Click Here for Printable Version

Market Update Coronavirus

In modern times what is currently happening to people around the world is unprecedented, not since the Spanish Flu of 1918 has a virus pandemic hit the global population to this extent.

Clearly, the most important thing is for our clients and their families to stay healthy at this difficult time. Many clients will know that “your health is your wealth” and what we at SRS can do is to reassure you that financially these events are always temporary, they will pass and for clients to concentrate on their health and let us worry about your wealth.

In our most recent newsletter we highlighted our long term portfolio roadmap in the context of the coronavirus and put forward two scenarios.

The first scenario was based on the coronavirus being contained in China with only marginal disruption globally, we have reprinted the second “Scenario 2” below and also updated the roadmap.

Scenario No. 2

“The virus spreads and deepens and forms a true Pandemic. Governments globally follow the Chinese example and shut down their economies. This precipitates a supply shock which causes widespread financial consequences to companies.

These consequences could lead to staff being laid off and bankruptcies accelerating.

Bad debts rise at the banks risking a “credit event”. Sounds dramatic but actually just a normal recession.

Again the impact would be mitigated by Central Bank action and China recovering.

This should be reflected in the markets through a “High Volatility” event. We must note that such recessions, that are caused by shocks rather than interest rate increases, tend to be shorter than normal i.e. no longer than 12 months.”

Unfortunately the above has come to pass.

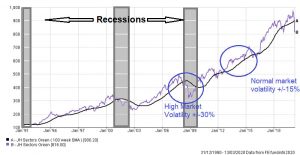

Since the start of the year equity indices have fallen by 30% and the roadmap portfolio by 20%. (Over 12 months the decline in valuations has been around half that). Importantly, looking at the above chart we can see that in a historic context there is nothing unusual about the current price action in portfolios.

We have seen it all before.

There have been 13 recessions since 1929, these have led to an average peak to trough fall in the S&P 500 index of 35%. Currently the S&P is down by 30% . So we can say that markets are doing what they always do, they are pricing in a decline in corporate profits and we must stress they are moving well within historic precedents.

What is different this time is that economies are now under the management of Health Ministries rather than the Treasuries.

This means that financial markets have to ignore tried and tested economic statistics to try and identify market cycle turning points and look at medical ones instead.

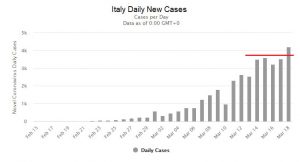

During the SARS epidemic it was a decline in the number of daily new infections that marked the turning point. It seems that the markets are once again fixating on these numbers.

In China and South Korea, once the number of new cases per day went over 100 then the infection numbers rapidly accelerated.

In China they peaked 22 days later. In South Korea it was 13 days later (they it seems were particularly well organised). Italy is currently on day 20 and might just be seeing a plateau in the number of new cases? In the crucial US economy the trigger point was on March 7th which would predict that they will not peak until around March 29th or so?

The UK would be later as it is a week behind the USA. So if the SARS investment pattern repeats itself then we should in the next few weeks be seeing “peak new cases” in Europe and traders may then start to speculate on an end to this crisis?

Daily new Coronavirus Cases

source: worldometers.info

For companies, the financial ramifications will last longer maybe over 12 months but it is very important to remember that markets are not priced on what is happening today but what may happen this time next year.

So we will get the classic post-recession bounce in share prices whilst the corporate news flow continues to deteriorate.

Markets bottomed in March 2009 but it was April 2010 before the global economy turned upward.

Could share indices go lower and touch the 50% move down (and thus portfolios touch the max historic volatility of 30%)?

Well yes they could, but again based on historic norms they rarely stay down at these levels for long. Such a move is usually the final flush-out of weak traders and nervous investors and precedes the turning point.

What should clients do? The old adage is “in a market rout do nowt”. We have always stressed the importance of having 18 to 36 months of additional net income needs in cash, periods such as this are exactly the reason why.

For those with excess cash (and strong nerves) there is a high probability that these events mark the long overdue end of the old investment cycle and when the turn comes, will mark the start of the new one, especially given the magnitude of the global economic stimulus that has already been announced.

Why is this important? For those investors with a long enough time horizon, buying well below the long term trend (as we are now), obviously leads, to significantly higher returns over time, than for those that prefer to wait for the air to clear.

19th March 20

Click Here for Printable Version

This information is not intended to be personal financial advice and is for general information only. Past performance is not a reliable indicator of future results.