February was the month when the FTSE100 finally touched a new all-time high after 21 months of going nowhere. This has been in marked contrast to other global markets and shows the benefit of having a properly diversified portfolio.

The two big geopolitical risks that are facing markets, Greece and the Ukraine, saw developments during the month but neither is anywhere near being resolved. The usual European strategy of, “kicking the can down the road” for as long as possible and only make a decision when you really, really have to, remains in place.

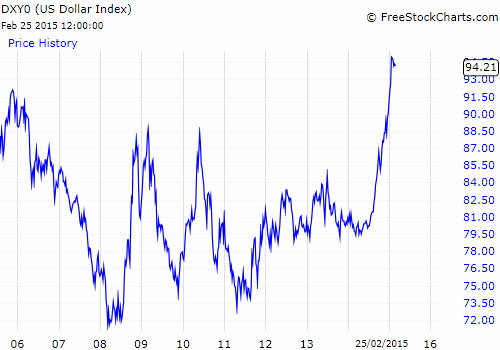

In the Ukraine there is a ceasefire, which no one expects to last, there are few signs that the lifting of sanctions against Russia is at all possible. In the meantime separate testimony from Janet Yellen and Mark Carney made it clear that they see the current low levels of inflation as temporary and they intend to raise interest rates as soon as the inflation data justifies it. In the UK, politics is beginning to become a concern and in the US a strong dollar appears to be having an impact on the juggernaut of US corporate profit growth.

US Corporate Profits and the Dollar

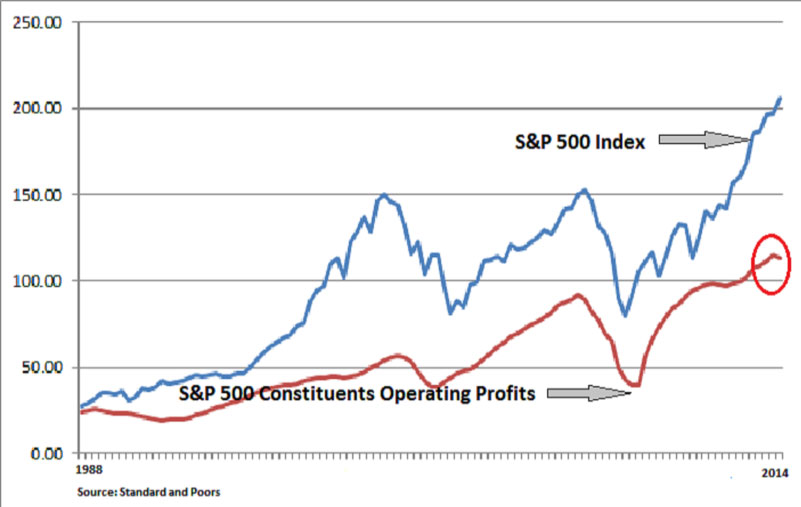

With 90% of S&P 500 constituents now having reported their fourth quarter 2014 profits, we can analyse what this means for equity markets. We know that share prices can only rise if company profits are rising as well.

The above chart shows the direct relationship between profits and share prices, i.e. when operating profits fall so do share prices. What is therefore slightly disconcerting is that for the last quarter the annualised operating eps fell by around 3%, which this is the first fall since 2008.

This is potentially hugely important, but only if this marks the start of a trend. Such data is often revised or recalculated and expectations at the moment are that profits will end 2015 up by 4.8% compared to 2014.

Nevertheless, we do have to be aware of the reasons behind this fall and make a judgement of whether they are transitory or not. If we look at the individual company announcements the culprit is clearly identified as the strong dollar. This has had an impact on company profits from currency translation and also unit sales.

US goods and services priced in dollars are becoming uncompetitive, particularly against European ones priced in euros.

If we then add in the negative impact from the oil sector, due to the collapse in the oil price, then the drop in corporate profitability is understandable.

Forecasts are that a pick-up in consumer demand in Europe will take up the slack but not until the 3rd and 4th quarters of 2015.

Markets can look through such blips, but for now, we have to watch carefully that this does not become a trend.

UK Politics

The UK General Election in May is getting closer and March 18th will see the Conservatives last big opportunity to sway undecided voters with the Budget.

This is potentially the most fascinating and dangerous election for many years, with some commentators suggesting that the last time the result was so unpredictable was when women voted for the first time. At the bookies and in the polls a hung Parliament remains the most likely outcome, but the odds for a Conservative majority have now moved ahead of a Labour one.

US style Approval Ratings place Davis Cameron way ahead of Ed Milliband which adds a further flavour into the mix of increased support for UKIP, SNP and the Green Party.

Pollsters also point out that the infamous “swing group of voters” is now larger than ever, as traditional party voting on historic lines disappears. For now, the view is that the Conservatives may win the most seats but this might not be enough to form a government; if they win enough seats a Labour/SNP combination may be the only workable coalition option.

It may well be that a re-vote will be needed. Normally this wouldn’t be a problem but it brings onto the agenda the possibility of a rerun of an independent Scotland, possibly with the Bank of England forced to accept monetary union and “Brit-exit” from the EU. All of which, have the potential to distort markets.

Barclays Bank

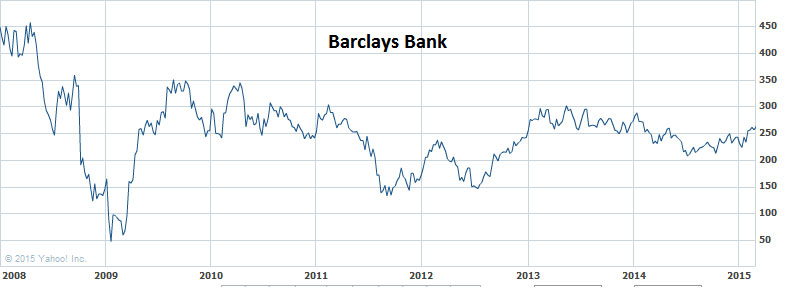

Recent results from Barclays Bank highlighted that, despite a recovery in underlying profits, these issues have not gone away. Net income from personal and corporate banking, despite a booming London housing market, was unchanged, which highlights a continued reluctance to lend.

Costs were cut by £1.8bn, with 14,000 jobs lost thus helping profits; Tier 1 Capital was up to over 10% but provisions against litigation continued to rise. These now stand at £1.25bn but analysts estimate this figure could rise to over £5bn. Suffice to say the banking sector is not fixed, yet.

Greece / Ukraine

These two big geopolitical issues remain a worry for markets, Greece has been deferred, and in the Ukraine the current ceasefire seems to be holding for now.

Markets need to see some sign that a permanent solution has been reached and thus Russian sanctions might be lifted, as we write this seems unlikely.

Indeed, with large numbers of US military “advisers” being deployed to the Ukraine it could be argued that the issue is being escalated.

Markets

As time marches on so does the cycle, as each month passes we get closer to the US Presidential election and thus a possible politically inspired recession in 2017.

Janet Yellen, remains “dovish” in her speeches to markets but makes it very clear the inevitable move up in interest rates is very much data dependent.

Any sign of inflation or the underlying drivers of inflation picking up, interest rates will rise. Neither Janet Yellen nor Mark Carney (Bank of England) are in the deflationist camp.

They are seeing the US and UK economies returning to normal and if the oil price hadn’t collapsed we should have been expecting the interest rate to be going up about now.

But to use a driving analogy they would be moving the throttle pedal to cruising mode rather than accelerating. They are nowhere near touching the brakes, as yet.

In Europe the announcement of the modest, but still bigger than expected, QE programme is helping to force down the euro against both the dollar and the pound.

Good news for German exporters not so good for US ones. The hope is that an economic recovery in Europe will outweigh the impact of a stronger dollar on multinational corporate profits; the danger is that at the moment this is an expectation rather than a reality.

For now though markets are seemingly prepared to look through this risk and cash is flowing into equities, especially as the taste for poor value bonds seems to be abating.

For the UK though, March is a big month, will the Conservatives create a vote winning budget? Indeed globally, as the quarter end approaches we also need to watch for currency inspired profits warnings.

If growth falters up go valuations and the markets could start to look expensive.

February 2015

Click Here for Printable Version