Click Here for Printable Version

Markets had been concerned about the Russian military build-up on the borders of Ukraine, the expectation was that if they were going to invade it would be a limited incursion into the Russian speaking areas of the eastern part of the country. Whilst a full scale attack focussing on the capital city Kiev was always a possibility, it was thought, one with a very low probability.

When the move came markets were initially surprised and fell sharply, but share prices followed the maxim of the great Victorian banker, NM Rothschild who recommended “buy at the sound of cannons”.

However, since then, the situation has become very complex and very fluid.

Far from a brief border skirmish this has become a full scale war with the Ukrainians putting up heavy resistance.

This brings a whole range of unexpected risks and uncertainties for the global economy and at present the ultimate outcome is very unclear. The two positives are that Russian gas is still flowing into Europe and that China has not fallen into step with the Russians. This is perhaps, for the long term, the single most important aspect of this whole sad event.

Markets are of course, as ever, mercenary, they look through conflicts and try to assess the financial risks, but also seek out opportunities.

Fundamentally, Russia was just 1.75% of global GDP and the Ukraine 0.2%. The single most significant event so far for markets (given the gas is still flowing) is the suspension of some (not all) Russian banks from the Swift system. This was part of the planned sanctions, but it is where there is risk.

European banks have a small but significant financial exposure to Russia. Whilst no one is expecting a “Lehman moment” as stress tests have already taken place, markets will be alive to any default costs that might arise from a possible collapse of the Russian banking system.

If the West is starting to wage full economic war (not there yet) on Russia then it needs to be prepared for the possible consequences, particularly to already high levels of inflation.

For now, oil and gas prices are at the front and centre of the market’s thought process.

Commodities

In a market that is currently concerned with high inflation and how in particular the US Federal Reserve Bank is going to react, yet another supply shock is not good timing.

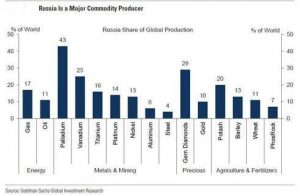

Russia is a relatively small economy and one that is almost wholly commodity based. The following table highlights the range of commodities that it exports. Ukraine is also major exporter of wheat, mainly to Turkey and the Middle East.

What further complicates the picture is Europe’s reliance on Russian gas, estimates are that between 30% to 40% of Europe’s gas comes from Russia.

Last year the UK imported only 4% of its gas needs from Russia. So far there has been no formal disruption, as Russia is going to need the cash and gas payments are (currently) excluded from the Swift ban.

But many shipping, insurance and other companies are refusing to handle Russian commodities. This is self-sanctioning from the business community in support of Ukraine.

In a global commodity market where supply, due to the impact of Covid 19 (many parts of the world are still in lock-down) is already very tight, further disruption is not welcome.

But history tells us that such supply shocks are usually temporary, so it is not the disruption that is important or the actual prices, it is the response of Central Banks that counts.

Here the picture is complex, their main aim was to withdraw the exceptional Covid stimulus as soon as possible. Economies are booming and thus so are inflationary pressures.

So far these pressures are primarily coming from a shortage of labour, but higher oil prices are for now, adding “fuel to the fire”.

For Europeans it is about the actual supply of gas, for the US it is pump prices.

It is easy to forget oil was over $120 per barrel between 2011 and 2015, prices have been up here before.

Pre-Covid, US official interest rates, just two years ago, were 2.5% they are now 0.25%. The Fed is trying to get back there as quickly as possible.

However, the complexity of the current sanctions on Russia could well delay these planned moves.

Militarily, this conflict could last a long time, thus commodity markets and therefore the Central Bank reaction, will also be in focus for some time yet.

Much will depend on the fallout from both the present and no doubt future sanctions and particularly the impact on the banks.

Banks

Whenever the normal order of markets is dislocated there is always the fear of unintended consequences.

The sheer scale and breadth of the sanctions does raise the possibility of triggering something unforeseen in the financial markets and thus defaults.

Current estimates are that western banks have less than $100billion exposure to Russia, sounds a lot, but not in the general scheme of things.

The risk appears to be concentrated in the usual European suspects i.e. French and Italian banks, with Société General and UniCredit allegedly the most exposed, but then they have the most supportive governments.

Markets are looking for Russia risk and thus it shouldn’t be a surprise if they do find it. Central Banks would though be morally bound to help with short term liquidity.

So this shouldn’t be a huge danger to markets, but it does require monitoring.

Markets

Whilst it is hard to be dispassionate at this time, that is what markets have to be.

They are pricing mechanisms that look at the interaction of interest rates, inflation and earnings growth. It is possible that the scale of the sanctions might have unintended

consequences, especially for the banks. This could though make the indicated interest rate increases less likely, which is positive.

The poor inflation picture will though get worse before it gets better, which is not good. So whilst inflation is worrisome the fundamental drivers of profit growth for the markets, especially given China and Hong Kong are still in lock-down, are essentially unchanged.

Nevertheless, we have seen some pull back in share prices, which as the following table shows, in the context of history have been pretty modest, which suggests in the short term markets may have some further repricing to do?

What this shows is that the war itself has had a limited market impact, the fear is though, that with Russian commodities being shunned rather than sanctioned, it is raw material prices, especially oil, that is becoming the major concern.

The Russian focus on Ukrainian cities is likely, militarily, to make this conflict a long and difficult one, therefore Russian commodities are likely to be off the markets for some time. Thus, the inflationary pressure, which the markets may have initially thought to be temporary, might be more permanent.

Just how the Central Banks will respond is very hard to say and will be the key to short term market direction.

Given the conflict looks to be heading towards a protracted one, the US Central Bank meeting on the 16th March will set the tone of just how these higher commodity prices are going to be dealt with.

We also need to consider the ramifications of a possible collapse of the Russian economy, it is not a large one, but the risk of bond and bank defaults is rising.

Markets though will rapidly move on from the conflict as long as inflationary pressures dissipate or the Central Banks ignore them. Markets hate uncertainty and that’s what we have at the moment, the Ukraine, commodity price inflation, Russia itself and the reaction of the Central Banks.

However, history tells us it never pays to be too pessimistic, as the above table shows, 18 months later equity prices are significantly higher. This is why we always recommend that clients maintain at least 18 months cash reserves.

March 2022

Click Here for Printable Version

This information is not intended to be personal financial advice and is for general information only. Past performance is not a reliable indicator of future results.