Click Here for Printable Version

The old stock market adage of “so goes January so goes the rest of the year” if true, raises the possibility of a good year for investors.

Global markets bounced strongly after the wild movements of early December. The MSCI World Index rose by 7.1%.

The Far East was up by 8.1% and the FTSE100 again lagged but still rose by 3.6%.

Some commentators will jump on the bandwagon and blame Brexit but it is simply the largest FTSE companies are in sectors that remain out of favour.

Why such a strong bounce?

Last month we identified that the markets were worried about a sharp decline in expectations for profit growth. They feared that a combination of Trump’s trade war with China and the US Central Bank raising interest rates were hitting global demand for goods and services whilst increasing costs.

During January the previously “hawkish” Fed Chair Jerome Powell soothed market fears. Indeed at the most recent FOMC interest rate setting meeting they changed their expectations from two further rate increases to none at all.

At the same time Trump seems to have sensed he needs to do a deal with China and soon. We have highlighted over the past two months that both of these issues are binary, both could be quickly turned from a negative to a positive.

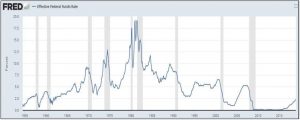

Recession Watch

Source:St Louis Federal ReserveBank

This chart from the Fed itself shows the historic pattern between the rate of change in the US version of Base rate and an ensuing recession (the grey bars).

Only twice in the past sixty years,inthe 1960sand the Greenspan era of the late 1990s,has a series of rate increases not led to a recession one to two years later.

So the probability remains high that we are approaching a danger zone for markets.

Our thoughts remain that the markets will start to price in a US and thus global recession from the end 2019 onwards, particularly as the US enters the Presidential Election process.

So what the Fed is doing now is,in the short term, very good news,but it may just be a stay of execution for markets.

For clients it remains very important that cash reserves are at the correct advised level.

DRAM Prices

In the past the “Canary in the Coalmine”for the global economy was machine tool orders, today it is DRAMs (memory chips that are in all electronic devices) DRAM suppliers and manufacturers had already begun to lower prices for the first-quarter contracts in December.

Taking account current high inventory, weak demand, and the pessimistic economic outlook for the medium to long term, both sides have cut prices of 8GBchipsfor the first-quarter contracts to around US$55 or lower.

This implies that the average price of 8GB chips has dropped by at least 10% in January, and there are reports that prices will continue to fall in February and March.

DRAMeXchange expects a quarterly decline of nearly 20%, steeper than the previous forecast of 15%. This is not a sign of a healthy global economy.

But it might just be the Trump/China trade war?

Brexit

Unfortunately, the soap opera continues.

However, anyone who knows anything about the workings of the European Union knows that nothing happens until absolutely the very last minute.

At this point there is either a resolution or the “can is booted down the road”.

So March 29this the deadline.

Between now and then all is irrelevant.

It would seem that the Prime Minister’s strategy is to be very persistent with her deal, wait until the last minute and hope for something from Brussels that would be acceptable to the DUP and help her gain their crucial votes.

In the meantime,we should expect Project Fear to be ramped up to even more extreme and frankly daft levels.

We are all apparently going to die earlier as we won’t be able to afford EU sourced fruit and vegetables!

As the pound has already devalued against the euro since the referendum this should already be a statistical fact, clearly it isn’t.

Also it ignores the reality that fruit and vegetables from elsewhere in the world would be much cheaper for UK consumers without the protectionist EU tariffs. For markets the only fear is of a chaotic crash-out. Goldman Sachs puts that risk at less than 10 to 15%, hence the relative stability of the pound.

US Corporate Earnings

As ever markets can only go up if company profits are increasing.As this chart shows the sharp December fall in global markets were preceded by a dramatic decline in earnings expectations.

From forecasts of 11.5% growth current expectations are for 7% growth.

This isn’t bad, with inflation at circa 2% it is actually very good, and in-line with historic norms.

It is just the market was promised a Ferrari and got a Fiat instead!

We are currently mid-way through the fourth quarter results season. So far the figures are ok and generally slightly better than the reduced expectations, however, forecasts for the rest of the year are still being cut.

Trump/China is again the major factor, as is rising costs.

With bad weather in the US there is a risk that without a China trade deal these numbers might yet come down further

Markets

Without sounding too much like a stuck record, as ever it all depends on Trump.

It does seem that the penny has finally dropped that trade tariffs are killing American jobs rather than saving them.

He needs to sign a trade deal with China and soon.

But he enjoys being unpredictable, he may yet“double down” at the last minute as it is now clear that China is hurting from the trade war more than the US is.

If he does,then markets might in turn seek to exert pressure on Trump and fall, just as they did in December.

It is still very odd that corporate earnings growth has started to slow at this point of the cycle, is it possibly too easy and neat just to blame Trump?

With Chinese New Year celebrations commencing now should be the time that a deal gets signed.

Elsewhere, Europe is slowing sharply, various political issues, masked by Brexit, are putting severe strain on the EU structure, the imminent end of Merkel’s reign and France’s free pass to break the budget rules whilst Italy was hauled over the coals isn’t good.

If the UK does leave then the power base swings decisively towards Germany at a time when they may soon be a more German centric leader.

With Deutsche Bank in trouble,Europe remains at the epicentre of risk. However, with the Fed having pleased the market all eyes will now be on Trump and a possible trade deal with China. He is also at war with Congress over his promised border wall. Markets don’t really fear US Government shut downs as they are always temporary. For now what they want is a trade deal and soon, otherwise we might well see more cuts to profit growth expectations, which would not be good.

Let’s hope the Chinese New Year proves to be a prosperous one!

January2019

Click Here for Printable Version

This information is not intended to be personal financial advice and is for general information only. Past performance is not a reliable indicator of future results.