2014 proved to be an unusual year for investors. Returns from the major asset classes varied enormously and highlighted once again the true benefit of ensuring that investment portfolios should be as diversified as possible.

The FTSE was down by 2.7% but Gilt prices rose 10%, and Global Equities also increased by 10%. But all this is now history; we must look forward to 2015.

Regular readers will know that the investment world follows a cycle, and on average this lasts for around 5 ½ years, crucially as the market bottomed in March 2009 we now are over this timeframe. Theoretically therefore, we are due a recession. This is important as corporate profits collapse during recessions and thus shares become expensive and have to fall.

But we have not had a “normal” recovery, so can we reasonably utter the most dangerous words in investment “will it be different this time?”

What should we be looking for?

We need to watch for Central Banks, and by far and away the most important of these is the US Fed, raising rates in order to deliberately slow down a booming economy to choke off rampant inflation.

But have we got a booming economy, is inflation in danger of spiralling out of control? US interest rates at 0.5% are abnormally low and need to normalise, but will a process of normalisation, say rising to 1.5%, precipitate a US recession and thus a collapse in US and global corporate earnings?

Based on current data the case for a major increase in US interest rates is slim. However, markets are tricky things; they are not valued on what is happening today but on 12 to 18 months in advance.

So the real questions is ……in 18 months’ time will the US and Global economy be growing to an extent that inflation could get out of control and thus interest rates have to rise?

Global Growth

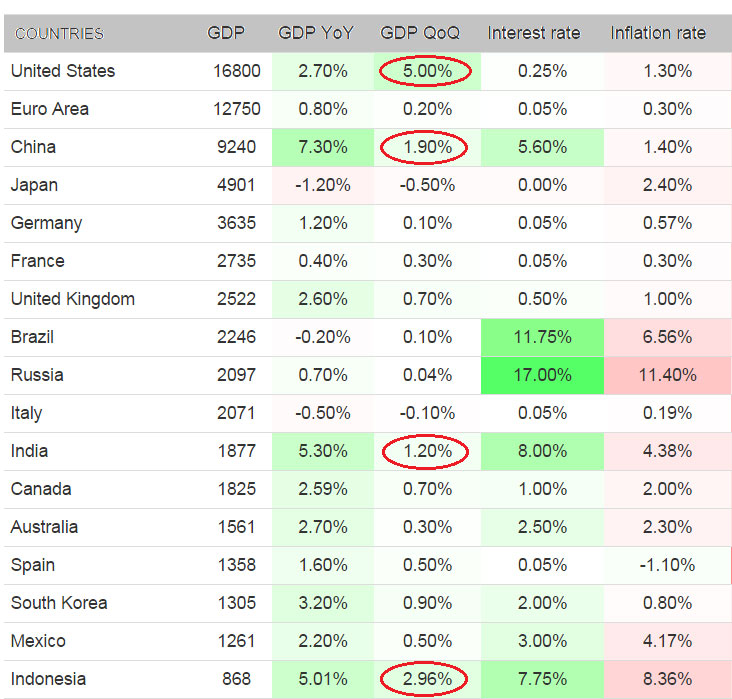

Generally speaking most of the growth is coming from the new world economies. The pattern is of high levels of GDP growth but this means high inflation and high interest rates.

The current aberration is the USA. We suspect that the last quarters GDP growth is a statistical fluke that will be adjusted, nevertheless economically such good levels of growth should ultimately lead at some stage to inflation. The current level of US interest rates is only sustainable if growth significantly slows down.

The table also highlights how many of the major economies are struggling, Euro Area, Japan, Brazil, Russia together an enormous percentage of global GDP, are either in or are flirting with deflation.

Not good news for those economies but crucially allows the US to grow without stoking up global inflation. For the UK the level of growth does justify an increase in interest rates, though we are concerned that our recovery is artificial and based on an unsustainable boost in the London housing market.

Meanwhile despite persistent rumours of an imminent collapse China keeps on growing, it simply shouldn’t be able to sustain this rate of growth for much longer.

However, the demographics mean that it will still be able to grow faster than the old world.

So it would appear that US growth is robust and accelerating, given that interest rates are below inflation (as a rule of thumb in normal circumstance interest rates should be about 0.5% above the rate of inflation) US rates must rise.

As long term investors it doesn’t matter when, but unless growth collapses (a low probability based on known events) they must rise from here.

Will this happen within the next 12 to 18 months? The balance of probabilities says yes, with most commentators expecting small upward moves this year.

Will this precipitate a recession within the next 12 to 18 months? The balance of probabilities says no. No-one is expecting a US Central Bank induced recession. (There are still many who don’t believe in the recovery and that growth will slip back) this is not the same as a Central Bank induced, inflation choking recession.

Ultimately though, it all depends on inflation. If inflation rises, so do interest rates, regardless of the state of the economy.

Inflation

The good news is there is no sign of inflation picking up either in the USA or the UK. The Fed and the Bank of England do clearly have itchy trigger fingers but there is, at the moment, no justification to increase interest rates to choke off inflation.

They do want to “normalise” rates to be closer to the inflation level, about 1% for both countries is sensible, but this is not the 5%ish level that could trigger a recession.

This is why the collapse in the oil price is such a “big deal”; it will stimulate growth and reduce inflation at the same time.

Both Central Banks are focussing on wage growth as an early indicator for inflation. There is excess capacity within these economies which limits the scope for wage increases. Both the US and UK have flexible labour markets and a laissez-faire approach to immigration which for now will limit the upside for wage increases.

So based on economics only, the cycle should be safe for now, it is though constantly moving and evolving and as time moves on this picture will change.

But the world is not just the USA, together Europe and China, are both major parts of the global economy and economic meltdown in either could trigger another global credit crunch and thus a recession.

Europe

Europe as the above Global Growth table shows is in a mess. The problem is political, which has frozen the economic management, and the fundamental structure of the European Union. The EU has evolved beyond a free trade area, and is now at a halfway house stage between a trading area and a Federal State.

It has the trappings of a United States of Europe with a Parliament, single currency and a Central Bank but without the legal, tax and political structure to make it function, nor the European Gilt needed to fund it.

It needs to move forwards or backwards; the unfortunate likelihood is that it will do neither and simply bumble on and hope that US and Chinese growth will help the Germans to sell more Audis, Mercedes and BMWs. For the rest of the world this is fine as long as one of the indebted Mediterranean countries doesn’t go bust.

If handled badly this could cause the dreaded contagion and impact on the global financial system. Having said that, there are many who are secretly hoping for such a crisis as this could be the only thing that forces the Europeans to address their fundamental structural problems.

China

The Chinese reform process is ongoing, this is an economy that is still centrally planned and historically lacks innovation (recent history).

Mass urbanisation does continue to drive growth as does the creation of a new “mass affluent” middle class.

History tells us that when this happens a country needs to reform and quickly. China seems to have recognised this and appears to be more accepting of political protest. State shackles on many businesses are slowly being removed and free trade zones where state control has been removed completely are being trialled. The new leadership is making progress.

For investors the development of new market leading Chinese technology companies is more interesting. Alibaba is now the biggest Chinese company and the likes of Xiaomi are making Apple quality devices at bargain prices. The risks of a property crash and ensuing financial credit crunch are high, but unlike their western counterparts, the Chinese government is flush with cash, the Chinese public are great savers rather than borrowers and the reform process seems to be targeting this area. Crashes happen unexpectedly and not when they are widely forecast.

China is not without risk but the long term numbers are too compelling to ignore.

Market Valuations

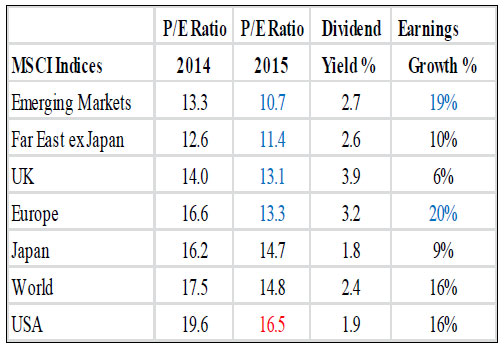

(Source MSCI)

To our eyes the forecasts look to be overly optimistic and we have to factor this into account.

Nevertheless valuations are still reasonable. The USA after its good run in 2014 is looking expensive and as this makes up about half of the World Index does drag this figure up.

The most attractive major markets are Europe and the UK and in the new world the Emerging Markets and the Far East are very cheap indeed. This is a major positive for Global Equity Markets.

Market Themes Number One- Politics

January sees a Greek General Election and there are fears that the anti-EU Syriza party might hold the balance of power. This could bring the Greek crisis back to life! In the UK May sees what is likely to be the most unclear election for some time.

The Conservatives could have their vote split by UKIP and Labour whilst leading in the polls may suffer equally from a resurgent SNP in Scotland as well as UKIP. As ever the bookies give us the best view of what may happen and odds for a hung Parliament are 2/5, Labour 7/2 and Conservatives 9/2, not good news, especially for Gilts. Cameron may have to offer the prospect of a “Brit-exit” from the EU and stronger policies on immigration to try and win the UKIP voters back to his cause. Good for votes but not for UK plc. This could all turn into a headache for the markets. In the US the Presidential Election is not until November 2016 and he or she will not take office until early 2017.

However, Obama has lost both Houses of Congress and now has limited powers, so politics will be an issue in the US and electioneering starts soon.

There is already speculation as to who will run for President, it is very early days and for what it is worth the bookies are suggesting it will be Hilary Clinton for the Democrats and Jeb Bush for the Republicans.

Market Themes Number Two- Geopolitical Risks

Ukraine, the Islamic State and the associated oil price war are issues that are yet to be resolved. There are few signs of resolution and the impact on Russia could yet have severe financial ramifications for markets.

Russia must now be in full recession and the risk of Russian corporate default is rising all the time. European banks seem the most exposed and these are the same banks that have not as yet fully resolved their 2008/09 non-performing loans.

A “perfect storm” for the European financial system would be a combined Greek sovereign and Russian corporate default. Greece has been and will be hard to resolve, Russia would be far easier, it depends on one man.

Putin would need to do a deal over the Ukraine then sanctions could be lifted. The falling oil price would still be a problem though. Military websites are suggesting a full blown offensive against the Islamic State in the spring, however, the Saudis would like Assad in Syria toppled and it is hard to see how an offensive against Islamic State would suit them with him still in power?

The extent of any offensive, if it happens, maybe to secure the Iraqi Shia border and Kurdish lands? Suffice to say Geopolitics will remain a major and unpredictable theme in 2015.

Market Themes Number Three- Cyberattacks

The UK Chief of Defence Staff has for years been telling us that Cyber Warfare is the biggest threat facing the UK notwithstanding the usual terrorist threats.

The alleged North Korean hacking of Sony Movies in the USA has highlighted the reality that the connected world is also an open one and a country’s infrastructure assets such as power stations, air traffic control, electricity supply networks as well as the banking and stock markets systems may all be open to attack.

The relatively harmless Sony attack has brought this potential problem to the front of investors’ minds and also to boardrooms around the world. Flash crashes in complex trading systems are becoming increasing common, sooner or later one will be blamed on a cyberattack.

Investment Strategy for 2015

So what are we looking for in 2015, same as in 2014 growth? In the UK and USA growth is healthy and we need this to continue and in some areas accelerate.

Remember we need companies to make profits in order to pay dividends and thus ensure their share price keeps rising. The cycle remains intact for now, it is probable that both the US and UK interest rates will rise in 2015 but not to the extent that equity markets should fear recession. Bond prices remain elevated and if inflation does pick up prices must fall.

Again this is not imminent but over the long term bond investments must represent poor value. So far, the ending of US QE has not led to a slowdown in economic growth but there is a fear that the recovery remains fragile.

If this is true then there are plenty of geopolitical risks around that could delay the recovery, but delay is the key word here, it does not change the long term big picture.

We have growth and cheap valuations, thus share prices should rise, but also we should expect a return to normal, higher, levels of volatility.

So in terms of client portfolios we have already taken steps to reduce the risk profile of our Cautious investments which are invested in Gilts and Bonds. We may be a bit premature but after the strong run in Bond markets last year banking the returns we believe is a prudent strategy.

For equities the underlying backdrop remains positive. Dividend yields around the world are at highly attractive levels and are growing as well. As ever we should expect volatility, it is the unpredictable nature of geopolitical events that will cause swings this year, and especially the UK General Election.

Long term a lower oil price will provide a major boost to the global economy and it is a major positive for markets and inflation expectations.

This should finally help the global economy return to something approaching normal for the first time since 2008. Europe remains a worry, but this is now reflected in below average valuations.

For January the usual Santa Claus hangover has arrived early, worries over Greece and falling oil prices are hitting big index constituents such as Exxon and Shell. The Greek election will dominate the news flow, but just as before it will pass, and the positive background will reassert itself. Do we need to worry about excessive growth in 18 months’ time, no, not yet?

December 2014

Click Here for Printable Version