Click Here for Printable Version

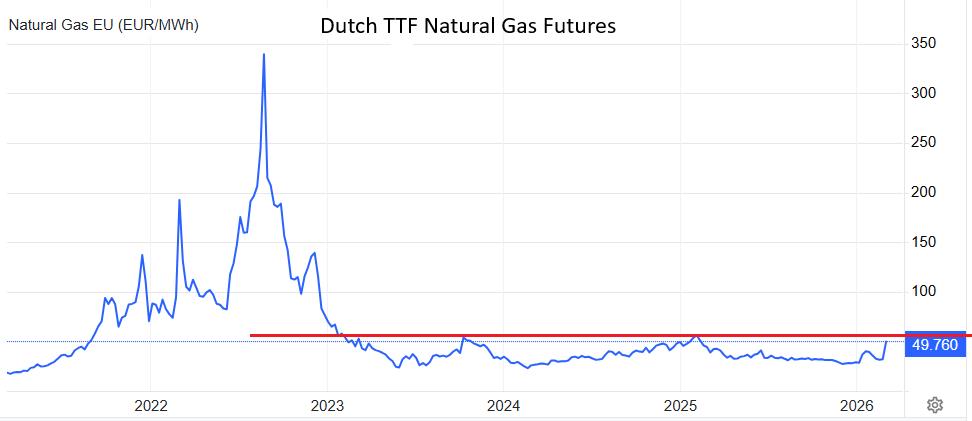

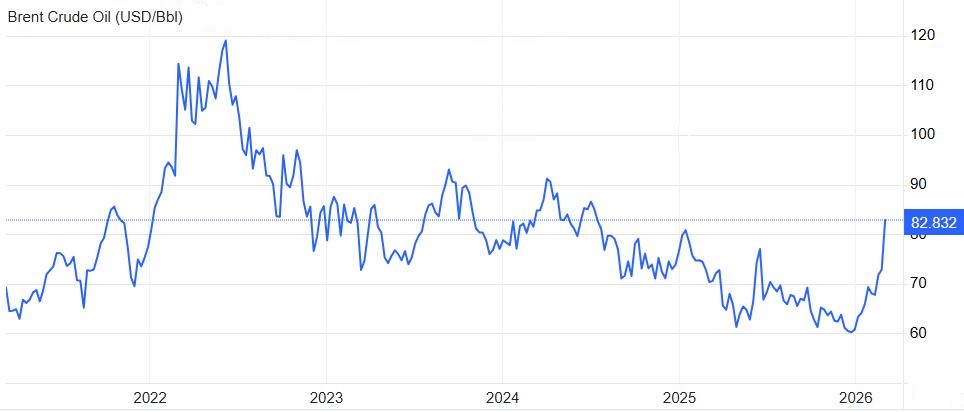

The economic calm in markets was shattered once again by geopolitics and by the words and actions of President Trump. The joint bombing of Iran, from the air and sea by combined US and Israeli forces, appears to have the objective of regime change. What form this might take remains open to speculation. The market believes Trump wants to follow his Venezuelan blueprint: removing the head of state and replacing him with an existing junior member of the regime. As ever, markets appear largely indifferent to the human cost of war in the Middle East; it is all about oil and gas (LNG). The bombings and the killing of Ayatollah Khamenei were initially met with a muted reaction in the commodity markets, as the Strait of Hormuz remained open. However, a subsequent Iranian change in tactics, attacking oil and gas infrastructure in the Gulf states, caused insurance premiums to surge, bringing oil and LNG traffic to a halt. This led to backlogs and cuts in production. Oil prices have since risen, while the already highly volatile Dutch LNG price has doubled. At a stroke, this has reignited dormant inflation fears, particularly in Europe. The economic impact of gas shortages and electricity price spikes following the Russian invasion of Ukraine remains a raw market memory. Is this simply the usual short‑term noise, or the beginning of another prolonged Gulf war with “boots on the ground”? This time is somewhat different. Trump is acting alone and does not have a clear legal mandate for his actions, hence the conspicuous absence of the usual allies (normally the UK and Canada). He also faces mid‑term elections this year, with the primaries already under way and has a high‑profile meeting with President Xi of China scheduled for the end of March. As a result, the probability, at present, is that this will be a short campaign. Clearly, both parties in the conflict are unpredictable; however, there does appear to be a pattern in Trump’s behaviour.

Trump Trading Strategy

Step 1.

Social Media. All the multitude of geopolitical issues the markets have faced during Donald Trump’s second term of office have started the same way, on social media with “classic Trump language” e.g. two months ago he posted several messages saying “a massive Armada is heading to Iran” and continuously urged Iran to “make a deal.” One month before the capture of the Venezuelan President he did the same thing, as he did with the EU over Greenland. Exert pressure, not through diplomats in private but on social media, in public. President Trump’s playbook is effectively verbal pressure on the target to “make a deal” using social media to magnify the pressure.

Step 2.

The Friday night verbal strike. One of the more consistent tactics in President Trump’s strategy is timing. Major announcements, military action or indeed sudden policy shifts have often occurred late on Friday evenings, after US equity markets have closed. After prolonged social media pressure, the strike is accompanied by threatening language.

Step 3.

The Monday morning sell-off. Traders have time over the weekend to digest the news and must “price it in”. Hence the Monday mark-down in prices. Equity, Bond and Commodity markets are thus being used to increase pressure on the target and instil a sense of fear and panic. The tariff war and the Greenland issue are classic examples of this strategy.

Step 3.

The Tuesday “Double Down”. This is designed counteract anyone who might think that the USA isn’t serious and have bought the Monday dip. Even stronger rhetoric that “doubles down” on the original Friday night strike, Recent examples include “wars can be fought forever”, “unlimited mid to upper tier weaponry” and “the big one is coming soon”. Markets start to assume that Trump is serious this time, that he is not looking for the usual quick win and thus need to price in a prolonged and economically disruptive period. Equity prices make another leg down.

Step 4

De-escalation. President Trump then historically introduces carefully calibrated de-escalation language, importantly, this does not resemble a retreat. When this happens depends on the magnitude of the market moves. Sharp downward moves often lead to quick soothing words from Treasury Secretary Scott Bessant. A recent example includes insurance cover for tankers transiting the Straits of Hormuz together with military escorts.

Step 5

The Deal. It doesn’t matter whether the President achieves his original demands, every major confrontation, so far, within this strategy ultimately concludes with an outcome that is framed as a strategic victory. The structure of the agreement varies by context and is often nowhere near the initial Step1 demands, but the language is always the same i.e. maximum pressure produced concessions. The success of the Venezuelan operation was not the capture of Maduro but persuading Delcy Rodríguez (Vice President) to take over as a compliant pro-USA leader. Best guess is that it would seem a similar strategy for Iran would be favoured. Whether “the Deal” ever justifies the market chaos created by this strategy is open to debate, investors must accept that they are in new world where volatility is to be expected.

Iran Oil and Gas

The biggest risk to earnings growth and inflation would be a prolonged conflict that drives oil and gas prices sharply higher. However, this would directly conflict with three core Trump policy priorities that have been repeatedly emphasised i.e. positioning himself as a peace-focused leader, reducing inflation and lowering gasoline prices. Elevated energy costs feed directly into US consumer sentiment and inflation data, which in turn influence voters during a midterm cycle. According to JP Morgan estimates, a full prolonged closure of the Strait of Hormuz could send oil prices to $120-$130/barrel. This would imply a spike in US CPI inflation to c5%. The last time we saw US inflation at 5% was in March 2023, when the Fed was aggressively hiking interest rates. This time with a weak labour market, a new Fed Chair and of course Trump as President it might be different?

Markets

Clearly, events in the Middle East are fast‑moving and any comments in this newsletter could look very wrong, very quickly. Nevertheless, equity markets believe that Trump cares as much about markets (perhaps more) as he does about Iran. He also faces a strict time window, he is meeting President Xi, a long‑time ally of Iran, at the end of March. Markets are therefore assuming that this conflict will be over and done with by then. Perhaps the Iranians believe this too and are simply playing for time. Much will depend on their reserves of drones and missiles. There are suggestions from various military websites that, at the current rate of use, these reserves could be exhausted by the weekend. Based on the strategy outlined above, we should be looking for comments from the Trump administration suggesting de‑escalation in the coming days. Markets will also be watching ship movements through the Strait of Hormuz. For the US, crude prices need to remain at least around current levels (c.$80). For Europe, it has been a cold winter and gas storage levels are low. As the chart above shows, while gas prices remain highly volatile, they are nowhere near the levels seen after the invasion of Ukraine. There are many headlines in the mainstream press, but in the markets, it remains business as usual, with recent moves largely dismissed as “normal noise”. Whether this conflict escalates into something more serious will depend on developments over the remainder of the month.