unemployment in the “Rust Belt” seems to be the issue.

Will this change if Trump can’t get his plans passed?

Markets

August sees the crucial second quarter US corporate results season, expectations are high and companies need to deliver, with valuations at current levels there is little room for error.

As we write 75% of results are in and the 12 month forward expectation is now for a very healthy 17.5% earnings growth which translates to a P/E ratio of 18 times, which is fine.

We must also remember this no longer includes any Trump stimulus. We are beginning to think that Trump will have to leave office (one way or another) in order for Congress to get behind his tax reforms.

If that does happen then there remains significant upside for US corporate earnings.

For the global economy wage inflation remains stubbornly low despite unemployment levels falling. Economic theory says this shouldn’t happen.

It may be due to, (as we discussed above) an ageing population or it might be a lifestyle choice with the statistics not being able to cope with employees trading pay rises for more free time?

Or it could just be a time lag? The usual economic supertanker taking a few miles to turn!

If it is a delay, then interest rates will rise sharply from here and we have to move to recession watch mode for the global economy. For now the economic ducks remain lined up nicely. The geopolitical ones, however, are flying in all directions.

July 2017

Click Here for Printable Version