Click Here for Printable Version

The pattern we have seen through the summer has continued. US and Far Eastern technology stocks have seen big percentage increases in their already huge market capitalisations, whilst other stocks and markets have gone nowhere. In the year to end August the US Nasdaq 100 index which includes Apple, Alphabet, Amazon, Facebook, Netflix and Tesla is up by 36% whereas the UK’s FTSE100 is down by 21%.

This is not a UK only issue, the French, Australian, Hong Kong, Singapore markets amongst others, are down by similar amounts.

Many commentators are comparing this performance to the “Tech Bubble” of 1999 and 2000 where concerns over Y2K meant that demand for new computers and servers was exceptionally high.

Has the Covid-19 pandemic created a similar one off boost in demand that will dissipate once/if employees finally return to their offices?

The virus is being far more persistent than the markets first thought. However, governments are keen to avoid economically damaging total lock-downs and seem to be waiting for a vaccine(s).

Greater testing means more cases are being identified, yet treatment is improving and thus the mortality rate remains, thankfully, lower than before. As the summer comes to an end we are entering a period of heightened geopolitical risk.

The US Presidential election is starting to impact markets, the polls favour Biden though Trump is doing better in the key decisive States, but there is a long way to go and the news flow will at times move markets.

In Europe and the UK the trade negotiations, or rather lack of them, is starting to make headlines.

However, the markets are anticipating that, as usual with the EU, nothing will happen until the very last minute. The key arbiter on this issue is the sterling/euro exchange rate and this remains well within its long term trading range.

Technology Sector

Source: S&P Dow Jones

The big US technology shares, collectively known by the acronym FAANGs have become traders favourites since the pandemic took hold.

Just like 1999 we have seen the return of “day-traders”, indeed some have suggested that with bookies and casinos closed across America and with no sports to bet on, gamblers large and small have turned to the stock market.

History does tell us this rarely ends well! Nevertheless, there is some justification behind the price rises. Firstly, sales are rising and accelerating whilst other businesses are being hit by the recession.

The market as a whole is seeing sales decline by over 10% and there are fears that this lower level will become a “new normal”. If so then tech rather than being volatile and risky is actually becoming a critical resource just like water, gas or electricity.

Valuations are incredibly (scarily) high but there is an argument that as these businesses spend far more on Research and Development than old economy businesses, their profits are artificially depressed.

Their true profitability can be seen in their staggering cash balances, bigger than the budget of most countries!

Whilst the pandemic remains, it is probable that these companies will keep benefitting.

The big risk may come when either a vaccine arrives or the virus burns out and the global economy returns to normal, could they experience the same hangover as they did in 2000?

It is perhaps no coincidence that Tech shares have wobbled as individual US States have been told to prepare for a vaccine from the 1st November.

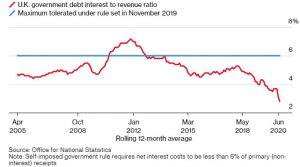

How Is The UK Going To Pay Off £2trillion In National Debt?

Chancellor Rishi Sunak has been on a spending spree, he had no choice, the government told businesses to shut down and quite rightly the government has attempted to cover employment costs in compensation.

As has been widely reported this has pushed the government’s overdraft (the Public Sector Borrowing Requirement, PSBR) to record levels.

This is then funded by primarily issuing debt (Gilts) which then becomes the government’s mortgage.

The obvious reaction to this is that the debt has to be repaid and thus the government needs to increase its income to do this, normally by increasing taxes and/or cutting spending.

This was the post 2009 strategy followed by the Cameron/Clegg coalition that led to austerity and a decade of low growth.

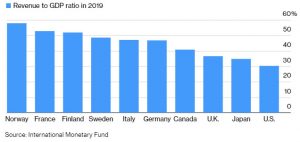

As the second chart shows there is room to increase tax. The UK’s tax take is low by European standards, but those that are significantly higher are either small economies or in case of France and Italy ones that have not grown for over 10 years, thus supporting the economic theory that high taxation leads to low growth.

But as the first chart shows he doesn’t actually have to do anything. QE means that interest rates are very low and thus whilst the amount of debt has ballooned the servicing costs have actually gone down to a record low!

Clearly this is a neat trick and falls into the classification of “smoke and mirrors”, but it does buy Sunak time and crucially leaves headroom for true Fiscal Stimulus should it be needed.

Markets

It would be easy to look at the headline US stock market indices and assume that markets are well on the road to recovery.

However, as we keep saying Tech, Healthcare and Supermarkets are all doing well, everything else remains stuck in neutral. This chart shows the forward Volatility Index for the US stock market.

During periods of panic it shoots up and in long bull markets it moves below 25 and stays there for many years. It has come down from its recent high but it is telling us there is still tension within markets.

One of the reasons for this could be the forthcoming US Presidential Election. Also it could reflect institutions buying insurance protection as the tech names move ever higher.

Just like normal insurance, buying option protection is a market and brokers will charge a higher premium if demand exceeds supply. Volatility is a key element of the insurance price. Whilst this is not a massive red flag it is indicative that under the surface some market participants remain twitchy and perhaps worried that a vaccine may not come as quickly as first thought or indeed might not work?

Against this negativity though, those parts of the global economy that are not directly impacted by the virus are recovering at a far higher rate than expected.

Housing activity in both the USA and UK is approaching boom levels.

September 2020

Click Here for Printable Version

This information is not intended to be personal financial advice and is for general information only. Past performance is not a reliable indicator of future results.