Click Here for Printable Version

February saw volatility finally return to markets with a vengeance. In the complex world of derivatives there was a very largespeculative position in the traded Volatility Future.

This particular market was leaning too far in the wrong direction.

Sensing blood and with one piece of US data suggesting an inflationary increase in wages, traders sought to unseat this huge position and were successful.

Everything in the markets is connected in a web of interaction; thus shares entered a correction phase, as we talked about last month.

But we have to be clear this isn’t investment, it is the daily noise of speculation that is an increasing part of the very short term marketplace.

As long term investors it is just the irritating and necessary noise we have to live with. It also highlights that to trade requires a very sophisticated understanding of the various technical nuances of modern financial markets.

In the meantime Donald Trump continues to make mischief, this time on trade tariffs, which promoted the resignation of highly respected Gary Cohn as his Chief Economic Advisor.

The Volatility Index

A key part of the underlying equation is Volatility.

Options act primarily as an insurance contract allowing fund managers to protect capital against major falls in markets. Just like insurance if the risk increases (e.g. you live in a flood area) you would expect to pay more.

Volatility therefore increases when the perceived risk is high and reduces when it is low.

This value, like everything else these days has its own index which can be traded. This is known as the VIX. As this chart of the VIX shows, during the Credit Crunch of 2008/09 it shot up from 14 to 90, and occasionally spikes up to 50.

In February, out of blue, we had another such spike.

This spike in the VIX was caused by a market technicality but led to primarily US based investors seeing a total loss on some of their Volatility Exchange Traded Note investments.

We have highlighted the risk of ETN/ETFs before, primarily in the context of High Yield Bonds.

These products are sold as “cheap” investments that do better than traditional active funds.

Often they can do better, but only in certain market conditions i.e. like the current one.

When they invest in Futures, as these did, there is the potential for total capital loss.

This is because a Future has a finite timespan and can expire at a substantial capital loss.

In this case the Futures didn’t expire at zero but the rate of change in the underlying VIX price was so rapid that the fund’s maths collapsed.

Whether this was due to market manipulation is now down to US regulatory authorities and this will be decided at some time in the future. In the meantime it is a salutary reminder that markets are risky and investing in anything other than “real assets of real companies” always has the potential to go horribly wrong.

Italy

Markets rarely have Credit Crunches, 1929, 2008 are the two key examples and there was one in the UK in 1974, they are nasty, dangerous and hard to predict.

We have previously written about the risk of Italy leaving the EU and critically the Eurozone.

This has the potential to cause a collapse in the whole European banking system and thus raise the risk of a new Credit Crunch.

The Italian Election has seen a big swing to the nationalist/populist parties.

So far, a new government has yet to be formed and thus markets have not as yet had to price in a possible “Italexit”.

However, this remains a possible risk, but not as yet a probable one. Nevertheless we have to be aware that it exists.

Alternatively, could it finally stimulate the much needed EU reforms?

If these reforms do happen could the UK change its mind? It never pays to have a closed mind in investment markets.

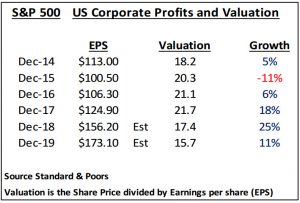

US Company Profits

As the list of geopolitical risks seemingly gets longer and longer and inflation and interest rates tick up, you would logically expect the markets to pull back.

However, all these risks are just factored into the market valuation.

Fewer risks equals a higher valuation and vice versa.

But when the denominator of the investment equation is growing so rapidly then markets should continue to go up.

A quick fact check after the end of the first quarter results season shows the dramatic acceleration in US corporate profits.

The markets are sceptical that these forecasts (from the companies themselves) can be achieved. If they can then the market is cheap and any dips in the markets should continue to be bought.

Trump Trade War and Gary Cohn

Trump seems to have been re-energised by his tax cut success, and he is now moving on to other items on his policy agenda.

We need to remember that Trump’s policies are based on speaking to the conservative “Rust Belt” of America, the people that voted him in and could re- elect him.

He doesn’t care about Los Angeles and New York; they will never vote Republican regardless of who the candidate is.

His trade strategy is purely political, there is no economic logic to it, and it is shameless electioneering.

What has become reasonably clear so far is that whilst Trump dominates the soundbites often there are tweaks and get-out clauses that seek to minimise the economic damage of many of his policies.

A trade war would not be good, and the markets corrected on the announcement, but they then recovered on the use of “friend” status exemption.

This move then increased the pressure on Canada and Mexico in the NAFTA talks.

Markets have realised that they have to careful in over interpreting Trump’s rhetoric.

The sad news from the Trade announcement was the resignation of Gary Cohn as Chief Economic Advisor.

Having a Wall St insider sitting on the top economic seat in the White House administration was a source of comfort.

Again though, we have to careful at over analysing this, Cohn may be looking at promotion within Goldman Sachs, which is personally more valuable to him than sitting at the top table with Trump.

Markets

Bonds:

The key 10 year US Treasury continues to hover just below the 3% level. Even at this level it does seem to be poor value as US growth accelerates and thus inflation should inevitably follow.

In the UK the Corbyn/Sturgeon risk is a real one; at 1.5% the UK 10 year Gilt does seem to be very poor value.

For Bonds, it is all about inflation, we have recently seen the first signs that US wages are starting to rise and the Federal Reserve Bank may now struggle to catch up with economic reality.

UK Equities:

The FTSE 100 continues to underperform. The mix of industries that dominate our market is very defensive e.g. Pharmaceuticals, Tobacco and we have no big Technology companies.

Fundamentally, an over exposure to the UK is one that is very focused on just a few industries.

For now though, the UK manufacturing economy continues to outperform all forecasts, and sterling has continued to recover.

Though, worryingly, London house prices have continued to fall. Political risks remain very real in the UK, as they do in Europe.

Summary:

How Italy develops over the next few months will be very critical for the short term development of markets. With Merkel so weak the European risk is now very elevated.

Nevertheless, the Trump trade continues, we cannot ignore the fact that corporate profit growth is accelerating to what are historically very high levels.

This, in theory, should feed into higher share prices.

Having said that, there are immense headwinds, rising inflation and thus interest rates, Italy, FBI investigation into Trump etc. All we can say with any certainty that volatility is back is we should expect the ride to be lot more bumpy from now on.

February 2018

Click Here for Printable Version