The summer doldrums for equity markets continue with day to day volatility, despite recent weakness, at relatively low levels.

This may seem surprising given the troubles in the Ukraine, Iraq and now Gaza. Global equity markets are dispassionate places, their concern is purely corporate profitability, anything that may impact on the ability of Global Inc. to make money is rapidly “priced-in” to share values anything else is callously ignored. As we write the US quarterly results season is progressing and generally corporate results have been fine, not brilliant but not bad either, just ok.

As the cycle is getting mature we do need to see profit growth accelerate and there were some glimmers of this, but valuations are no longer cheap and the markets will be looking for more and soon. Markets can be derailed by geopolitical events, risks are getting elevated in both the Ukraine and Iraq and whilst from a portfolio perspective there is little we can do to prepare, we do need to be aware of what these risks may be.

Ukraine/Iraq/Saudi Arabia

Geopolitical risk should really be renamed as inflation risk; the common factor in all market moving events such as the two Gulf Wars has been oil.

The first instance of this was in the early 1970s when the various Arab/Israeli wars led to oil supplies from the Middle East being cut off, energy was restricted and inflation took off, contributing in part to the 1974 market crash and very high levels of inflation through the ‘70s and early ‘80s. Essentially conflict is bearable, from a market perspective, as long as the oil supply is not affected. The two Gulf Wars are classic examples of this. Currently we have two conflicts, Ukraine and Iraq that so far are having no impact on the oil price but have the potential to do so.

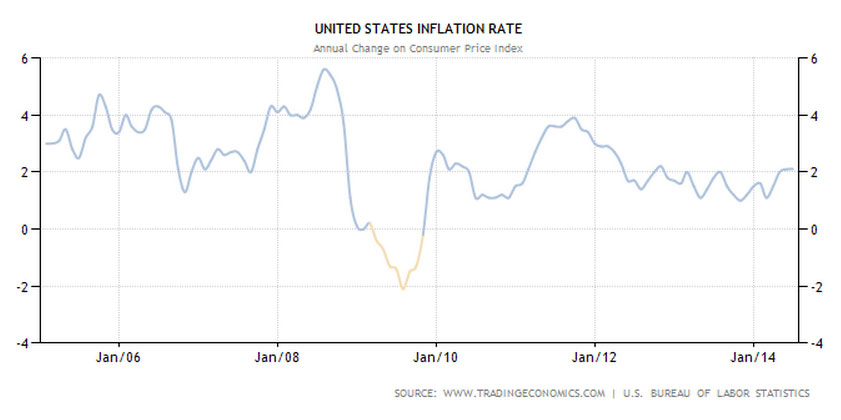

As the above charts show, oil prices and US inflation remain relatively subdued, this means that the markets have looked at the risk of Russia cutting off the oil (and gas) and ISIS taking the Southern Iraqi oilfields and assessed them as small. The market may well be right based on current information but we should be aware that both geographic areas have the potential to spiral out of control and have a significant impact on energy prices, inflation and thus interest rates, then bond and share prices.

In the Ukraine Putin has handled the situation badly. Time and democracy would have seen Russia peacefully acquire eastern Ukraine, his militarily support of the separatists has led to the shocking destruction of the Malaysian Airlines plane and that act has stimulated a now unified sanction response from Europe and the USA. As we write there has not been a response from Putin but companies, such as BP, will now be very worried that their immense investments in Russia will prove worthless.

For Europe and Russia gas is the key, will Putin turn the gas off? He can’t afford to but may just be bloody-minded enough to do so. Europe does have high gas stockpiles and there is a glut of LNG from Qatar, additionally the US has plentiful gas supplies from fracking. But a cold European winter could change the game. Russia has signed a deal to supply China with gas but needs to build a pipeline first.

On its own, and based on current information this problem should be contained, but if we also get an oil crisis in the Middle East, it won’t be.

Saudi Arabia is the dominant oil producer in the world, second is Iraq. The fundamentalist insurgent group ISIS has taken over the Sunni religious areas of Iraq, which doesn’t include the main oilfields in the South, hence the lack of reaction in the oil price. Why should Saudi Arabia be dragged in?

The answer is very complex but lies in the relationship between the Saudi Royal family and the Saudi religious establishment (Ulema). If ISIS becomes a threat to the Ulema’s predominant religious position, as it may do, then Saudi Arabia may decide to “take-on” ISIS.

So far the Saudis have moved 30,000 troops to the Iraq border, ostensibly to prevent incursion into Saudi Arabia, so this risk has gone beyond the theoretical. Nothing has happened and probably will not do so, but we do have to be aware of these risks and the impact they could have on the cycle, especially as valuations are steadily moving to neutral from cheap. Such geopolitical risks are binary events which makes them very difficult to plan for.

Driverless Cars

The UK government has announced that driverless cars will be allowed on public roads from January next year, this has created some headlines but could over time mark the beginning of the fourth transport age after horse, steam, petrol/diesel?

A car is often the most expensive item a family buys after their house. Unlike a house most cars go down in value, increasingly cost more to run and park and in cities rarely travel faster than a horse and cart from over a hundred years ago! For most however, public transport does not offer a viable alternative.

It is expensive, inflexible, and not as pleasant as travelling in your own cocoon with radio and air conditioning. A taxi is often seen as only marginally better, so why would we want a driverless car?

Two US companies perhaps offer us a vision of how the driverless car experience might just work. Firstly, Google offers the car part, a small pod like car complete with internet connectivity into which you just sit and it takes it you (just like a taxi) to your destination. You might pay a fare or the inevitable adverts you will have to suffer will pay it for you.

Secondly, an existing taxi software company, Uber, uses an app on your smartphone to know where you are, allows you to select from a range of vehicles e.g. limo or minicab, allocates the closest vehicle, takes you to your destination and automatically bills you depending on how far you have gone (no tip).

In New York where Uber originates the number of young people with a driving licence is dropping significantly, the convenience of pressing a button for your transport with minimal waiting outweighs the hassle of owning, parking and driving a high cost vehicle. Combine Uber software and a Google car and for many city dwellers owning your own car will become an unnecessary expense.

For electric cars the handicap of slow recharging is negated as a fully charged one in the fleet comes into service when the other runs out of juice.

This will all take time of course and applies mainly to big cities but for many car manufacturers they are going to have to adapt to a new world or go the way of the steam engine.

Markets

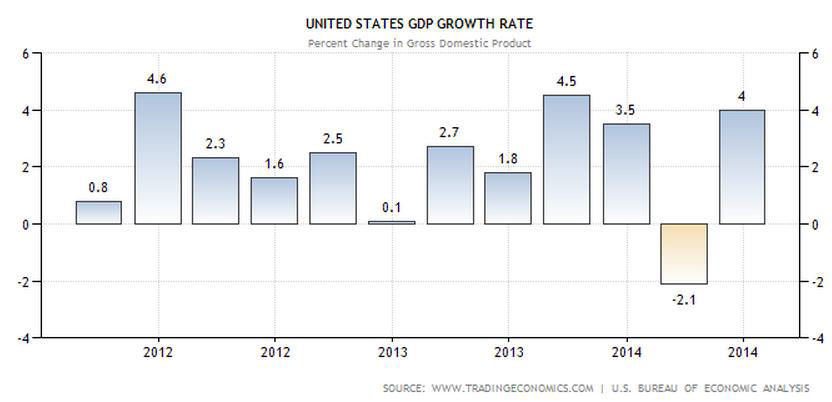

Profit and GDP are interlinked each one feeds on the other. The recent US results season has been fine but really should have been very good. Much has been made of the recent US GDP numbers hitting a more normal 4% but as this table shows bursts to 4% have not been uncommon, we need consistent quarter after quarter of 4% for the US economy to have truly returned to “normal”. US QE “tapersout” in October, there is some nervousness in markets that without QE the US will slip back to minimal growth.

It took some time but the weakness in small and mid-sized company indices has finally fed through to the Blue Chips. But, as we have said many times before such moves or corrections are necessary.

Normal levels of volatility for share prices call for swings of up to 20%, the fact that we have not had such a move for some time doesn’t mean that it won’t happen at some stage. However, they are healthy, it is important that, just occasionally, the short term traders are shaken out and allow the long term buyer to pick up stock at value prices and push the indices back to their highs.

This can be a painful process but not if your portfolio is structured properly. Nothing fundamentally has changed; we still have not had enough consistent economic proof that the US and thus the Global economy are returning to normal.

The taper ends shortly and we will enter a period of uncertainty, has the nurturing of the Federal Reserve Bank worked, will the fledgling US economic recovery soar to new heights? Or has it left the nest too early?

The performance of bonds and smaller companies suggests that the “hot money” thinks it has moved too early, but if it has then the Fed will have to come up with something else and quickly. Pressure from the White House with an eye on the next Presidential Election will ensure that this will be the case. As ever “don’t fight the Fed” is an important adage to remember.

July 2014

Click Here for Printable Version