April saw the much anticipated first quarter US company profit reporting season. Virtually without exception results were pretty poor.

Forecasts had already been heavily downgraded ahead of the news and most companies merely matched these lowered numbers.

This is hardly the sign of a booming global economy. Looking back through our records, this time last year analysts expected the S&P 500 constituents to deliver earnings of $30.71, the reality so far with 75% of companies having reported is $24.97.

In normal markets an earnings miss of this magnitude is matched by a commensurate fall in share prices, this hasn’t happened, why not?

Well it’s partly the hope that a fully recovered global economy is just around the corner, and investors with a reasonable time horizon don’t want to sell just in case they miss out on the ever imminent “good times”.

Secondly, the belief is that the Fed and the other Central Banks still “have your back” and as such you shouldn’t “fight the Fed”. This view was called into question recently by the Bank of Japan, which has left some commentators wondering if we are approaching a change in Central Bank policy?

Helicopter Money

QE has kept the global banking system alive, but Central Banks are just one part of the triumvirate of global stimulus, government spending and commercial bank lending are just as or perhaps even more important for “normal” economic growth.

The problem with QE is that it creates super low and increasingly negative interest rates which means the commercial banks can’t make their “turn” on the difference between savings and lending rates so they simply shut up shop and wait for better times.

Governments meanwhile are still in austerity mode, so reliance is placed on the Central Banks.

They are in the process of rolling the last dice, negative interest rates. This is when they charge banks for having money on deposit with the central banks. The theory being it is better to lend at low rates rather than be charged for hoarding cash.

The problem is the banks are choosing the safety first option as their customers are currently comfortable doing nothing.

So the risk is a Central bank says to its government “that’s it we have done what we can, it’s over to you”.

The first glimmer that we might be approaching this step came from the Bank of Japan, who against expectations did not extend their negative interest rate programme.

This led to suggestions that it is about to pass responsibility to the Japanese government to stimulate a sluggish economy.

The old chairman of the Fed Ben Bernanke coined the phrase Helicopter Money, i.e. to get the economy moving you throw bundles of cash out of a helicopter, in reality this would mean tax cuts, subsidised wages and mortgages, as well as reduced regulation etc.

The danger is that the global economic supertanker is already moving, it is just not apparent as yet, governments would then be throwing petrol onto a smoldering inflationary fire.

London Property Market

Not only are corporate profits falling but so are property prices, albeit so far just in the overheated London market.

Demand for London homes under construction slumped by 33 percent in the first quarter as a new capital gains tax on overseas buyers and increased stamp duty dampened demand. The number of homes sold prior to completion in London fell to 5,947 from a high of 8,927 a year earlier, according to Molior London.

New builds are normally bought by international investors from Asia, Russia and the Middle East, but with currency issues and low oil prices buyers are not as flush with cash this year. In 2016 6,379 new homes were started in the first three months of the year, 39 percent less than a year earlier and the lowest number for seven quarters.

Developers in central London are now offering institutional investors discounts of up to 20 per cent on bulk purchases of luxury apartments as demand from international buyers’ slump.

Pension funds and asset managers plan to invest up to £30 billion in multi-family housing, according to a 2015 Savills survey; it will be needed to soak up unsold new developments. Property in general has been a strong investment for the past few years as the London effect has slowly rippled across the country. However, we do need to be wary that the overseas funded investment boom may now be coming to an end.

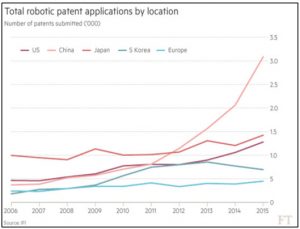

Robotics

Japan and China have demographic problems, not enough children have been born and their population pyramids are becoming distorted.

In the West, immigration is seen as the economic solution, in the East it is robotics. At the prestigious Milken Institute’s Global Conference, which discusses long term trends, robotics was the dominant theme.

Technology so far has tended to impact low-wage, low-skill jobs, but this is changing. They cited robots/artificial intelligence operating trucks in some Australian mines; corporate litigation software replacing employees with advanced degrees who used to sift through thousands of documents prior to trials; and on Wall Street, the automation of jobs previously done by bankers with MBAs.

Big banks have slashed thousands of jobs in recent years as businesses like bond trading have become less profitable.

Under pressure from shareholders to boost profits but unable to grow revenue banks have increasingly turned to technology to reduce costs.

But technology’s impact will extend beyond the City and Wall Street. Driverless cars are getting closer, consumers may not choose to give up their cars but companies like Amazon will use them for 24 hour deliveries, also Uber for taxi services.

Even Ford is investing heavily, changing from a vehicle manufacturer to a transport provider. History tells us that technological change is ultimately good for personal wealth but can cause short term disruptions.

Electric cars once outsold petrol in the USA, as female drivers in Edwardian frocks disliked the hand cranks needed to start engines, then the electric starter was invented and battery powered cars disappeared, until Tesla arrived!

It also shows that China’s inexorable rise to global economic dominance will not be through low cost manufacture for western brand names e.g. Apple.

China is preparing itself for its future population shortage and the inevitable managed decline of state owned basic industries such as steel. Until now, most robots have taken the form of high-precision preprogrammed industrial machines.

The cheaper more flexible machines that are emerging are designed to be more adaptive and work with humans.

From driverless cars and drones, they try to sense and adapt to their surroundings.

Examples include Tug, a robot that delivers supplies around hospitals, Savioke, (which similarly delivers to hotel rooms), the new technology is moving from the factory into the service industry.

Brexit / Trump update

With Ted Cruz dropping out, Donald Trump may just have won himself the Republican nomination.

In American politics nothing is certain until the Party Convention. As we write the bookies are still pricing in a Hilary Clinton victory, though Bernie Sanders is not as yet out of the race.

The Brexit vote odds also still point to a comfortable IN victory. So in essence little has changed on either vote.

There is a chance that US interest rates will rise at the June Fed meeting but this may be postponed if the Brexit odds narrow.

Markets

In 2015 the markets had a good run until May; they then rolled over before rallying into the year end. 12 months ago the S&P 500 stood at 2076 and the end of April it was 2066.

This is despite the sharp deterioration of corporate earnings. So as we have said before there is the very real risk that if markets are efficient they should price in this fact.

However, as we have seen so far this year it doesn’t take much good news for the buyers to come out of the woodwork.

We are now entering the seasonally weak period of the year, regular readers will know about “sell in May go away don’t come back ‘til St Leger Day”, and with old world valuations stretched rational analysis suggests that the adage has a high probability of success again this year.

But stock markets are not logical, if they were the robots could do it all for us! Oil, Brexit, Trump, QE and any hint that countries are starting the load the helicopters with cash will all twist and turn these markets on a sixpence.

The big institutions are fearful, they do not want to miss out when the full recovery eventually arrives.

Traders are currently looking to bring the markets down, logic suggests it’s a good idea, but logic is rarely an accurate predictor of markets. April 2016

Click Here for Printable Version