Click Here for Printable Version

Trump has reached a tentative agreement with Iran and ship transits through the Straits of Hormuz are slowly building. Brent crude oil prices have fallen sharply from a high of $114 to $76. This is important, as inflation fears have receded. Just how fragile this ceasefire remains to be seen, but the impression is that Trump has moved on and is now focusing on November’s mid-termelections. He needs gasoline prices and inflation to fall ahead of the vote, which is helpful for markets. While inflation expectations have fallen, interestingly there has been no recovery in bond prices. This suggests that traders do not believe there will be any further interest rate cuts. Politics plays a key part in bond pricing and this is particularly the case in the UK. A change in Prime Minister seems certain and this will be a tense time for gilts and sterling. The UK is heavily in debt and continues to spend far more than it receives in tax revenue. A promise to keep to self-imposed fiscal rules has kept the markets just about on side with the present “tax and spend” policies. Spending is fine if it generates a return greater than the cost of financing. The problem is that, so far, it has not. Part of that is geopolitical: the success of the Starmer/Reeves plan was always dependent on a booming US economy and minimal tariffs, which was risky. A new PM, who might be promising even more “tax and spend”, needs to ensure that the spending does, this time, generate a return. If not, markets can be savage and will punish gilts, which in turn will push mortgage rates higher, with negative consequences for the UK economy. Globally, although bond yields have not reacted to the improved inflation outlook, which would normally be a market negative, it is the third of the key market drivers, profit growth, that is delivering at present. Indeed, as we approach the second-quarter earnings season, the numbers are not just good; they are spectacularly good.

Key Market Driver Earnings Growth

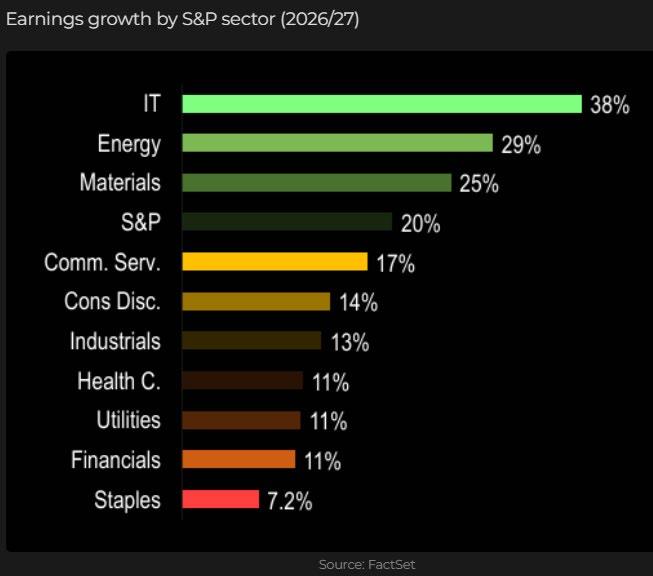

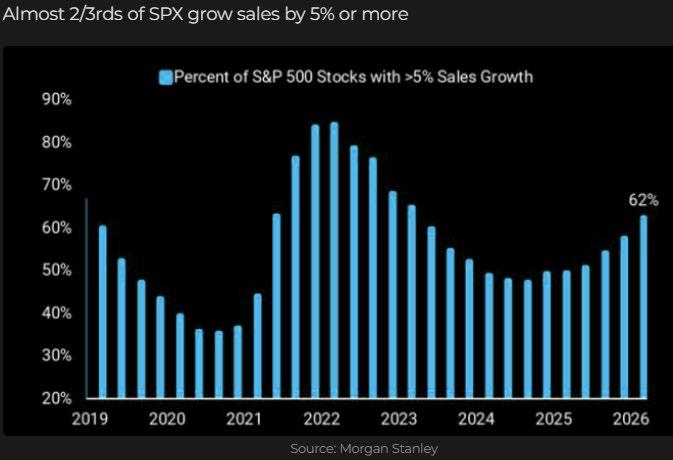

Historically, a good year for S&P 500 earnings growth is 7%, with 10% the norm at this early stage of the cycle. Current growth is running at an exceptional level of 20%. Part of this can be explained by the artificial intelligence boom and the boost to energy profits from the closure of the Straits of Hormuz, but, as the first chart shows, high levels of growth are common across most sectors, even consumer-facing ones. This is confusing, as the US consumer is struggling with high mortgage rates and inflation. One explanation may lie in the strength of the US stock market, US consumers might be banking investment gains to supplement their income, thereby outweighing higher mortgage costs. The second chart shows that these earnings are based on solid fundamentals. There is real sales growth taking place despite the impact of tariffs and inflation. US growth is presently good and, crucially, is broadly based as well. This is a positive sign for an economy that has had to contend with significant inflationary pressures and negative tariff news flow. The AI infrastructure build-out remains a major driver of earnings growth, the message from the March earnings season and in all probability the forthcoming June one, is that it is not the sole driver of market performance. This is important if the AI trade falters.

Upgrades and Valuations

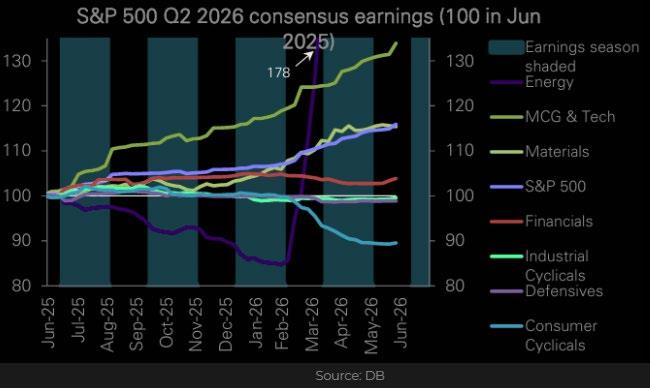

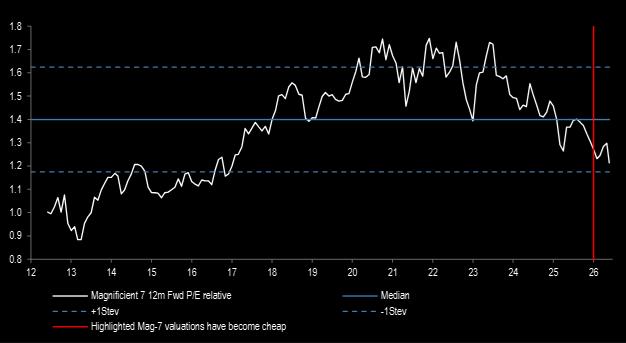

It is not just the high level of earnings growth that is important, but also the rate of change in the numbers. Remember, it is not only the direction of the three key drivers that matters, but also whether they are accelerating or decelerating. The first chart shows the change in consensus earnings by sector over the past 12 months. Energy has received a boost from the Iran conflict. Consumer Cyclicals, perhaps the sector most exposed to tariffs, is the one big negative, although even here there are some signs of life. Crucially, the financial sector earnings are picking up, there cannot be a true bull market without the banks. Interestingly, Mega Cap Tech continues to show the fastest rate of growth in expectations, yet, as the second chart shows, its valuation is now cheaper than the rest of the market. Nvidia remains cheaper than Coca-Cola, for example. This tells us that the market fears the AI trade may be another “tech bubble”. This is why earnings season is now so important to market direction. If companies such as Nvidia keep delivering profit and sales growth ahead of expectations, then the bull market can keep running.

UK

The next UK general election must be held no later than August 2029. As PM Keir Starmer leaves office, the UK has changed economic direction significantly under his premiership. Many of the current economic issues, such as anaemic growth and high inflation, cannot be attributed wholly to his leadership, but also reflect global events. Indeed, a comparison of UK GDP growth with that of the EU makes the UK look relatively good. The reality, though, is that many of the Budget decisions taken had an immediate negative financial impact on the economy, as well as a psychological one, killing off the “animal spirits” that are necessary for an economy to grow quickly. It may well be future generations that benefit from the infrastructure and energy investments started over the past two years, but in politics that is too long to wait.

Markets

The Straits of Hormuz has “sort of” reopened, however, it has been enough for oil prices to collapse and inflationary pressures to ease. Nevertheless, the inflationary “genie is out of the bottle”, agricultural prices are rising and a Super El Niño is coming this year, at just the wrong time. Markets must now assume that interest rates will, at best, remain unchanged from here. That is the message from the bond markets, where prices have not moved despite the reopening of the Straits. For markets, this means there is now no support from lower interest rates, which is why the strong earnings growth picture is so important. This is also typical of this stage in a bull market: the initial stimulus from central banks has now passed and it is up to companies themselves to deliver actual, rather than financially engineered, growth. Markets also need to be wary of Donald Trump’s actions. The Iran conflict has not sat well with US voters, he needs to deliver a vote-winner that cuts the cost of living, not too dissimilar to the position of the next Prime Minister in the UK. Markets need this earnings season to be very good.