Click Here for Printable Version

The bombing of Iran was supposed to be a short-term event that precipitated leadership change. The success of Venezuela has, so far, not been repeated and the dreaded military “mission creep” emerged. As we write, a two-week ceasefire has been agreed, and Donald Trump seemingly has the “off-ramp” he needs to extricate himself from what was becoming a politically and economically messy situation. The closure of the Straits of Hormuz has created a global shortage of crude oil, LNG, diesel, jet fuel, fertiliser and helium (required for semiconductor manufacturing). The US despite being self-sufficient in crude oil is not immune to global market prices and the politically toxic prices of gasoline and fertiliser have doubled at the wholesale level. With the mid‑term election process already under way, negative economic news was starting to accumulate. Comparisons with Iraq’s invasion of Kuwait and Russia’s invasion of Ukraine, both of which precipitated global recessions, made uncomfortable reading for markets. There is, however, a crucial difference this time. Oil and refined products were largely not totally removed from the market (aside from some missile damage) but are instead trapped in a vast maritime traffic jam. As a result, forward prices must factor in the possibility of a resolution that could trigger a sharp collapse in oil and related prices. Economically, therefore, this conflict would stimulate core inflation and force interest rates higher only if it became prolonged. As the Chair of the Federal Reserve Bank explained, interest‑rate policy is long‑term in nature, whereas oil shocks tend to be short‑term. Policymakers can therefore look through such shocks and adopt a “wait and see” approach. Nevertheless, there has been a disruption to oil and refined goods supply that will cause economic damage. Jet fuel is already running short across Europe, and Australia is facing rationing. There will be an impact on inflation question is for how long?

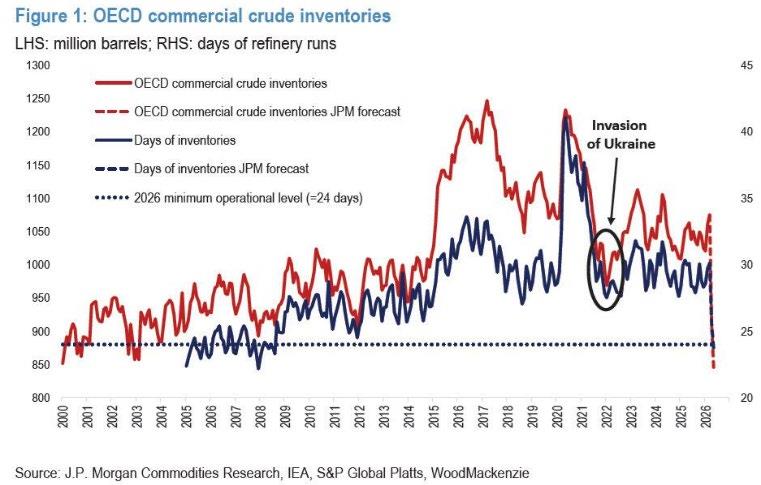

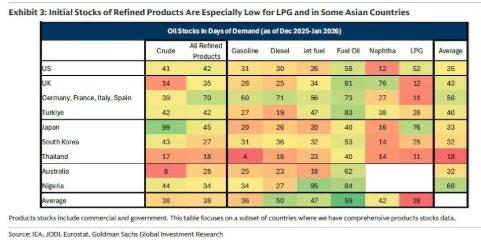

When does the Oil run out?

The first chart illustrates that global crude oil stocks were approaching critically low levels, nearing the minimum operational threshold. The second chart provides more significant insights by detailing refined product inventories measured in days. Some nations lack the capacity to fully refine their fuel requirements; for example, the United Kingdom can refine all its petrol domestically but only 30-40% of its demand for diesel, jet fuel, and heating oil. The situation remains complex, for example, the UK has limited LPG reserves but receives Norwegian and North Sea gas via pipelines on a just-in-time basis, with 76% of its gas supply originating from Norway and domestic fields. Fortunately, peak gas usage in the UK has passed as warmer weather reduces demand and boilers are switched off. Nevertheless, pricing is determined globally and genuine shortages in the Far East continue to exert upward pressure. So far, this shock appears manageable, avoiding the widespread manufacturing closures and food price surges seen following the Ukrainian invasion. However, elevated diesel and fertiliser costs are adversely affecting the Northern Hemisphere planting season at a critical moment, which is likely to result in food inflation later this year.

What happens to inflation?

As ever for markets the human cost of any conflict is irrelevant, it’s the impact on the three key market drivers (inflation, interest rate and corporate profits) that matter. Supply shocks are inflationary, they cannot be anything other, c50% price increases in key resources together with supply shortages make it inevitable that consumer and producer prices must rise. But, crucially for how long? Throughout this conflict key commodities such as oil and gasoline have seen their exchange prices in contango. This is an archaic market phrase that describes when contracts for immediate delivery “spot prices” are higher than those for delivery in three months. The markets are effectively saying that this supply stress is temporary. For Central Bankers, that were in a rate-cutting mindset, they now must refocus and will now be looking for signs that inflation has lurched upwards. The last time the global economy faced labour shortages as well, after Covid encouraged many skilled workers to retire early. This isn’t the case now, furthermore, global supply chains have been forcibly restructured by Trump’s tariffs. If the Straits reopen as promised (no guarantee as we write) then the market’s best guess, at present, is that the inflationary risk should pass quickly.

Corporate Earnings

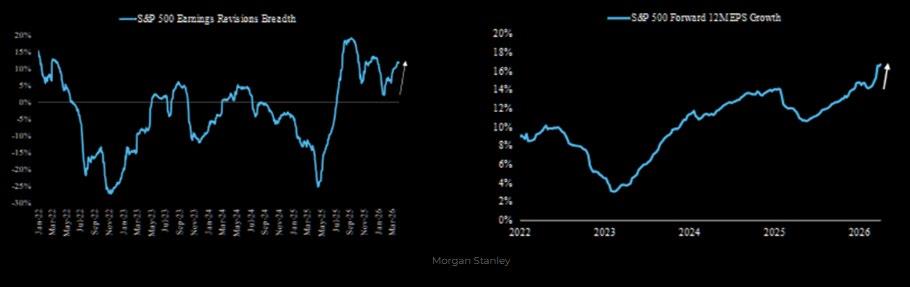

The irritating aspect for the markets about this conflict is that it was all looking so good. As these charts show, corporate profit growth was accelerating and spreading across a wider range of industries. Markets also enter earnings season with stocks on a below average valuation and the MAG 7 at their lowest valuation for over 5 years, just as AI adoption takes off. The biggest risk to earnings growth (and inflation) would be a prolonged conflict. Helpfully, shares, especially tech, are cheap and profits growing rapidly.

Markets

Clearly, events in the Middle East are fast‑moving and any comments in this newsletter could look very wrong, very quickly. Nevertheless, equity markets believe that Trump has the off-ramp he needs to put this issue behind him. There will undoubtedly be many weeks yet of news-flow that will move markets one way or the other, but for now, they have rapidly priced in a “return to normal”. For businesses and consumers, it will however take many months for supply lines of key resources to be fully restored to pre-conflict levels. What this means for interest rates is that Central Bankers now have a genuine excuse to do nothing. A version of “wait and see” will be in every statement from now on. This at a stroke has turned one of the key market drivers from positive to neutral, an unwelcome move. No one is talking of global recession. The AI and defence booms provide a solid growth base which would be hard to break, nevertheless, prolonged disruption of the Straits of Hormuz would bring the recession risk forward and thus end the present Bull cycle early. For now, the fragile ceasefire has reduced that risk, but it is important to note that it remains there in the background, Trump has released it. This appears to have been a “vanity project” for the President against the wishes of many in his party, it is a huge political risk for him just ahead of the mid-term elections, US voters are very sensitive to inflation and are also suffering under high mortgage rates, this conflict has just made both worse. For markets the “Trump Put” is more alive than ever, they assume he will now do whatever is necessary to help the US voter. Markets remain under the control of one man and events in one narrow waterway in the Middle East.