We have been highlighting in previous “Market Views” that volatility in the global stock markets has been unnaturally low and we finished last month’s letter with the hope that “they don’t lose patience”.

With a range of negative pieces of news and with most market participants on holiday the markets did finally snap and “normal volatility” has been resumed.

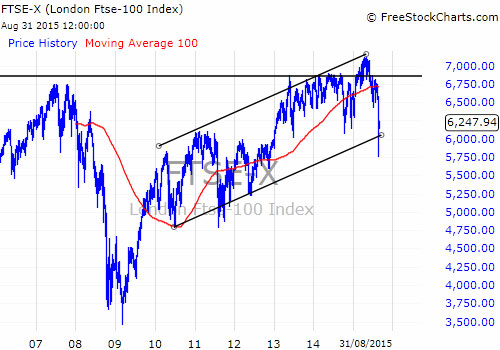

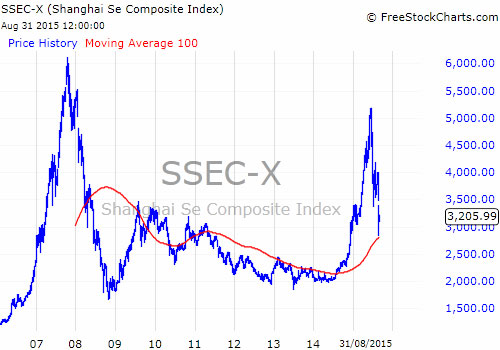

As the following charts show, so far, this is no big deal.

The markets remain in trend and the recent swing down appears no different to many that have gone before. But, we always have to ask ourselves, as the cycle is mature, is this, the beginning of a 12 to 18 months turndown equity markets?

Normally such turns in the cycle are caused by interest rates rising to choke off rampant inflation. US interest rates may soon rise but by a tiny amount, and inflation remains stubbornly low, so what is going on?

What are the reasons behind the return of volatility?

We know about poor corporate earnings and a misfiring Chinese growth engine.

What was the particular catalyst for markets to break now when there have been many very important reasons that might have caused a correction before now?

Markets had become focused on a few key stocks and sectors, thus the slowdown in corporate profitability left many valuations exposed.

For example, Disney produced great results but was “priced for perfection”, as such, enough was enough and fund managers took profits. When market leaders like Disney fall after good profit news (and just before a new Star Wars movie) it is clear that markets have got ahead of themselves.

Then we have the impact of trading computers and the extensive use of sophisticated “volatility” funds. These funds, due to their complex structure, were forced sellers when volatility moved upwards. JP Morgan estimates that these funds had to sell $100billion of equities during this move, and could have a similar number to go! In August, with few human beings around, the computers seemed to take over. When such a change in market temperament takes place we have to focus on valuations, which as we have written extensively about aren’t particularly cheap at the moment.

Furthermore, the bond markets are more efficient at pricing risk than equities. Bonds focus on company balance sheets whereas equities look at profits.

The yields in high yield bonds (lower quality companies) have recently increased (so their capital values fell).

Equities therefore became expensive versus high yield bonds and the gap was too wide and had to narrow.

With overall global economic growth prospects seeming to diminish, the chasm between the real economy and financial asset prices grew too wide and the markets have had to reprice shares.

Global growth expectations may still be too optimistic, but the consensus is now moving toward more realistic forecasts after being too high. Moreover, the fall in oil should, at some point, fuel an improved economy as the consumer starts spending again.

A US rate rise is imminent, albeit a very small one. But the major trigger event was China choosing to devalue its currency.

China

The devaluation, by a relatively small amount, of the yuan versus the dollar surprised the markets. They then started to fret as to the reasons why.

Could Chinese growth be collapsing? Might this explain the commodity price fall and what impact will this have on already struggling US corporate earnings?

rates are very high and the Chinese habit of unleashing a QE bazooka means that it is dangerous to write this important economy off. The Chinese do take the long view and the scope for this huge economy remains substantial.

There are also alternative views for the real reason behind the surprise devaluation.

One belief is that is perhaps more to do with the IMF, who on 4 August deferred the decision to include the yuan in the Special Drawing Rights reserve until October.

China seems to have taken the view that these are delaying tactics by the USA designed to keep the yuan out of this exclusive high status “club” and thus protect the dollar’s role as the global reserve currency. America has most to lose from China’s long term rise to global economic dominance. So the yuan devaluation and perhaps beginning a free float sometime in the next few years was a signal to the USA that, if she so wishes, China can dictate the global economic outlook through the foreign exchange markets? There may be no coincidence in China’s timing particularly as this move, ahead of a possible US interest rate rise on September, does inflict maximum pain.

The Federal Reserve Bank Balance Sheet

QE has in practice meant that the various Central Banks have accumulated $10 trillion of assets, this has kept interest rates low and monetary conditions lose.

But as QE has now ended in the US some of the bonds it holds on its balance sheet will come due for redemption in 2016. The accounting of such a redemption means that if these bonds are not replaced then the Fed is effectively tightening monetary policy.

The plan was originally fine, growth should now be fast enough to cope with this fact, but the current reality is that it remains below where it should be. Which means the Fed is stuck; to raise interest rates significantly now would be to increase this tightening perhaps more than they would want to?

Add in the Chinese devaluation and thus the selling of their US treasury holdings, means that they are effectively

tightening US economic policy as well.

So the Fed may wish to “normalize” US rates and could start the process very soon, but they really do need growth to pick up, otherwise we may have an accidental short recession in the USA.

Markets

So in the space of a couple of months we have moved from a position of accelerating global growth to a possible slowdown; good corporate profits growth to a decline in earnings; cheap valuations to average ones and finally accommodative central banks to the Fed possibly tightening.

Investors knew these facts but had the confidence that the Fed “had their backs”, that the dollar would eventually weaken and accelerating European and Chinese growth would push up profit growth in the final quarter and into 2016.

Now the market may have been spooked and for these same investors greed has evaporated and fear is back on the agenda. Is this the end of the current cycle?

Probably not, though the worst case could be a mild US recession and continued moderate fall in US corporate

earnings.

This would be very different to a full blown “normal recession”. Much will depend on the policy response around the world, do we get a Chinese QE bazooka; will European QE have the desired effect; will the US consumer

start spending again?

There is no immediate clear answer to any of these, so the markets have to price this in. We should therefore expect lower returns for now and a return to normal day to day volatility.

September will be a busy month, we have the FOMC meeting where US interest rates might inch up from 0.25% to 0.5% and we also have meetings for the G20, ECB in Europe and the PBOC in China. Oh and another Greek election as well! August has shown why it is important to have properly balanced portfolios that match your time horizon. It reminds us that markets are inherently not predictable in the short term. But this will pass, why, because it always does!

August 2015

Click Here for Printable Version